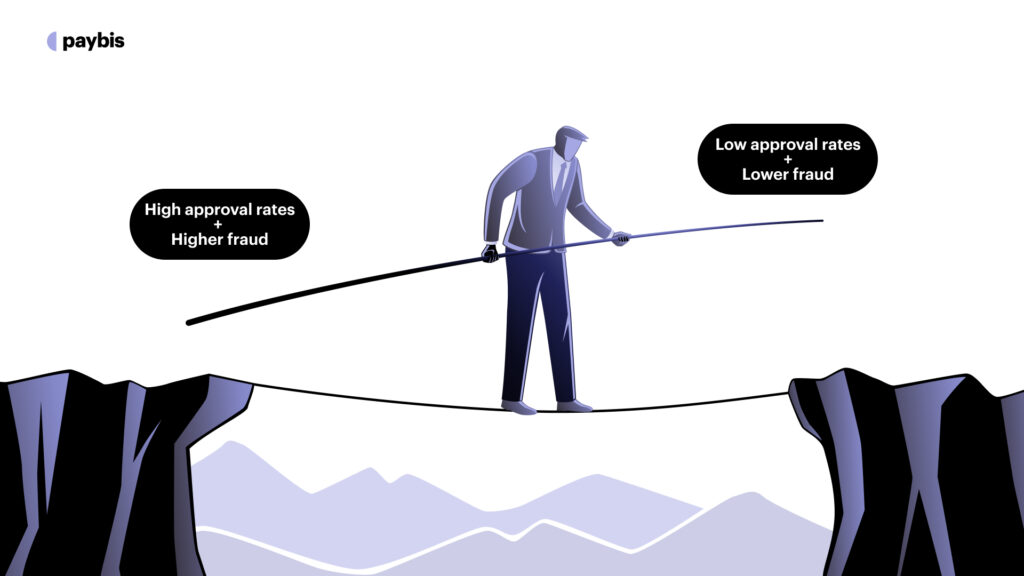

Double-Edged Sword: How to Balance Between High Approval Rates and Fraud?

Companies enabling cryptocurrency transactions are grappling with a critical dilemma: how to maximize transaction approval rates while effectively guarding against fraud.

This equilibrium is not just a matter of operational efficiency but is crucial for the sustainability and growth of businesses in today’s fast-paced market.

The complexity of this issue is further accentuated in the case of cryptocurrency transactions. Given their reputation for being anonymous or pseudonymous, these transactions pose unique challenges.

For instance, banks tend to reject crypto-related transactions due to the high-risk perception associated with MCC 6051, adding another layer of complexity for businesses trying to navigate these waters.

In this article, we will explore how apps and websites offering cryptocurrencies to their customers can balance between high approval rates and fraud.

Table of contents

The Tightrope of Transaction Approval

Companies constantly walk a tightrope when it comes to transaction approvals.

The goal is to maximize revenue growth by approving as many transactions as possible, a strategy inherently tied to customer satisfaction and business expansion.

However, this approach is not without its risks.

Maximizing Revenue through High Approval Rates

The correlation between high transaction approval rates and increased revenue is undeniable.

Every approved transaction represents potential income, making the approval process a critical driver of growth.

Crypto businesses are under constant pressure to streamline their approval processes to ensure a higher rate of successful transactions.

This approach is not merely about approving more transactions; it’s about recognizing legitimate transactions that might otherwise be declined due to overly cautious fraud prevention measures.

The Risks of High Approval Rates

However, the pursuit of high approval rates is not without significant risks. The most glaring of these is the increased susceptibility to fraudulent transactions.

As businesses loosen their transaction scrutiny to boost approvals, they inadvertently create vulnerabilities that can be exploited by fraudsters. This not only leads to financial losses but can also have legal repercussions, especially in industries subject to stringent regulatory compliance like cryptocurrency trading.

Moreover, the reputational damage from fraud incidents can be long-lasting and far more damaging than the immediate financial losses. It affects customer trust, which is a cornerstone of business success in the digital era.

A single major fraud incident can erode years of built-up customer confidence and goodwill.

Balancing Approval Rates and Fraud Prevention

The balancing act here is delicate: approve too many transactions without due diligence, and the risks escalate; be overly cautious and restrict too many legitimate transactions, and customer frustration mounts, potentially harming the lifetime value of customers and increasing customer acquisition costs.

The key challenge, therefore, lies in finding the optimal balance between maximizing transaction approvals and minimizing the risk of fraud.

This necessitates a sophisticated approach to transaction screening, one that can intelligently differentiate between legitimate and fraudulent activities. It also involves a dynamic adjustment of fraud prevention strategies based on evolving patterns and trends in fraudulent activities.

The Complexity of Crypto Transactions

Cryptocurrency transactions present a unique set of challenges that set them apart from traditional financial transactions.

Unique Nature of Cryptocurrency Transactions

Cryptocurrency transactions are fundamentally different from traditional transactions. They are digital, decentralized, and sometimes anonymous.

This anonymity and lack of a centralized authority make crypto transactions inherently risky from a fraud prevention perspective.

Additionally, cryptocurrencies can be highly volatile, adding another layer of complexity to the transaction approval process.

Businesses dealing with cryptocurrencies need to be acutely aware of these differences and tailor their transaction approval strategies accordingly.

High-Risk Nature of MCC 6051 Transactions

Transactions categorized under Merchant Category Code (MCC) 6051 are considered high-risk due to their association with quasi-cash or cryptocurrency transactions.

These transactions are often scrutinized more heavily by banks and financial institutions, leading to higher rates of rejection.

The challenge for businesses, therefore, is to develop a nuanced understanding of the risk profile of MCC 6051 transactions and to implement appropriate measures that can mitigate these risks without overly restricting legitimate transactions.

Inadequacy of Traditional Transaction Approval Methods

Traditional transaction approval methods, designed primarily for conventional financial transactions, are often ill-equipped to handle the peculiarities of crypto transactions.

These methods may not effectively account for the unique risk factors associated with cryptocurrency, leading to either a high rate of false positives (legitimate transactions being declined) or a failure to catch fraudulent activities.

This necessitates the development of specialized strategies and tools tailored to the specific needs of cryptocurrency transactions.

Useful links

Streamlining Verification Processes

Identity verification is a critical tool in fraud prevention. It helps ensure that transactions are legitimate and comply with regulatory requirements.

However, overly complex or time-consuming verification processes can deter legitimate customers, leading to abandoned transactions and a poor user experience.

The challenge lies in implementing a KYC process that is both thorough enough to deter and detect fraud and streamlined enough to not inconvenience legitimate customers.

Paybis’s Simplified KYC

Paybis introduces an innovative approach to KYC with its Simplified KYC system.

This system is designed to provide speedy and efficient user verification while maintaining high-security standards.

By minimizing the need for extensive documentation and leveraging advanced technologies, Paybis’s approach can significantly enhance user convenience without compromising on the thoroughness of the verification process.

The entire process, from onboarding to transaction takes an average of 78 seconds with Paybis.

Real-Time Transaction Screening

The ability to screen transactions in real-time offers a significant advantage in identifying and preventing fraudulent activities as they happen. This immediacy is crucial in the fast-paced environment of digital transactions, where delays can lead to missed opportunities for fraud detection and prevention.

Traditional transaction screening methods take hours or even days. So, they aren’t ideal if you want to serve your customers instantly or before they look for an alternative solution that fulfills their needs.

Paybis addresses these challenges by incorporating Artificial Intelligence (AI) and Anti-Money Laundering (AML) algorithms:

- AI in Screening: AI allows for dynamic and adaptive screening, capable of analyzing large data sets and identifying emerging fraud patterns.

- AML Algorithms: These algorithms are crucial for regulatory compliance and detecting potentially illegal activities, enhancing the security of transactions.

Handling the Inevitable: Chargeback Protection

Despite the best efforts in fraud prevention and real-time screening, no system is entirely foolproof. Chargebacks remain an inevitable aspect of digital transactions, especially in the high-stakes world of cryptocurrency.

Recognizing the challenges posed by chargebacks, Paybis has implemented a policy of 100% chargeback protection.

This policy is designed to support our partners against the financial losses from chargebacks, providing several benefits:

- Financial Security: By offering chargeback protection, Paybis helps businesses mitigate the financial risks associated with disputed transactions.

- Operational Efficiency: This protection reduces the administrative burden on businesses, as they don’t have to invest resources in handling chargeback disputes.

- Customer Confidence: Knowing that there’s a safeguard against chargebacks can enhance customer trust and confidence in the transaction process.

Final Thoughts

This balance between approval rates and fraud hinges on several key strategies. The complexity inherent in cryptocurrency transactions, marked by factors like the high-risk nature of MCC 6051 and bank rejections, demands a nuanced approach to transaction approval.

Building customer trust emerges as a cornerstone in this landscape, where strategies such as providing social proof, exceptional customer service, and transparent operations play pivotal roles.

Simultaneously, the importance of streamlining verification processes, such as implementing efficient yet thorough KYC measures, becomes apparent. Paybis’s Simplified KYC exemplifies an innovative approach in this regard.

Businesses that effectively integrate Paybis to cater to the needs of their customers while abstracting away the hassles of building a product and team from scratch in uncharted waters.

FAQ

How does fraud prevention affect the experience for legitimate users?

When it’s done well, users barely notice it. Platforms integrated with Paybis let customers buy crypto while KYC and fraud screening run transparently in the background, without adding unnecessary friction to the purchase flow.

Are bank transfers safer from a fraud perspective than card payments?

Generally yes. Customers who buy Bitcoin with a bank account carry a lower chargeback risk compared to card-based transactions, even though bank transfers still fall under MCC 6051 scrutiny from financial institutions.

Does AML screening apply when selling too, or just when buying?

Both directions. When customers sell Bitcoin, the same real-time AML screening runs in reverse to verify the transaction is legitimate before any fiat funds get released on the other side.

When are chargebacks most likely to occur in the crypto flow?

The highest risk point is typically when users withdraw Bitcoin to a bank account. That fiat settlement step is where disputed transactions most commonly surface, which is why chargeback protection at that stage is so important.

How can businesses help their customers recognize fraud attempts?

Understanding how to spot and avoid crypto scams gives both businesses and their users a clearer picture of the patterns that fraud prevention systems are built to catch. An informed customer is a much harder target.

I keep seeing KYC mentioned. What does it actually involve?

If you’re not familiar with what KYC means and why regulators require it, getting that foundation in place helps you understand why streamlining the verification process has such a direct impact on approval rates and customer drop-off.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info