B2B Stablecoin Payments: The $226B Market Most Businesses Miss Out On

- B2B stablecoin payments reached $226 billion in 2025, around 60% of all stablecoin payment volume globally

- B2B stablecoin payments grew 733% year over year in 2025

- On Paybis, stablecoins grew from 12.1% of crypto volume in July 2023 to 85.7% by April 2026

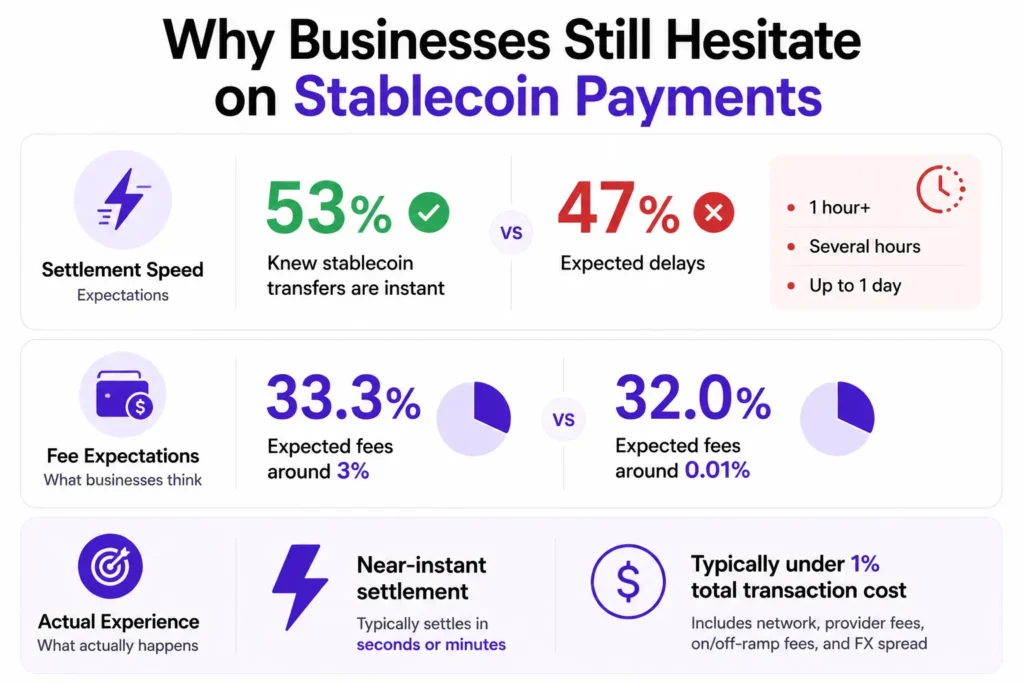

- Nearly half of the businesses surveyed thought stablecoin transfers take hours or a full day to settle. They actually take seconds

- One-third of businesses expected stablecoin fees around 3%. The real cost is generally below 1% end to end

- 22.5% of surveyed businesses already use stablecoins for international payments or plan to

Most stablecoin coverage focuses on retail. Will consumers pay with crypto? When does this go mainstream? The debate carried on, and businesses quietly started using stablecoins to pay suppliers, move treasury, and run international payroll at scale.

The retail question is still open. The B2B move already happened, and the numbers behind it are bigger than almost anyone expects.

If you want to see what a stablecoin transfer costs for your own transaction size, Paybis shows the full breakdown before you commit.

Why are businesses switching to stablecoin payments?

Because traditional cross-border payments are slow, expensive, and hard to track, stablecoins fix all three at once. A wire transfer takes 2 to 5 business days, costs $25 to $50 before correspondent bank fees, and gives you little visibility into where the money actually is.

Stablecoin payments settle in seconds to minutes. They generally cost below 1% end to end. Both sides get a clear transaction trail they can check at any time.

For a business paying international suppliers, contractors, or running global payroll, that difference shows up directly on the bottom line.

How big is B2B stablecoin activity right now?

It’s bigger than most people expect. B2B stablecoin payments reached an estimated $226 billion in 2025, about 60% of all real stablecoin payment volume globally, and grew 733% year over year.

To put that number in context, McKinsey separates actual payment use from the trading and internal fund movements that inflate raw blockchain figures. The $226 billion reflects real business transactions, not market noise.

What does Paybis transaction data show?

The same pattern is visible at the platform level. Stablecoins went from 12.1% of Paybis crypto volume in July 2023 to 85.7% by April 2026, and the customers behind that volume changed just as fast.

B2B transactions were 35.7% of Paybis stablecoin volume in 2023. By 2025, that figure was 96.9%, and in the first four months of 2026, it reached 97.8%.

Total stablecoin volume on Paybis hit $2.81 billion across the review period. Of that, $957 million landed in January to April 2026 alone.

What kinds of businesses are driving this?

Interestingly, the answer is not crypto companies. The five largest sectors on Paybis since April 2024 are digital goods, virtual asset businesses, technology, retail and e-commerce, and fintech. Together, they account for 78.4% of all B2B stablecoin volume.

These are businesses that operate across borders, serve global customers, and run high-volume payment flows. Those are exactly the flows where traditional rails create the most friction.

So why haven’t more businesses moved over?

Because most still don’t have accurate information about how stablecoin payments actually work. Paybis surveyed more than 1,000 business decision-makers in May 2026, and the results show a clear knowledge gap between interest and adoption.

On settlement speed, only 53% correctly identified stablecoin transfers as instant. The other 47% expected settlement somewhere between one hour and a full day. A full 17.4% expected a whole day, close to a traditional wire timeline.

On fees, 33.3% expected costs around 3%, and 32% selected 0.01%. The two largest groups landed at opposite ends of the range. The real figure sits below 1% end to end for most transactions, though the full cost includes the network, the provider, on and off-ramp fees, and any FX spread.

A business working from either estimate is not comparing stablecoins against its current payment providers on accurate terms.

Which businesses does this make the most sense for?

Any business that moves money internationally on a regular basis. That covers supplier payments, contractor payouts, global payroll, marketplace settlements, and cross-border treasury transfers.

The math is easiest to see on a single payment. Take a $50,000 supplier payment:

| Method | Cost rate | Cost per payment | Cost over 12 monthly payments |

|---|---|---|---|

| Wire transfer | 2% | $1,000 | $12,000 |

| Stablecoin transfer | 0.5% | $250 | $3,000 |

| Difference | $750 | $9,000 |

So one payment flow, run monthly, saves $9,000 a year. The fit is weaker for domestic payments where local bank transfers are already cheap and fast. It is also weaker for very small transactions, where fixed fees eat into the advantage.

If you want to see what the difference looks like for your own transaction size, Paybis shows the full cost breakdown before you commit.

Bottom Line

You can think of B2B stablecoin payments as a future use case. However, the businesses that figured out what stablecoins actually cost and how fast they actually settle have been moving real money at scale for two years.

The research shows that for the businesses that haven’t moved yet, the gap is hardly the technology or the regulation. It is accurate information. And that is a much easier problem to solve.

FAQ

How fast do stablecoin business payments settle?

Stablecoin transfers settle in seconds to minutes, regardless of which country the recipient is in. A traditional wire takes 2 to 5 business days. This is the single biggest reason businesses with international payment flows make the move, since it frees up working capital that would otherwise sit in transit.

What do stablecoin payments actually cost?

For most transactions, the all-in cost sits below 1% end to end. That figure includes the network fee, the provider fee, on and off-ramp fees, and any FX spread. It compares against roughly 2% or more for a wire once correspondent bank charges are added, though the exact number depends on your transaction size and route.

Are stablecoin payments only useful for crypto companies?

No. The largest sectors using them on Paybis are digital goods, virtual asset businesses, technology, retail and e-commerce, and fintech, which together make up 78.4% of B2B stablecoin volume. The common thread is cross-border activity and high payment volume, not crypto itself.

When do stablecoin payments not make sense?

They make less sense for domestic payments where local bank transfers are already cheap and fast. They also make less sense for very small transactions, where fixed fees reduce the advantage. The benefit is clearest on regular, larger, cross-border flows like supplier payments and global payroll.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info