Seamless Transactions: Skip the KYC

Simplify onboarding. Maximize transactions.

In the world of cryptocurrency, Know Your Customer (KYC) procedures are considered essential to ensure security and compliance with regulatory standards. However, for many users and businesses, the lengthy and often frustrating KYC verification process has become a significant barrier.

The extensive list of documents, passports, proofs of address, and residence permits required often discourages new users from joining the crypto ecosystem. This leads to lost customers and hinders conversion rates.

At Paybis, we understand this pain and have developed a solution to address it.

Table of contents

White-label On/Off Ramp with Streamlined KYC Flow

Introducing our White-label On/Off Ramp, a revolutionary instrument that allows you to eliminate the need for verification for transactions up to certain limits! With its streamlined KYC flow, this solution guarantees a more seamless onboarding process and increases the number of completed transactions.

KYC procedures are implemented by businesses to verify the identities of users and assess their suitability for engaging in financial activities. They are crucial in combating money laundering, terrorist financing, fraud, and other illicit activities.

While the idea of eliminating KYC may sound attractive, it is essential to consider the regulatory landscape and the risks associated with such a move, as completely removing it would expose platforms to increased risks.

Paybis takes a different approach by addressing the problem of lengthy KYC processes.

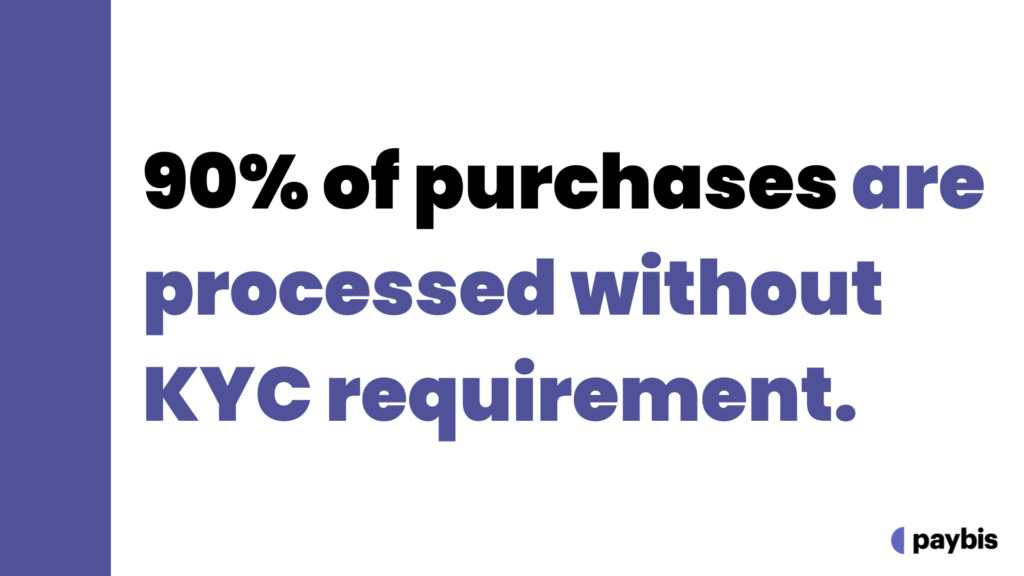

Our White-label On/Off Ramp solution eliminates the need for verification for transactions in 90% of first transactions.

Behind the Scenes

Behind the scenes, Paybis performs a number of checks to ensure compliance with regulatory requirements. This streamlined approach allows us to verify customers, ensure security and compliance, and provide a smoother onboarding process without burdening users with excessive documentation.

For your customers, this means that they can effortlessly buy cryptocurrencies within 20 seconds, without the hassle of going through the tedious verification process.

By removing the need for verification for some transactions, Paybis empowers businesses to attract and retain more customers and open up additional revenue streams. Our user-friendly onboarding process is especially beneficial for decentralized exchanges (DEXes), decentralized applications (DApps), non-custodial wallets, and even centralized exchanges. It not only streamlines the customer experience but also allows users to access services more quickly and easily, encouraging small transactions and increasing engagement.

Friction-Free KYC

While we prioritize security, we understand the importance of a hassle-free process. For transactions that exceed a certain threshold, our verification process remains simple, with no proof of address required in most cases. This customer-oriented approach allows Paybis to be a leader in enhancing approval rates and reducing customer loss during onboarding.

Contact us today to learn more about how Paybis can transform your business and enhance your customer journey in the world of cryptocurrency.

Why KYC Drop-Off Is a Revenue Problem, Not a Compliance Problem

Most businesses treat KYC as a regulatory checkbox. The smarter framing is to treat it as a conversion funnel. Every step you add between a user’s intent to buy and their first completed transaction is a place they can leave and not come back.

The data on this is consistent across on-ramp providers. Users who hit a verification wall on their first transaction abandon at significantly higher rates than those who complete without one. For DEXes, DApps, and non-custodial wallets where users already expect a low-friction experience, a traditional KYC flow feels like a contradiction in the product promise.

Paybis’s white-label on/off ramp handles 90% of first transactions without triggering a verification request. The compliance work still happens, it’s just moved behind the scenes so the user never sees it. The result is a buying flow that completes in under 20 seconds for most users, which is closer to the experience people expect from a wallet top-up than from an exchange account opening.

For businesses running crypto wallet infrastructure, the plug and play crypto wallets product takes this further. It combines the streamlined onboarding with 50+ payment methods and instant stablecoin settlements, handling fraud and chargebacks from day one so your team doesn’t need to build that layer separately.

Who This Actually Serves: B2B Use Cases Beyond the Obvious

The article mentions DEXes, DApps, and non-custodial wallets. The use cases extend further than that.

Centralized exchanges looking to reduce onboarding friction for new users benefit from the same logic. A user who completes their first small purchase without friction is significantly more likely to return, verify fully, and increase their transaction size over time. The no-KYC threshold creates a low-stakes entry point that feeds the top of that funnel.

For businesses that need to move funds on behalf of clients or pay out to multiple wallets, Paybis Send handles bulk crypto transfers with the same compliance infrastructure underneath, so the regulatory requirements are met without being handed to the end user as their problem.

Corporate treasury teams and OTC buyers have a separate track through the corporate account product, which is designed for larger volumes with dedicated support rather than self-serve onboarding.

Understanding where authorization rates break down across different user segments is also worth reviewing before choosing an integration approach. The breakdown of authorization vs success rates for on-ramps shows why a high authorization rate at the payment step doesn’t always translate to completed transactions, and how the KYC layer interacts with that gap.

FAQ

Does the no-KYC flow still apply after MiCA came into force in December 2024?

Yes, within the thresholds set per jurisdiction. For EU users, Paybis applies the appropriate verification logic in the background based on MiCA requirements. The no-KYC experience up to $2,000 remains available where regulations permit it, and Paybis handles the compliance mapping so your platform doesn’t have to. For a full picture of what MiCA means for partners, see the Paybis EU licensing post.

How does Paybis verify returning users without asking them to re-submit documents?

Once a user has completed verification through any Paybis-powered integration, that verification is stored at the Paybis level. When they arrive at your platform, Paybis recognises them and skips the re-verification step. This shared verification pool is one of the main practical advantages of building on Paybis rather than a provider who starts from zero with every new partner. It also ties directly into the passwordless login flow, which removes the authentication friction on top of the KYC friction.

What happens when a user exceeds the no-KYC threshold mid-transaction?

If a transaction would push a user past the threshold, Paybis prompts verification inline before completing the purchase. The user doesn’t hit a dead end or get redirected out of your platform. The verification step appears within the existing flow and, once completed, the transaction continues. For partners running higher-volume use cases, the corporate on/off-ramp covers different limit structures.

Does the no-KYC flow affect approval rates?

It tends to improve them. Fewer steps before payment means fewer drop-offs. The no-KYC flow removes a point in the funnel where users historically abandon, which is particularly relevant in markets where users are less willing to share documentation for smaller purchases. If approval rates by market are something you’re tracking, the Paybis partner portal gives you real-time data broken down by payment method and geography.

Does skipping KYC mean the platform is unregulated?

No. Paybis performs compliance checks behind the scenes on every transaction. The user doesn’t go through a document upload flow for smaller transactions, but the regulatory requirements are still met. Platforms remain fully compliant while users experience a faster onboarding process.

What types of businesses benefit most from streamlined KYC?

DEXes, DApps, non-custodial wallets, and centralized exchanges all benefit from reducing onboarding friction. Any product where users expect a fast, self-serve experience will see higher conversion rates when the first transaction completes without a verification step.

What happens when a transaction does require verification?

For transactions above the threshold, Paybis’s verification process is simplified. In most cases no proof of address is required. The process is designed to retain as many users as possible rather than applying a one-size-fits-all document checklist.

Can businesses combine the no-KYC on-ramp with other Paybis products?

Yes. The white-label on/off ramp, plug and play wallets, and Paybis Send are separate products that can be used independently or together depending on the use case. Businesses handling both retail top-ups and bulk payouts can run both alongside each other under the same compliance umbrella.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info