Crypto Licenses by Country: The Complete Global Guide

- A single MiCA CASP licence covers all 27 EU member states, with minimum capital ranging from €50,000 to €150,000 depending on services offered.

- The US requires FinCEN MSB registration plus separate Money Transmitter Licences in most states. New York’s BitLicense and California’s new DFAL (from July 2026) are exceptions with their own standalone regimes.

- The UAE’s VARA licence remains one of the most expensive to obtain, with capital requirements up to AED 1,500,000 (~$390,000) for exchange and custody services.

- Singapore’s MAS framework is thorough and slow, often taking 6 to 12 months, but it carries some of the strongest institutional credibility in Asia.

- Switzerland’s FINMA framework is considered one of the most stable and crypto-friendly in the world, with clear guidance dating back to its early ICO rules.

- Most operating exchanges hold two or three licences across their target markets rather than a single global authorization, because no single licence currently covers every major market.

Table of contents

- What Is a Crypto License and Why Does the Country You Choose Matter?

- What Does a Crypto License Cost and Require in the European Union?

- How Does Crypto Licensing Work in the United States?

- What Are the Requirements for a Crypto License in the UAE?

- How Strict Is Singapore’s Crypto Licensing Regime?

- Why Is Switzerland Considered the Most Stable Crypto Jurisdiction?

- What Other Jurisdictions Are Worth Knowing About?

- How Do You Actually Choose a Jurisdiction?

- How Does Paybis Fit Into a Global Licensing Strategy?

- Bottom Line

What Is a Crypto License and Why Does the Country You Choose Matter?

A crypto license is formal authorization from a financial regulator to provide cryptocurrency services legally within that regulator’s jurisdiction. For a fuller breakdown of what that authorization actually involves, the Paybis crypto license glossary entry covers the fundamentals.

The country matters because crypto licensing is not global. Each jurisdiction sets its own capital requirements, governance standards, and approval timelines. A licence from one country rarely grants automatic access to another.

There is one exception. In the EU, a single MiCA authorization covers all 27 member states through passporting. Outside the EU, the picture fragments quickly. A licence in Singapore says nothing about whether you can serve clients in the US. A US MSB registration means nothing in Dubai.

This creates a strategic decision for any crypto business:

- Where you license first shapes which markets you can serve

- How much capital you need to lock up depends entirely on jurisdiction

- How long the process takes varies from weeks to over a year

- What kind of banking relationships you can realistically build follows from both of the above

Getting that decision wrong is expensive. This guide walks through the major jurisdictions one by one, with the numbers that matter for each.

What Does a Crypto License Cost and Require in the European Union?

The EU runs the most unified crypto licensing system in the world. A single CASP authorization under MiCA, granted by any one national regulator, covers exchange, custody, advisory, and trading platform services across all 27 member states.

Capital requirements are set in three tiers under MiCA’s Article 67 and Annex IV:

- €50,000 for advisory and order reception services

- €125,000 for custody, exchange, and execution services

- €150,000 for operating a trading platform or trading on your own account

These figures are EU-wide minimums. The threshold is the same whether you apply through Lithuania, Ireland, Latvia, or any other member state.

What differs by member state is the speed and feel of the process. Lithuania has built a reputation for processing CASP applications efficiently, typically within 6 to 8 months, and has become a popular entry point for companies targeting the EU market. The Bank of Latvia has similarly developed a track record handling MiCA applications for international crypto businesses. Almost every member state now requires a resident director and a physical local office as part of the substance requirements that came with MiCA.

The transition deadline is firm. Companies that held national VASP registrations before MiCA had until July 1, 2026, to convert to full CASP status, provided they had applied by July 31, 2025. Miss that window and VASP status is lost immediately, with no fallback to the old registration regime.

For a deeper look at what the application process actually involves, the Paybis guide to getting a crypto licence in Europe covers the requirements, costs, and timeline step by step. The CASP glossary entry and the MiCA glossary entry both cover the underlying regulatory concepts in more detail.

How Does Crypto Licensing Work in the United States?

The US runs a two-layer system that catches many new applicants off guard.

Layer one: federal. Every crypto business handling exchange or money transmission must register with FinCEN as a Money Services Business. That registration alone takes one to two months and applies nationwide.

Layer two: state by state. Beyond federal registration, most states require a separate Money Transmitter Licence before a business can legally operate there. Obtaining an MTL can take anywhere from four to twelve months depending on the state, and the requirements differ state by state. A company with national ambitions in the US is realistically looking at dozens of separate state-level applications, not one.

Three states sit outside this pattern entirely:

- New York requires its own standalone BitLicense, a notoriously demanding and expensive authorization that has deterred many smaller applicants

- California introduces its Digital Financial Assets Law (DFAL) from July 1, 2026, creating a new dedicated framework specific to that state

- Montana also maintains its own distinct approach

Each of these three requires separate, specific attention rather than fitting into the general MTL pattern.

The SEC has also been active in 2026, releasing new guidance in March to clarify how different categories of crypto tokens are treated under securities law. For businesses involved in token issuance rather than pure exchange services, that guidance is worth tracking closely as the framework continues to develop.

What Are the Requirements for a Crypto License in the UAE?

The UAE has built one of the most structured and capital-intensive crypto licensing regimes outside the traditional Western frameworks, centred on Dubai’s Virtual Assets Regulatory Authority, known as VARA.

Capital requirements:

- AED 500,000 (around €130,000) for payment and transfer services

- AED 1,500,000 (around €390,000) for exchange or custody licences

If a single company wants to offer multiple categories of service, the capital requirement increases for each one. Beyond the headline figure, companies must hold reserve assets equal to the full value of their liabilities to clients. Under 2026 standards, they must also maintain net liquid assets equal to at least 1.2 times their average monthly operating costs.

The VARA process in 2026 runs in two stages. First comes an Approval to Incorporate, which covers operational setup. Second comes the full VASP Licence, known as the Full Market Product authorization. The earlier MVP licence stage that some companies used to enter the market is no longer the standard route for new applicants.

Free zones like IFZA and DSOA offer a faster, lighter path into the UAE market, but companies operating through them can only serve clients within that specific free zone. That limits the commercial upside considerably.

Outside Dubai specifically, Abu Dhabi Global Market operates its own framework through the Financial Services Regulatory Authority, giving businesses a second UAE pathway depending on where they want to be based.

How Strict Is Singapore’s Crypto Licensing Regime?

Singapore’s Monetary Authority of Singapore runs one of the most procedurally demanding licensing regimes in Asia, and that reputation is well-earned.

Capital requirements:

- SGD 100,000 for a Standard Payment Institution licence

- SGD 250,000 for a Major Payment Institution licence, which most serious crypto exchanges need

The application process involves several distinct stages:

- Register the company and secure a physical local office

- Write a detailed business plan, including an external auditor’s assessment of your technology and cybersecurity controls

- Designate a resident director and a local AML officer

- Submit the application with a fee in the range of SGD 1,000 to 1,500

From there, MAS assigns a case officer who conducts genuine due diligence, including verifying shareholders and the source of their wealth. Passing the regulator’s interview earns an In-Principle Approval. After that, the company sets up a local bank account, funds it with the required capital, and completes a final technology audit before the full licence is issued.

Retail crypto activities face tight restrictions under this framework, and the overall timeline runs long, frequently exceeding a year for new applicants.

What makes the effort worthwhile for many businesses is the credibility that comes with it. A MAS licence carries weight with banks and institutional partners across Asia-Pacific in a way that lighter offshore registrations simply do not.

Why Is Switzerland Considered the Most Stable Crypto Jurisdiction?

Switzerland’s reputation as a crypto-friendly jurisdiction predates most of the regulatory frameworks discussed in this guide. FINMA, the Swiss Financial Market Supervisory Authority, published clear guidance on crypto businesses and Initial Coin Offerings years before most regulators had formed a position at all.

Companies typically incorporate as a Swiss LLC or LTD, with required capital ranging from CHF 20,000 to 100,000 depending on the structure and the services involved. The canton of Zug, often referred to as Crypto Valley, became the geographic centre of this ecosystem and remains one of the most concentrated blockchain business hubs anywhere in the world.

Switzerland also offers a meaningful tax advantage for individuals. Private capital gains on crypto are taxed at 0% for personal holders, which has made the country attractive to founders and investors as well as companies.

On the banking side, dedicated crypto-friendly banks like Sygnum and SEBA give Swiss-licensed businesses banking access that is considerably harder to secure in many other jurisdictions, where traditional banks remain hesitant to onboard crypto companies even once they are licensed.

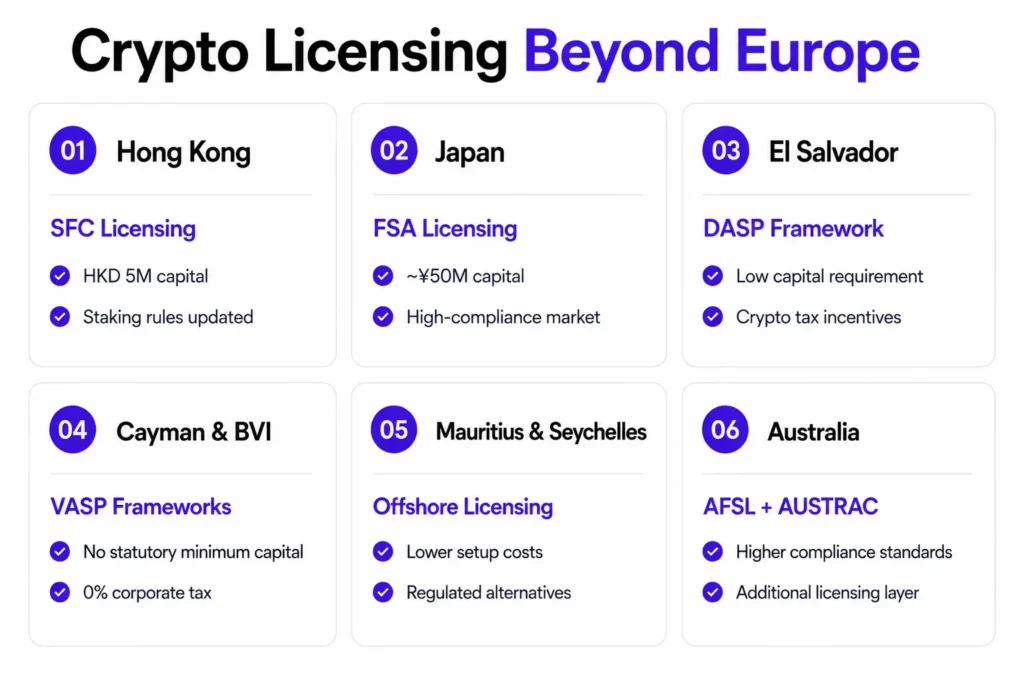

What Other Jurisdictions Are Worth Knowing About?

Beyond the major frameworks above, several other jurisdictions show up consistently in 2026 licensing discussions, each for different reasons.

- Hong Kong runs a licensing regime through the Securities and Futures Commission for Virtual Asset Trading Platforms. Capital required: HKD 5 million paid-up plus HKD 3 million in liquid assets The SFC tightened its guidance in 2026, including new rules covering staking services

- Japan’s Financial Services Agency requires capital of roughly ¥50 million, around $350,000. That makes it one of the more capital-intensive jurisdictions in Asia alongside Singapore.

- El Salvador sits at the opposite end of the cost spectrum. Licensed entities under its Digital Asset Service Provider framework benefit from exemptions on corporate income tax and VAT for qualifying crypto activities. The minimum capital required can be as low as a few thousand dollars, making it one of the most accessible jurisdictions for early-stage companies testing a business model before committing to a more expensive licence elsewhere.

- Cayman Islands and the British Virgin Islands both operate under VASP Act frameworks with no statutory minimum capital requirement and 0% corporate income tax for licensed entities. They remain popular for institutional structures, hedge funds, and prime brokerage operations that value the combination of genuine regulatory oversight with offshore tax efficiency.

- Mauritius and Seychelles offer lower-cost offshore alternatives. Mauritius operates under its VAITOS Act, while Seychelles runs a dedicated VASP Act introduced in 2024. Both provide real regulatory oversight at a fraction of the cost of EU or Singapore licensing. The trade-off is a smaller addressable local market and more limited banking options.

- Australia has moved toward a higher-compliance model. Platforms handling significant trading volume now need an Australian Financial Services Licence on top of AUSTRAC registration, reflecting the same global trend toward tighter oversight that the EU and Singapore have already gone through.

How Do You Actually Choose a Jurisdiction?

There is no universally correct answer here. The right jurisdiction depends entirely on the specific business model, the target customer base, and the capital available to deploy toward licensing.

A few practical patterns hold consistently across the industry:

- EU market reach and institutional credibility: MiCA, applied through an efficient member state like Lithuania or Ireland

- Middle East customer flow: VARA in Dubai or ADGM’s FSRA framework

- Asia-Pacific: Singapore’s MAS framework weighed against Hong Kong’s SFC regime, depending on which regional market matters more

- US dollar customers: FinCEN MSB registration plus a realistic state-by-state MTL rollout, with specific attention to New York and California

Most operating exchanges end up holding two or three licences across their target markets rather than betting everything on one. A company might combine an EU CASP licence for European reach, a US MSB registration with select state MTLs for American customers, and an offshore structure for operational flexibility. Planning for that multi-jurisdiction reality from the start, rather than discovering it midway through a single licensing process, saves significant time and cost.

Banking deserves equal weight in the decision. A licence without a workable banking relationship is close to useless operationally. Most regulator-acceptable banks will not even take an introductory call without a draft application or a letter of intent already in hand. Banking conversations need to start alongside the licensing process, not after the licence is granted.

How Does Paybis Fit Into a Global Licensing Strategy?

For businesses still working through their own licensing process, or businesses that have decided a direct licence in every target market is not the right path, partnering with an already-licensed infrastructure provider is a practical alternative.

Paybis holds the MiCA CASP licence and the Payment Institution licence under PSD2, both issued by the Bank of Latvia in May 2026, covering all 27 EU member states and the broader EEA. Alongside that EU authorization, Paybis holds FinCEN MSB registration in the US, FINTRAC registration in Canada, VASP registration in Poland, and FCA authorization in the UK. That regulatory footprint is what businesses can point to when their own partners or regulators ask about counterparty due diligence.

The Paybis on/off-ramp gives businesses a way to offer crypto buy, sell, and swap functionality to their customers through a licensed integration, without holding a licence of their own in every market served. The Corporate On/Off Ramp extends that same licensed infrastructure to institutional clients needing direct fiat and crypto liquidity, with KYB and AML handled on the Paybis side. For businesses running payout operations globally, Paybis Send covers crypto payouts under the same licensed framework.

The crypto exchange regulations guide covers what licensed platforms must maintain on an ongoing basis once a licence is in place, and the Paybis MiCA content hub tracks regulatory developments as the EU framework continues to evolve.

Bottom Line

Crypto licensing in 2026 is a genuinely global patchwork, and no single authorization covers every market a growing business might want to serve. The EU’s MiCA framework offers the broadest single-licence coverage available anywhere, spanning 27 countries through one CASP authorization. The US requires federal MSB registration alongside a state-by-state Money Transmitter Licence rollout. The UAE and Singapore offer strong institutional credibility at a meaningfully higher capital cost. Switzerland remains the benchmark for regulatory stability. Offshore jurisdictions like the Cayman Islands, El Salvador, and Mauritius offer faster, cheaper entry points for businesses not yet ready for the cost of a Tier-1 licence. Most serious operators end up holding several licences across their target markets, planned and sequenced together rather than pursued one at a time as an afterthought.

FAQ

Which crypto license is best for a business with global ambitions?

There is no single licence that covers the world. A MiCA CASP licence covers the EU and EEA, which is the closest thing to a multi-country passport that currently exists in crypto licensing. Outside the EU, a business with global ambitions typically needs to combine a US MSB registration with relevant state MTLs, a MiCA CASP licence for Europe, and either a UAE or Singapore licence for its respective region, depending on where the customer base is concentrated. Most exchanges operating at real scale hold several licences simultaneously rather than relying on one.

How much does it cost to get a crypto license in 2026?

Costs vary enormously by jurisdiction. On the low end, a Panama corporate setup or an El Salvador DASP licence can cost a few thousand to around $30,000. On the high end, a New York BitLicense with full surety bond and substance requirements can exceed $1.5 million. For an institutional-grade licence in a major jurisdiction like the EU, UAE, or Singapore, the median first-year cost typically runs between $250,000 and $500,000 once legal fees, substance requirements, and paid-up capital are included. Annual ongoing costs after the first year typically run 30 to 50% of that initial figure.

How long does it take to get a crypto license?

Timelines range from a few weeks for some offshore registrations to 18 months or more for the most demanding frameworks. Singapore’s MAS process frequently exceeds a year. The UK’s FCA registration typically takes 9 to 12 months. MiCA CASP applications in efficient EU jurisdictions can complete in 6 to 8 months with a well-prepared application, though the statutory review period itself is only 25 working days once an application is deemed complete. UAE VARA licensing timelines vary by stage and licence type. Building in buffer time for completeness checks and follow-up information requests is essential when planning any jurisdiction’s timeline.

Do I need a license to operate a DeFi protocol?

As of 2026, fully decentralized DeFi protocols with no identifiable operator largely escape direct licensing requirements in most jurisdictions, including under MiCA. However, regulators are increasingly scrutinizing the on-ramps and off-ramps that connect DeFi to fiat currency. Staking services, yield platforms, and exchange-operated DeFi offerings frequently do require a VASP or CASP licence depending on the jurisdiction. The regulatory trend points toward AML rules eventually reaching protocol operators more directly, so a DeFi-adjacent business should not assume the current light-touch treatment is permanent.

What happens if I operate without the correct crypto license?

The consequences compound over time rather than appearing all at once. In the near term, an unlicensed business risks bank account freezes, outright refusals from financial institutions, and being excluded from Travel Rule networks that licensed Virtual Asset Service Providers use to exchange compliance information with each other. Over time, unlicensed operators increasingly find themselves shut out of partnerships, institutional client relationships, and major markets entirely, since regulated counterparties are required to perform due diligence that an unlicensed business simply cannot pass. Regulatory enforcement varies by jurisdiction but increasingly includes direct fines on top of these structural disadvantages.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info