Crypto Compliance Explained: KYC, AML, and Licensing Requirements

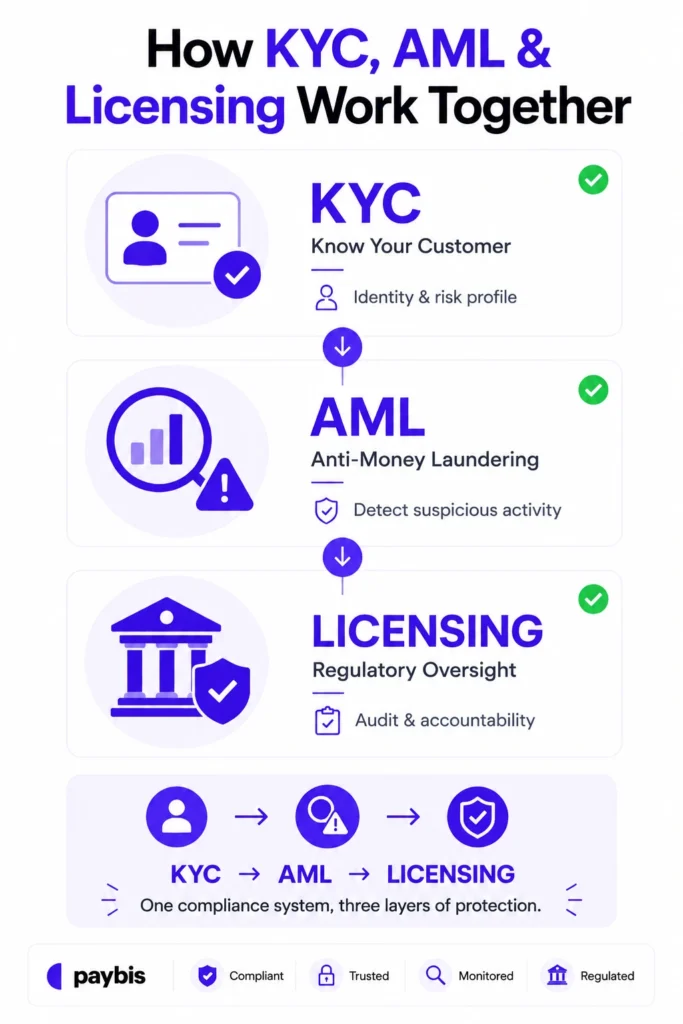

- KYC, AML, and licensing are three separate compliance layers. Each carries its own requirements and its own enforcement risk.

- KYC is about verifying who your customers are before they transact. AML is about monitoring what they do after. Both are mandatory in every major jurisdiction.

- Licensing goes beyond KYC and AML. A licensed business has been reviewed and approved by a financial regulator, not just registered with one.

- Under MiCA, any platform serving EU crypto users must hold a CASP licence. Operating without one is a legal violation with fines of up to 15% of annual turnover.

- Non-compliance consequences are not theoretical. Binance paid $4.3 billion to US regulators in 2023. BitMEX founders faced criminal charges. Enforcement has reached every corner of the industry.

In 2023, Binance paid $4.3 billion to US regulators. The fine was the largest in US financial history at the time. It came from running a global crypto exchange for years without compliance controls. That is what it cost.

For smaller businesses, it does not take years to reach that point. One banking relationship terminated over a compliance concern can shut the business down in days. The scale is different, but the mechanism is the same.

This guide covers what KYC, AML, and licensing each actually require, why they are different obligations rather than different names for the same thing, and how to think about them as a connected system.

What Is Crypto Compliance and Why Does It Matter?

Crypto compliance is the body of legal obligations that crypto businesses must meet to operate lawfully. At its core, it covers how you verify customers before they transact and whether your business is actually authorized to offer services in the first place.

The stakes have shifted sharply over the past few years. The early crypto industry operated in a regulatory grey zone where enforcement was rare, and consequences were limited. That era is over. The EU’s MiCA regulation has been fully in force since December 2024. US enforcement actions have produced multi-billion dollar settlements. The FCA in the UK has rejected most crypto firm applications it has received. Compliance is no longer a legal formality. It is the condition for staying in business.

For businesses that want to offer crypto services without building the compliance infrastructure from scratch, the Paybis on/off-ramp handles verification and monitoring on the integration side.

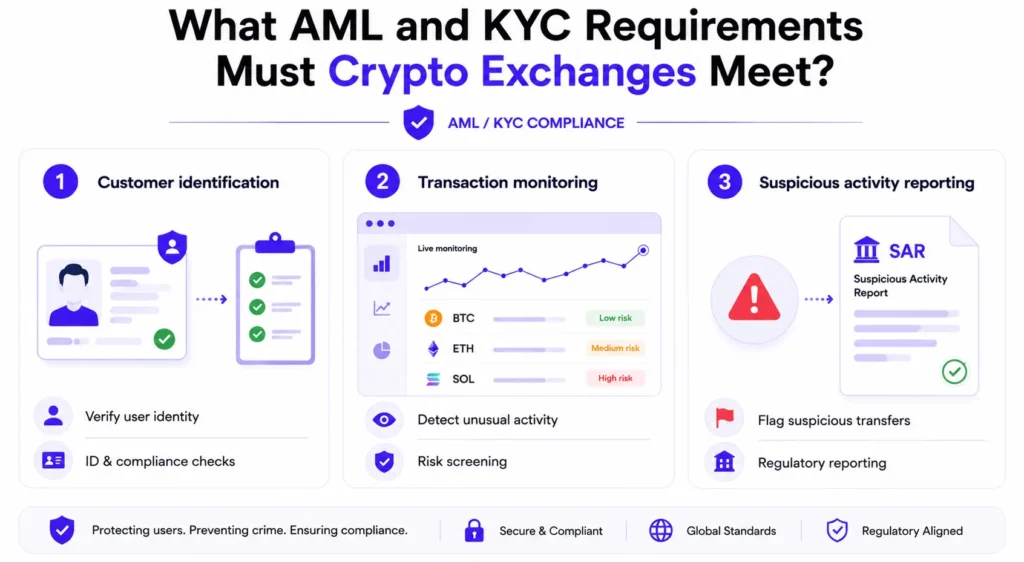

What Is KYC in Crypto and What Does It Actually Require?

KYC stands for Know Your Customer. In practice, it means verifying who your users are and building enough of a picture to recognize when their activity stops making sense. Every major jurisdiction that regulates crypto requires it, and what regulators actually expect goes well beyond a signup form.

- Verification starts with identity. A government-issued document and a biometric check confirm who the person claims to be. That is the starting point. The Paybis KYC guide covers how verification design balances compliance requirements with user experience in practice.

- What regulators look for is a risk-based program. A retail customer making their first small purchase is a different risk profile from a corporate account moving significant volume. The program needs documented policies that reflect those differences. Applying the same process to every customer regardless of risk is not what a regulator wants to see, and it will come up during review.

- The part most businesses get wrong is treating KYC as a one-time onboarding exercise. Regulators expect it to run continuously. When a high-risk customer’s circumstances change, the records need to update. When transaction patterns shift away from the customer’s stated profile, that triggers a new review. A user who cleared verification at signup but has since started moving funds in ways inconsistent with what they told you is a compliance problem, regardless of how clean the original check was.

- Documentation is what makes the program defensible. When a regulator asks to review your KYC process, they want the written policies, the risk methodology, the customer records, and evidence that the process ran as described. A program that lives only in the heads of your compliance team will not hold up.

What Is AML in Crypto and How Does It Work?

If KYC is about knowing who your customers are, AML is about watching what they actually do. The two feed each other, but AML is a separate legal obligation with its own requirements.

The foundation of any AML program is transaction monitoring. This means watching customer activity continuously and flagging patterns that are inconsistent with what you know about them. A customer moving large amounts quickly between wallets without any clear commercial reason is one example. Deposits followed immediately by outbound transfers to unrelated addresses is another. The monitoring system needs to be calibrated to your specific customer base, because a generic alert threshold applied across the board generates noise instead of signal.

When monitoring flags something that cannot be explained by the customer’s profile, the obligation is to file a Suspicious Activity Report with the relevant financial intelligence unit. Failing to file when the threshold for suspicion is crossed is a criminal offence in most jurisdictions, separate from whatever the underlying activity was.

Beyond monitoring, AML requires a compliance officer with genuine authority to act on findings. Staff training is mandatory. An annual independent audit of program effectiveness is required. Transaction records must be kept for a minimum of five years in most jurisdictions. FATF Recommendation 15 explicitly captures crypto businesses as obligated entities, putting them on the same footing as banks.

The most common AML failure regulators see is a program that exists on paper but has never been calibrated to the actual risks of the business. A crypto exchange that has operated for three years without generating a single SAR will be questioned on whether the monitoring is functioning or just running in the background. For partners using the Paybis Corporate On/Off Ramp, AML monitoring and KYB for corporate accounts are handled on the Paybis side.

What Are the Licensing Requirements for Crypto Businesses?

This is where the compliance picture expands beyond what most businesses expect. KYC and AML are compliance obligations. A licence is an authorization to operate. Having an AML program in place does not mean you are licensed, and the difference between a registration and a full licence is where most enforcement risk currently sits.

Most crypto businesses in Europe have historically held AML registrations. A registration tells the regulator you exist and have committed to anti-money laundering rules. What it does not establish is that a regulator has reviewed your business and decided it meets the standard for offering financial services to customers.

Under MiCA, that distinction became legally significant in December 2024. Any platform offering crypto services to EU clients now needs a CASP licence. Getting it requires a full regulatory review. The regulator looks at governance, capital, management suitability, and IT security before granting authorization, and each element is assessed on its own terms. Operating without that licence while serving EU users is a legal violation.

Outside the EU, the frameworks differ but the direction is consistent. The US requires FinCEN registration at the federal level plus money transmitter licences in every state where customers are served. That alone can mean dozens of separate applications for a business with national reach. The UK’s FCA has approved fewer than 15% of crypto firm applications since its registration regime launched. The bar everywhere is rising, and registration-level compliance is becoming insufficient wherever serious volume sits. The crypto exchange regulations guide covers the full compliance picture for licensed platforms.

How Do KYC, AML, and Licensing Connect?

Getting compliance right means understanding how these three layers feed into each other. Each one depends on the others functioning properly.

- KYC feeds AML. The customer profile you build during onboarding is the baseline your transaction monitoring uses to decide whether activity is normal or suspicious. A monitoring system without good customer data has no context to work from. It generates alerts it cannot prioritize and misses patterns it cannot recognize because it has no reference point for what normal looks like.

- AML feeds licensing. When a regulator reviews a CASP application, the AML program is one of the most closely examined elements. They want evidence it was built for the specific business and tested against real activity. They want to see that the person running it has genuine authority to act on findings. An AML program that has never produced a single SAR in a business that has run for years is a red flag, not a clean record.

- Licensing holds everything accountable. A CASP licence commits the business to maintaining the KYC and AML program to the same standard indefinitely, with annual audits to demonstrate it. The governance approved at licensing still needs to reflect how the business actually runs twelve months later. When it drifts, the licence is at risk.

Businesses that survive regulatory scrutiny treat compliance as one connected system. The ones that struggle treat it as separate departments solving separate problems.

What Are the Consequences of Getting Compliance Wrong?

Binance paid $4.3 billion to US regulators in 2023 for AML failures that had accumulated over years. The BitMEX founders faced criminal charges. Both were among the largest names in the industry at the time their enforcement actions began.

For smaller businesses, the consequences arrive faster and tend to be less survivable. A regulatory action that triggers a banking suspension can effectively close the business overnight. Most crypto companies maintain only a small number of banking relationships. Losing one over a compliance concern starts a cascade that is very difficult to reverse quickly.

The damage also happens before any formal enforcement begins. Institutional clients and enterprise partners run compliance due diligence before signing agreements. A business that cannot show a functioning AML program and appropriate licensing will not pass that review. That means lost revenue while the compliance gap still exists and no regulator has yet knocked on the door.

Under MiCA specifically, operating as a CASP without authorization exposes a business to fines of up to 15% of total annual turnover. That figure is calculated on revenue. The fine can exceed the actual profit from the unlicensed activity by a significant margin.

How Does Paybis Handle Compliance for Partners?

When a business integrates Paybis, the compliance infrastructure for the crypto layer is already in place and already licensed.

Paybis holds the MiCA CASP licence and the PSD2 Payment Institution licence, both granted by the Bank of Latvia in May 2026. That covers all 27 EU member states and the broader EEA. On top of that sits FinCEN registration in the US, FINTRAC registration in Canada, VASP registration in Poland, and FCA authorization in the UK. The full context is in the Paybis EU licensing announcement.

Partners using the Paybis on/off-ramp get KYC verification and AML monitoring handled on the Paybis side. The Corporate On/Off Ramp extends the same coverage to institutional and business clients, including KYB for corporate accounts. For businesses running payout operations, Paybis Send handles global crypto payouts under the same licensed framework.

Worth being clear on one point: integrating with a licensed partner does not transfer your compliance responsibility entirely. Your own operations outside the integration remain your own. What it does is remove the need to build and maintain the compliance infrastructure for the crypto layer independently. For businesses where crypto is a feature rather than the core product, that is a significant operational difference. The Paybis MiCA content hub covers ongoing regulatory developments and what they mean for platform operators.

Bottom Line

KYC, AML, and licensing are three separate layers of a compliance program, each with distinct requirements and distinct consequences for failure. Getting one right while neglecting the others does not produce a compliant business. The Binance settlement did not come from one bad decision. It came from years of systematic gaps across all three layers. That is how compliance failures actually accumulate, and it is why treating any one of these as a box to tick rather than a system to maintain is how businesses end up in the same conversation.

FAQ

What is the difference between KYC and AML in crypto?

KYC and AML are related but separate obligations. KYC establishes who your customers are and keeps that picture current as circumstances change. AML monitors what customers do with funds once they are on the platform and acts on patterns that suggest financial crime. A business with strong KYC but weak monitoring is collecting data it is not acting on. A business with strong monitoring but weak KYC is generating alerts without the context to investigate them properly. Both need to work for either one to be effective.

Do all crypto businesses need a licence, or just exchanges?

The licensing requirement depends on what the business actually does and where. Under MiCA, a CASP licence covers a wide range of services including exchange, custody, portfolio management, and crypto advice. The question regulators ask is not what the business calls itself but what it does operationally. If it holds customer funds, executes transactions on behalf of clients, or converts between crypto and fiat, it is almost certainly in scope for licensing in any major regulated jurisdiction.

Can I outsource KYC and AML to a third-party provider?

Yes, and many businesses do. Third-party verification tools and monitoring platforms are standard parts of the compliance stack. The important distinction is that outsourcing the function does not outsource the responsibility. If a third-party provider fails to meet the required standard, the business faces the regulator. Contracts with compliance vendors need to specify service levels, audit rights, and what happens when something goes wrong.

How does my compliance standing affect integration and partnership decisions?

Regulators assess the compliance standing of your infrastructure partners as part of evaluating your own risk. Integrating with an under-licensed provider creates counterparty risk that reflects on your own program. Before finalizing any integration that involves customer funds, request regulatory credentials, review the partner’s AML policy, and make sure the contract includes compliance representations that can be enforced if something goes wrong.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info