Paybis vs Coinbase Commerce: Fee Comparison and Feature Analysis for DeFi Wallets

Key Takeaways:Paybis delivers transparent, itemized fees with no hidden spreads, a white-label widget deployable via a no-backend-required URL integration, and pre-acquired licensing across FinCEN, FINTRAC, VASP, and FCA jurisdictions covering 180+ countries. Coinbase Commerce brings institutional brand recognition and deep liquidity, making it a strong fit for US-centric platforms already inside the Coinbase ecosystem. If you need to calculate net received accurately before writing a line of integration code, ship an on-ramp this sprint, and offload KYC/AML ops without building a compliance team, Paybis is purpose-built for that. Subsequent card transactions process in approximately 30 seconds, Paybis supports 90+ cryptocurrencies and 20+ payment methods, and the platform carries 30,700+ Trustpilot reviews with an average rating of 4.1 out of 5 (“Great”).

Brand recognition does not equal integration speed. When you choose Coinbase Commerce based on brand alone, you often accept more complex SDK requirements, less transparent fee structures, and multi-week backend build timelines. For teams building DeFi wallets, an on-ramp is an infrastructure dependency.

You need to know exactly what your users receive, exactly how long the integration takes, and exactly which jurisdictions you can serve without building a legal department. This analysis breaks down both platforms on those terms so you can make the build-vs-buy decision with data.

Table of contents

Quick Comparison: Paybis vs Coinbase Commerce for Wallet On-Ramps

We break down the variables that matter most at the infrastructure decision stage.

| Feature | Paybis | Coinbase Commerce |

|---|---|---|

| Base service fee | From 1.49% (0% on first purchase) | 1% flat fee on all transactions |

| Fee transparency | Full breakdown shown before confirmation | Flat fee structure |

| Processing fee (card) | 4.5–8.5% for card transactions over $50 | N/A (crypto-to-crypto payments) |

| Integration options | Standalone URL, Web SDK, Native API | SDK and hosted checkout |

| Supported cryptocurrencies | 90+ | 100+ (primarily major assets) |

| Payment methods | 20+ including SEPA, PIX, ACH, M-Pesa | Cryptocurrency payments from crypto wallets |

| Geographic coverage | 180+ countries, 48 US states | US-focused, limited in key regions |

| Compliance licenses | FinCEN, FINTRAC, VASP (Poland), FCA | State-by-state MTL (US), FCA (UK) |

| KYC verification time | ~2 minutes | Varies by implementation |

| Subsequent transaction speed | ~30 seconds processing | Varies by payment method |

| B2B white-label | Full white-label with custom branding | White-label stablecoin solutions available |

| 24/7 human support | Yes, avg. 1–2 min response | Live chat, phone, and ticket support |

Fee Structures and Net Received Analysis

Most on-ramp relationships fail when the gap between what you advertise and what your user receives becomes too wide. A $1,000 USDC purchase that nets your user $930 is a very different product than one that nets $895, and that difference determines whether users complete their first transaction or abandon the funnel.

The core distinction between these two platforms is displayed fees versus embedded spreads. Paybis separates every fee into a line item visible before confirmation. Coinbase Commerce embeds a spread directly into the quoted price, meaning your user never sees it itemized.

How Coinbase Commerce Calculates Spreads and Transaction Fees

Coinbase Commerce applies a spread of approximately 0.5-2% by adjusting the asset’s buy price above the mid-market rate. You will not see this spread itemized as a fee in the transaction summary. Instead, Coinbase Commerce absorbs it directly into the exchange rate, so a user buying $1,000 of USDC sees a quoted “purchase price” that already includes a 1-2% markup with no line item disclosure.

On top of the spread, Coinbase Commerce charges a flat 1% processing fee across all transactions. Platforms embedding spreads can add 5-7% to the total transaction cost while disclosing only the visible fee percentage, leaving users to discover the full charge only at confirmation. For a platform building a transparent checkout experience, an opaque upstream pricing model makes it structurally impossible to publish an accurate net received figure before your user commits.

How Paybis Calculates Upfront Costs and Net Received

Paybis uses a three-part fee structure where every component appears before the user confirms payment. The structure breaks down as follows:

- Service Fee: Starts from 1.49% (the first card transaction per asset carries 0% service fee, with a $2 minimum applying after that)

- Processing Fee: 4.5-8.5% for card transactions over $50, depending on currency

- Network Fee: Varies by blockchain demand, typically $0.70-$3 for Bitcoin, updated in real time

For a $1,000 card purchase after the first transaction:

| Fee Type | Amount |

|---|---|

| Service Fee (1.49%) | ~$14.90 |

| Processing Fee (4.5–8.5%) | $45–$85 |

| Network Fee | ~$0.70–$3 |

| Total Fees | ~$60.60–$102.90 |

| Net Crypto Received | ~$897–$939 |

Example shown is for a transaction after the first purchase. First buy per asset carries 0% service fee.

This full breakdown is visible on the Paybis calculator before the user enters payment details. For B2B partners, fee structures are customizable per cryptocurrency and per payment method, creating a calculable revenue share model you can customize before committing engineering resources.

“fees are shown upfront, and transaction speeds were consistently good during my tests… Fees and exchange rates are displayed transparently before confirmation, making it easy to understand exactly what you” – Joon huh on G2

Integration Speed and API Flexibility

Every week of integration delay gives your competitors another week to compound user growth. You need to know which platform your team can ship against this sprint, not which one has better documentation in theory.

Coinbase Commerce SDK and Documentation

Coinbase Commerce requires backend integration to process payments and manage webhooks. The SDK supports standard e-commerce flows, but you will need to build backend API connections, webhook listeners, and compliance configuration before going live. For teams running a lean engineering squad, this backend requirement translates directly into sprints allocated away from core product work.

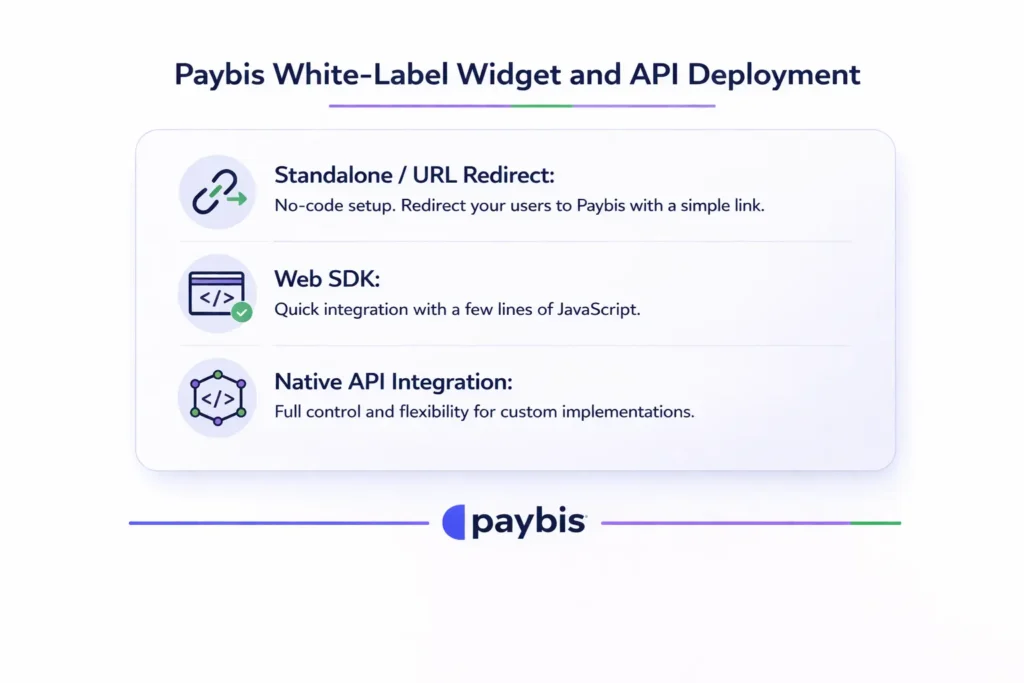

Paybis White-Label Widget and API Deployment

The Paybis widget offers three integration paths documented at docs.payb.is, each targeting a different point on the speed-vs-control spectrum:

- Standalone / URL Redirect: Build a signed URL with an HMAC signature and launch the Paybis widget. No Paybis API calls required beyond signature generation. This is the fastest path to production and ships in hours.

- Web SDK: Embed the widget directly into your page layout using JavaScript. Offers event handling and display control without full API integration.

- Native API Integration: Full server-to-server communication authenticated via a private API key. Unlocks Shared KYC (your already-verified users skip re-verification), Single Sign-On, one-click checkout, and frictionless off-ramping. The Widget API reference uses standard REST with Bearer token authentication and a sandbox environment.

The Standalone path requires zero interaction with the Paybis API beyond HMAC signature generation, which means a frontend-centric team can go from evaluation to live widget without waiting on backend resource allocation. The FXEmpire Paybis analysis confirms Paybis has processed over $2 billion in fiat-to-crypto transactions since launch, which validates the infrastructure reliability behind that deployment speed.

“I appreciate Paybis for its ability to facilitate instant cryptocurrency purchases using my card… I found the initial setup with Paybis to be easy and fast, contributing to a smooth onboarding experience.” – Denis I. on G2

“I like how easy it is to buy crypto with my card and send it directly to my wallet. The interface is clear, transactions are fast, and support has been helpful whenever I had questions.” – Elizar S. on G2

Global Compliance and Regulatory Coverage

Operating in 20+ countries without a dedicated compliance team is only possible if your infrastructure provider has already done the licensing work. Paybis holds four active regulatory registrations you can verify independently:

- FinCEN (MSB, United States): US entity #31000272911973, PL entity #31000277275964

- FINTRAC (MSB, Canada): M22061209

- Revenue Chamber in Katowice (VASP, Poland): RDWW-805

- FCA (Cryptoasset Registration, United Kingdom): Reference #928013

These are government-verified registrations, not marketing claims. Each registration requires ongoing audits, anti-money laundering programs, and customer fund protection protocols. Paybis also holds PCI DSS Level 1 certification (Payment Card Industry Data Security Standard), required for processing over 6 million card transactions annually.

The KYC flow offloads compliance ops from your team entirely. Verification takes approximately 2 minutes: the user uploads a photo ID and takes a selfie, and automated document recognition handles the rest. As BitTrust’s independent Paybis review confirms, verification completes automatically within 5 minutes in most cases. Partners using the Shared KYC feature via the Native API pass already-verified users through without requiring re-verification, which directly reduces drop-off at the identity check step.

Paybis covers 48 US states. New York and Louisiana apply specific state-level licensing frameworks and are currently excluded. US-heavy user bases with significant NY or LA traffic should factor this into integration planning.

Coinbase Commerce holds state-by-state money transmitter licenses in the US and maintains FCA authorization in the UK, which serves US-centric platforms well. Where Paybis differentiates is in LATAM and SEA coverage, where much of the DeFi wallet growth is occurring. Paybis’s global-first licensing structure covers these markets nativelywithin the same integration.

Supported Assets and Payment Methods

Paybis supports 90+ cryptocurrencies and 20+ payment methods across 180+ countries. Local payment methods include SEPA (Single Euro Payments Area for Europe), PIX (Brazil), ACH (Automated Clearing House for US), M-Pesa (Africa), SPEI (Mexico), Skrill, and Neteller. The platform supports 48 fiat currencies natively.

For DeFi wallets serving LATAM or SEA users, local payment method coverage directly impacts conversion. A user in São Paulo who cannot pay via PIX will not switch to a wire transfer. They drop off. Paybis’s regional payment method expansion covers these markets natively within the same integration, with no additional PSP contracts required.

“as someone who sometimes moves between countries, I appreciate Paybis working globally and letting me pay in many different fiat currencies. That flexibility really matters.” – Christine K. on G2

For DeFi protocols or wallets supporting emerging market users or niche asset classes, Coinbase Commerce’s asset coverage skews toward major tokens and is strongest in North America and Western Europe. Verify specific asset and payment method availability directly with Coinbase Commerce before assuming coverage.

Which On-Ramp Fits Your DeFi Wallet Roadmap?

Your decision maps to your product architecture and user geography.

Choose Paybis if:

- You need to ship a fiat on-ramp this sprint without multi-week backend work

- Your users are distributed across LATAM, SEA, or Africa and need local payment methods

- You need to publish accurate net received figures at checkout without spread opacity

- You are operating in 20+ countries and need pre-acquired licensing without building a compliance team

- Revenue share with transparent, customizable fees is core to your margin model

Coinbase Commerce Excells When:

- Your user base is primarily US-based, and Coinbase Commerce brand recognition measurably lifts conversion at checkout

- You are already deeply integrated into the Coinbase ecosystem (Prime, Custody)

- Institutional liquidity depth for large transaction sizes is your primary infrastructure requirement

Key Takeaways for Builders

- Paybis shows all fees (Service, Processing, Network) before the user confirms payment. Net received is calculable before you write a line of integration code.

- The Standalone URL integration requires no backend API calls beyond HMAC signature generation, which compresses deployment from weeks to hours.

- FinCEN, FINTRAC, VASP, and FCA registrations are verifiable in public government registries, not marketing claims.

- 90+ cryptocurrencies and 20+ payment methods across 180+ countries, with no new PSP contracts required.

Review the Paybis API documentation and sandbox environment to test the full widget flow without touching production infrastructure. Try the on-ramp at Paybis and get your first transaction underway.

Key Terminology

Net received: The actual cryptocurrency amount a user receives after all fees (Service, Processing, and Network) are deducted from the fiat purchase amount. Accurate net received calculations require full fee transparency before confirmation, which is why the distinction between itemized fees and embedded spreads matters at the integration decision stage.

Spread: A markup applied to the mid-market exchange rate that increases the effective buy price without appearing as a separate fee line item. Spread is how most on-ramp providers hide fees in on-ramp transactions, making it impossible for partners to publish accurate pre-confirmation net received figures.

Cascade routing: A multi-acquirer payment processing approach that automatically retries a declined card transaction through a secondary or tertiary payment processor before returning a failure to the user. This directly improves card approval rates without requiring the user to resubmit payment details.

HMAC signature: A Hash-based Message Authentication Code used to authenticate widget URL parameters in the Paybis Standalone integration. You generate it server-side to verify request parameters have not been tampered with, without requiring full Paybis API authentication.

VASP: Virtual Asset Service Provider, a regulatory classification required by the EU’s 5th and 6th Anti-Money Laundering Directives for businesses providing crypto exchange or custody services. Paybis holds VASP registration in Poland (RDWW-805) through the Revenue Chamber in Katowice.

FAQ

Can I customize the Paybis fee structure for different cryptocurrencies or payment methods?

B2B partners may be able to negotiate custom fee structures per cryptocurrency and payment method. Contact the Paybis B2B team to discuss available customization options and revenue share arrangements before committing engineering resources.

How long does Paybis KYC verification take for a new user?

Approximately 2 minutes for most users uploading a photo ID and completing a selfie check. Subsequent card transactions then process in approximately 30 seconds. Partners using Shared KYC via the Native API pass already-verified users through without requiring re-verification.

Does the Paybis Standalone widget integration require backend API calls?

No. The Standalone URL approach requires only an HMAC signature generated server-side. No Paybis API calls are required to launch the widget, as documented in the Standalone Integration guide.

Which US states are excluded from Paybis coverage?

New York and Louisiana require specific state-level licensing frameworks. Paybis currently covers 48 US states. US-heavy user bases with significant NY or LA traffic should factor this into integration planning before go-live.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info