Merchant Crypto Settlement for iGaming: Operator Revenue Payouts Beyond Affiliate Commissions

Key Takeaways:iGaming operators are increasingly evaluating API-driven stablecoin settlement as an alternative execution layer for cross-border merchant and partner payouts, particularly for revenue-share models. This approach can streamline multi-party distributions and improve settlement speed and transparency compared to legacy banking rails, though actual performance depends on liquidity, network conditions, and compliance screening. Operators remain responsible for KYB, regulatory obligations, and payout governance when using such infrastructure.

Crypto assets can increase or decrease in value. Paybis is a payment gateway, not an investment service. This content is for informational purposes only and does not constitute financial advice.

The biggest threat to your iGaming platform’s margin isn’t player acquisition costs. It’s the hidden FX spreads and rolling reserves embedded in legacy payout infrastructure. On a $10,000 settlement, a single international wire can cost $40-$65 or more in base fees, with intermediary charges and FX markups pushing all-in costs significantly higher per transaction. Across hundreds of monthly merchant settlements, that drag is structural.

Traditional banking classified gambling as high-risk and imposed arbitrary restrictions, elevated fees, and frequent transaction blocks. Operators can no longer rent financial rails designed to exclude them. This guide breaks down how API-driven crypto settlement infrastructure eliminates that dependency, automating multi-tier merchant and revenue-share payouts at a fraction of traditional SWIFT wire costs.

What Is Merchant Crypto Settlement for iGaming Operators?

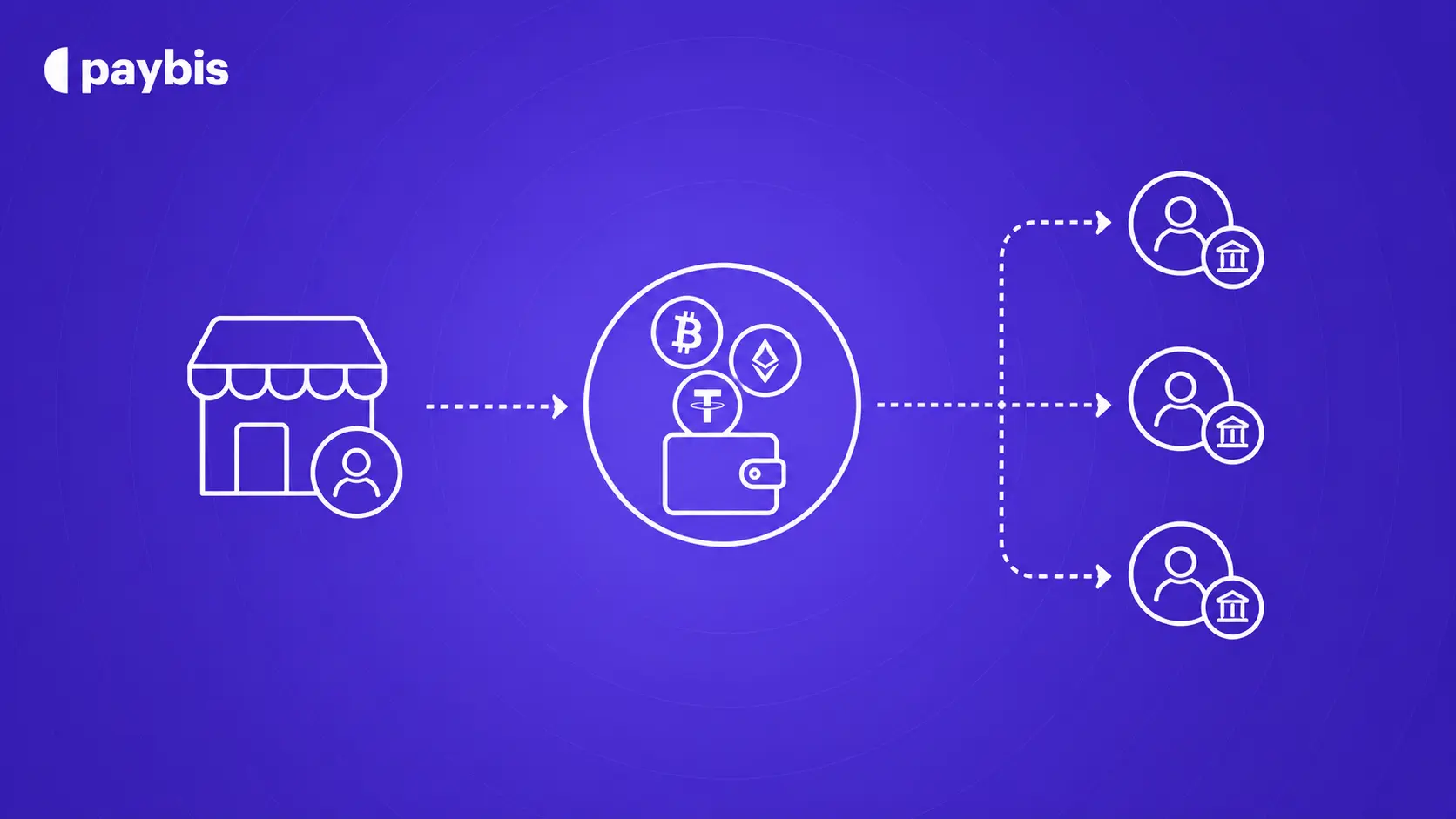

Merchant crypto settlement is defined as the automated disbursement of Net Gaming Revenue to business counterparties using crypto rails. This is distinct from player withdrawals. It carries a different compliance profile, fee structure, and operational complexity, and it is the architecture iGaming’s most competitive operators are building right now.

Operator Revenue: Settlement vs. Commissions

Net Gaming Revenue (NGR) is the foundation of every operator-to-merchant payout: Gross Gaming Revenue (bets minus wins) minus bonuses, fees, taxes, and contractually defined deductions. In a Cost Per Action (CPA) affiliate model, a fixed payment triggers once per referred deposit. Revenue share is different: ongoing, variable, and tied directly to NGR performance.

For operators running multi-merchant models, a single NGR pool feeds multiple recipients simultaneously: a game studio receives a negotiated percentage on their title, affiliate revenue shares typically range from 25% to 45%+ of NGR, with specific terms set by contract, and a white-label merchant hosting the product takes another percentage. That single pool requires multiple coordinated, correctly sequenced payouts every settlement period.

Identifying Crypto Settlement Entities

The recipient universe for merchant settlements is broader than most operators’ payout systems handle:

- Game studios: Revenue share on NGR generated by licensed titles

- White-label merchants: Platform licensing fees plus performance bonuses

- Sub-affiliates: Cascading commission splits from top-tier affiliate agreements

- Content creators and streamers: Performance-based fees tied to player acquisition volume

- Software providers: API usage fees and integration revenue shares

Each entity type carries distinct KYB requirements, preferred settlement currencies, and payout threshold preferences. Infrastructure built for monthly affiliate commissions breaks under this load.

iGaming Merchant Settlement: Why Crypto?

The operational case for crypto settlement in B2B iGaming payouts comes down to three measurable advantages. Because stablecoin payouts via direct API infrastructure bypass the high-risk payment processor layer, operators remove the primary mechanism through which rolling reserves are imposed. Chargebacks drop to zero on confirmed blockchain transactions. Cross-border settlement compresses from three to five business days to under two minutes on Polygon or Solana.

Take rate protection starts with understanding what “net received” means for B2B payouts. Most legacy providers advertise a fee percentage while embedding additional margin in the FX spread applied at conversion. An operator sees a 1.5% stated fee and discovers post-launch that the FX markup added another 2-4% on top.

For a €10,000 settlement, Paybis Send’s 0.49% base rate results in €49 in fees, plus less than €0.01 in Polygon network costs. By comparison, a traditional international wire of the same size can cost approximately €300–€800 in total once FX markups, intermediary banking charges, and transfer fees are included. The cost difference compounds significantly across hundreds of monthly settlements.

Crypto Payout Thresholds for Operators

Network fees make micro-payouts economically irrational without minimum thresholds. The math is straightforward using Polygon, where fees run under $0.01 per transaction:

- Without thresholds: 1,000 payouts of $10 each at $0.002 Polygon fee = $2.00 total network cost

- With $100 threshold: 100 payouts of $100 each at $0.002 = $0.20 total network cost

The principle scales regardless of chain: fewer, larger payouts reduce per-dollar network overhead. For operators processing high volumes of small partner payments, configuring minimum thresholds before execution delivers meaningful margin recovery with a single API configuration change.

Fixed-Cadence iGaming Revenue Payouts

Scheduled payouts reduce reconciliation complexity but increase merchant dissatisfaction when NGR calculates weekly but settles monthly. Real-time settlement is operationally superior but requires infrastructure that processes payouts outside banking hours, including weekends and holidays.

The pre-funded virtual IBAN model solves this directly. With fiat held in a company-named IBAN and conversion happening at the moment of each payout API call, you can execute settlements at any time without dependency on banking clearance windows. A game studio in Southeast Asia receives their Wednesday NGR share on Wednesday, not the following Monday.

Implementing Multi-Tier Payout Models

Multi-tier settlement requires API logic that splits a single revenue pool across multiple stakeholders simultaneously. No smart contract deployment is required. The split logic lives in your system. Paybis executes and confirms each leg independently. The architecture:

- NGR calculation: Your system computes NGR per game, per merchant, per sub-affiliate tier for the settlement period

- Rule evaluation: API logic applies configured percentage splits and thresholds per recipient

- Batch execution: A single API call dispatches multiple payouts to different wallet addresses in different cryptocurrencies

- Webhook confirmation: Real-time status updates confirm each payout leg, enabling automated reconciliation

Distributing Crypto to Tiered Partners

Configuring Direct Merchant Payouts

Paybis Send was built to execute this architecture directly. You pre-fund a virtual IBAN issued under your company name in USD, EUR, or GBP. When your payout API call fires, it converts the specified fiat amount to the merchant’s preferred cryptocurrency at the locked quote rate and transfers it to their wallet address in near-real time. No need to hold crypto on your balance sheet. No exposure to BTC or ETH price movements between funding and disbursement.

The API flow follows a quote-then-execute model: your system screens the recipient wallet address for AML compliance, requests a real-time conversion quote, submits the payout against the locked quote, and the transfer executes to the merchant’s wallet. The webhook delivers real-time confirmation of each transaction status, feeding directly into your reconciliation system. For operational resilience, the API supports idempotency keys (unique request identifiers that tell the system a payout has already been submitted), which prevent duplicate payouts when retry logic triggers after a failed call.

When a payout fails, whether from an invalid wallet address, AML flag, or insufficient vIBAN balance, Paybis API returns a specific error code, and the webhook delivers a failure status immediately. Your system logs the error, alerts your finance team, and either retries automatically or routes to manual review based on your configured logic.

Sub-affiliate cascades present the hardest reconciliation challenge in manual payout systems. Without API automation, the operator either manages this manually (expensive, error-prone) or leaves reconciliation to the top-tier affiliate (opaque, trust-eroding).

API-driven infrastructure allows you to configure sub-affiliate splits directly. When the top-tier affiliate NGR is calculated, your system automatically computes each sub-affiliate’s entitlement and dispatches individual payouts. No manual intervention. No batch file uploads. An audit trail is maintained at the transaction level for each leg, as detailed in our affiliate payout support documentation.

Customize Payout Hierarchy Levels

Effective hierarchy customization requires three API-layer capabilities:

- Partner ID tagging: Unique identifiers for each merchant, affiliate, and sub-affiliate in the API call

- Currency preference storage: Per-partner default cryptocurrency and network

- Override logic: The ability to override the default currency on a per-payout basis, such as a merchant requesting 50% USDC and 50% EUR for a specific settlement period

Accelerate Crypto Payouts: Optimize Frequency

Daily vs. Weekly vs. Monthly Settlement

Settlement frequency directly affects merchant retention and your working capital requirements:

- Monthly: Lowest operational overhead, highest merchant dissatisfaction, highest FX exposure during NGR accumulation

- Weekly: Balanced for mid-tier partners, requires reliable API automation

- Daily: Strongest retention signal, near-zero FX exposure window, requires pre-funded vIBAN balance sufficient for peak daily volume

Transaction Cost per Settlement Event

Batch processing makes daily settlement economically viable. Dispatching 100 merchant payouts on Polygon simultaneously incurs network fees per transaction leg at under $0.01 each, totaling under $1.00 for the full batch. The same 100 payments via SWIFT would cost $2,500-$5,000 in wire fees alone, excluding FX spread.

Retain Merchants with Faster Payouts

Payout speed functions as a merchant acquisition and retention mechanism. Game studios with multiple operator relationships allocate their newest titles and promotional inventory to the operator whose infrastructure makes them feel most valued. Platforms running weekly or monthly settlement on legacy fiat rails are competing against API-driven operators who settle daily via stablecoin. That is not a marginal difference in merchant experience.

Defining Tiered Payout Batch Rules

Effective batch configurations include:

- Time-zone batching: Execute during off-peak network hours (01:00-06:00 UTC) to minimize Ethereum L1 gas spikes for high-value payouts

- Congestion-aware routing: Route to Polygon or Solana during Ethereum congestion events rather than paying elevated gas fees

- Balance-triggered batching: Delay execution until the vIBAN balance exceeds the total batch payout value plus a buffer for conversion rate movement

API Integration for Automated Payouts

The technical requirements for a production-grade mass payout integration are well-defined. The core flow covers wallet address AML screening, real-time conversion quoting, payout execution, and webhook-based status delivery for reconciliation. Refer to the Paybis API documentation for current endpoint names and parameters.

Webhooks are non-negotiable for reconciliation at scale. Without webhook confirmation, your finance team manually checks payout status against blockchain explorers for each transaction leg. At hundreds of monthly payouts across 50+ merchants, that overhead is unacceptable. Webhook-driven reconciliation triggers automatic ledger updates the moment each payout confirms on-chain.

You access transaction data three ways: real-time via webhook for automated reconciliation, batch CSV export from the partner dashboard for monthly finance close, or on-demand via the API filtered by date range, recipient, or transaction status.

Infrastructure for Payout Partner Setup

Table 1: Self-Hosted vs. Managed API Infrastructure

| Capability | In-House Build | Paybis Send |

|---|---|---|

| Software Development Kit (SDK) availability | Requires internal development | Web, iOS, Android SDKs |

| Webhook support | Custom-built system | Native, documented |

| Compliance offload | None | KYC, AML, address screening |

| Multi-jurisdiction licensing | Build per market | Inherited (MiCA, CASP, FinCEN, VASP) |

| Time to first live payout | Months to over a year | Varies by integration and compliance review: can be shorter |

| Rolling reserve | May apply via banking partners | Varies by risk and account setup |

| FX Spread | 2–4% typical | Confirm with sales |

KYC and AML Obligations by Jurisdiction

The Markets in Crypto-Assets Regulation (MiCA) came into full effect on 30 December 2024, requiring all crypto-asset service providers in the EU to obtain Crypto-Asset Service Provider (CASP) authorization from their national competent authority. Payment Services Directive 3 (PSD3), expected to apply around 2027 to 2028, is set to consolidate payment and e-money services under a single framework, extending obligations to payment service providers.

When you use Paybis as your settlement infrastructure, Paybis handles: per-transaction wallet address AML screening, sanctions list checks, ongoing transaction monitoring for velocity and pattern anomalies, and regulatory reporting for its VASP obligations. Your team retains responsibility for: collecting and validating merchant business registration documents, performing UBO due diligence for partners above applicable MiCA thresholds, maintaining partner KYB documentation for audits, and reporting suspicious activity if a merchant’s transaction pattern changes materially.

Eliminate Single Points of Failure

For B2B payouts, the single point of failure is the pre-funded balance account. If your settlement provider experiences an outage or a compliance freeze, every scheduled payout stops until resolution.

The mitigation: configure dual-provider settlement with automated failover logic. Your primary settlement flow runs through Provider A. If an API call fails or times out, your system automatically routes the payout batch to a secondary provider with minimal manual involvement, based on your configured runbook and approval thresholds. Paybis supports this model via the API’s idempotency keys, which prevent duplicate payouts when failover logic triggers. For operators processing significant weekly volume in merchant settlements, this architecture prevents a single-provider event from blocking all partner payouts simultaneously.

Crypto Settlement Data Accuracy

Finance teams require transaction-level audit trails for every payout leg. Minimum data requirements for a compliant reconciliation system:

- Transaction hash per payout (on-chain verifiable)

- Fiat amount at time of conversion and locked exchange rate

- Recipient wallet address and cryptocurrency

- Timestamp of execution and blockchain confirmation

- AML screening result per recipient address

This data architecture satisfies both MiCA and the EU’s Transfer of Funds Regulation (TFR), which requires originator and beneficiary data to accompany all CASP-to-CASP crypto-asset transfers regardless of amount.

Optimizing Net Received for iGaming Operators

Network Fees by Blockchain and Volume

Blockchain selection for mass payouts is a cost engineering decision. The current fee landscape:

- Solana: Typically under $0.01 per transaction (fees vary by network conditions), ~400ms confirmation, best for high-frequency small payouts

- Polygon: Typically under $0.01 per transaction (fees vary by network conditions), 30 seconds-2 minutes confirmation, optimal for volume above 1,000 monthly payouts

- Ethereum L1: $0.40-$5+ per transaction during normal conditions, 12-30 seconds, reserved for high-value enterprise settlements where percentage cost is negligible

- Arbitrum/Optimism (L2): $0.10-$0.50 per transaction, 2-5 seconds confirmation, suited to Ethereum-native apps with mid-range volumes. Both are Layer 2 networks, meaning they process transactions on top of Ethereum to deliver faster throughput and lower fees than the Ethereum base network.

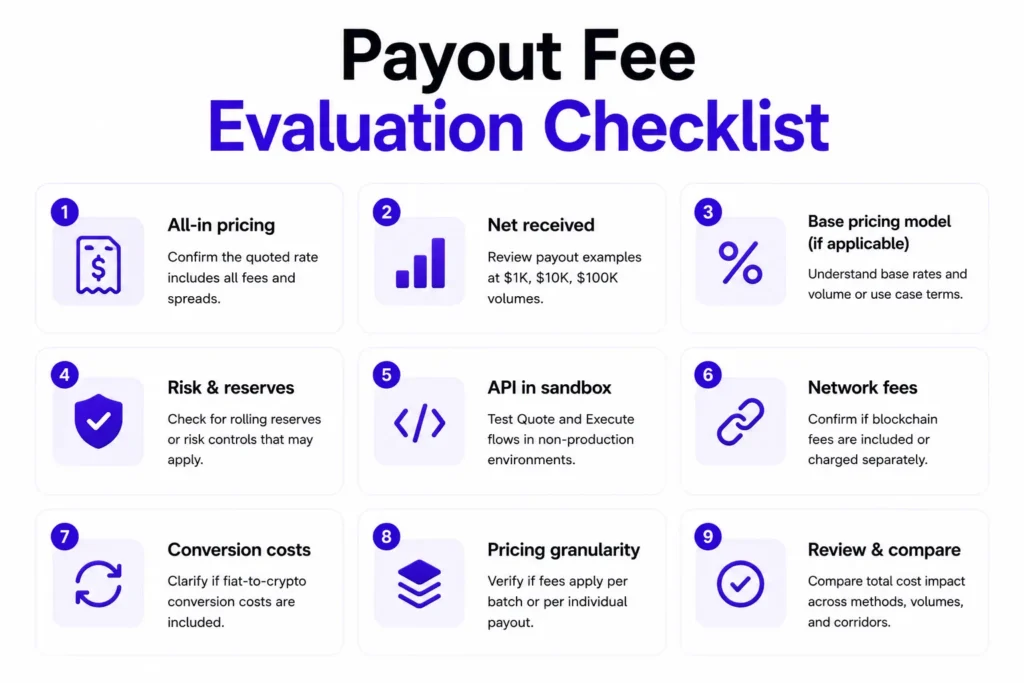

Payout Fee Evaluation Checklist

Use the following checklist when evaluating a payout infrastructure provider:

- Confirm all-in pricing structure: Ensure the quoted rate reflects total applicable fees, including any spreads where relevant, not only the base service fee.

- Validate net received outputs: Review example payout amounts at different volumes (e.g., $1,000, $10,000, $100,000) to understand expected recipient value.

- Review base pricing model (where applicable): Some providers may apply a standard base rate for B2B flows, with additional commercial terms depending on volume and use case.

- Check risk and reserve policies: Confirm whether any rolling reserves or similar risk controls may apply based on classification or settlement structure.

- Test API behavior in sandbox environments: Validate Quote and Execute flows in non-production environments before relying on production assumptions.

- Confirm network fee handling: Understand whether blockchain network fees are included in pricing or treated separately at execution time.

- Clarify conversion cost structure: Review whether fiat-to-crypto conversion costs are included in the quoted rate or applied separately.

- Understand pricing granularity: Confirm whether fees apply per transaction batch or per individual payout within a batch structure.

Choosing Stablecoin vs. Native Payouts

The volatility concern around crypto settlement is valid for merchant payouts denominated in assets like BTC or ETH, but stablecoins operate differently because they are designed to maintain price stability relative to fiat currencies.

Stablecoins offer several operational advantages over traditional wire transfers, including faster settlement, lower transfer costs, and easier integration into automated payment infrastructure. A merchant receiving USDC can hold a dollar-pegged asset immediately without needing to convert funds to reduce volatility exposure.

For revenue share agreements denominated in fiat currencies, stablecoins can simplify cross-border settlement while reducing banking friction. USDC (USD Coin, a regulated stablecoin pegged to the US dollar) is commonly used in markets prioritizing regulated dollar-denominated settlement, while USDC remains widely adopted across regions where stablecoin accessibility and liquidity are a priority.

Mitigating Regulatory Risk in Crypto Payouts

Managing VASP for Merchant Crypto Payouts

Obtaining CASP authorization in one EU member state typically takes 4-6 months. According to regulatory licensing advisors, building multi-jurisdiction coverage independently compounds that timeline across each market.

MiCA now governs EU-facing crypto-asset services, including merchant payout transfers.

MiCA now governs EU-facing crypto-asset services, including merchant payout transfers. As the framework takes effect across the EU, providers operating in member states are expected to align with CASP authorization requirements established by national competent authorities, either directly or through regulated partners.

Paybis operates under MiCA CASP authorisation from the Bank of Latvia, which passports across all 27 EU member states, and a PSD2 Payment Institution licence from the Bank of Latvia. It also maintains FinCEN MSB registration in the United States, FINTRAC registration in Canada, and VASP registration in Poland (RDWW-805).

When used as settlement infrastructure, Paybis provides operators with access to an already-licensed framework across these regions, reducing the need for operators to pursue separate licensing pathways before integrating payout functionality.

Business counterparty onboarding (KYB) sits with the operator regardless of which settlement infrastructure you use. Standard KYB documentation for merchant and affiliate onboarding includes:

- Certificate of Incorporation

- Beneficial Ownership Declaration (UBO with over 25% ownership)

- Proof of Business Address (dated within 90 days)

- Director identification documents (government-issued photo ID and proof of residential address)

- Source of Funds declaration for high-volume partners

KYB collection should be integrated into your partner onboarding portal with document upload, validation, and encrypted storage, not managed via email. This maintains audit trails and reduces processing time at scale.

Crypto Payout Tax Obligations and Regulatory Traceability

Tax reporting obligations for crypto payouts vary by jurisdiction but share a common requirement: accurate, timestamped transaction records with fiat-equivalent values at the moment of settlement. EU operators face additional obligations under the EU’s Directive on Administrative Cooperation 8 (DAC8), which requires crypto-asset service providers to report transactions involving EU-resident clients to relevant tax authorities.

The TFR requires originator and beneficiary information to accompany all CASP-to-CASP crypto-asset transfers in the EU regardless of amount. A separate €1,000 threshold applies specifically to the self-hosted wallet ownership-verification step, where CASPs must obtain and verify additional information when a transfer involves an unhosted wallet above that value. Paybis’s compliance engine handles address screening and AML monitoring at the infrastructure level, but your system must supply the merchant KYB data required for TFR compliance on each payout leg.

How Do Threshold-Triggered Payouts Reduce Costs?

Threshold logic holds accumulated NGR for a specific merchant until the balance crosses a pre-configured minimum before executing the payout. On Polygon, where network fees run under $0.01 per transaction, the cost difference between 30 daily micro-payouts and one consolidated monthly payout is real but modest. On higher-fee chains or for operators processing thousands of micro-payouts, the consolidation effect is more material: the same network fee covers one payout of $500 as covers one of $5.

The key design principle: tier your threshold logic by partner value. High-value game studio relationships typically warrant daily settlement cadences, subject to cash flow requirements and risk configuration. Mid-tier merchants commonly operate on weekly settlement cycles, though the appropriate cadence depends on cash flow requirements and risk profile. Lower-volume partners accumulate NGR until the balance crosses the configured minimum threshold, at which point the payout executes automatically. This structure preserves the merchant experience where it matters most while recovering margin at the tail.

iGaming Partner KYC Details

For lower-volume sub-affiliates, KYB requirements depend on the applicable regulatory jurisdiction and payout provider compliance obligations, but at minimum include AML and sanctions screening to confirm recipient identity. Paybis validates the recipient’s wallet address format and runs AML compliance checks before any funds move, so non-compliant addresses are caught before the payout executes. The Paybis Send business payout documentation covers the wallet validation and onboarding flow in detail.

Configuring Unique Merchant Payout Rules

Edge cases in revenue share agreements are common. A merchant may want 50% of their monthly NGR share in USDC and 50% converted to EUR via bank transfer. Another may require payouts held until a specific date regardless of threshold.

The Send API supports cryptocurrency-level customization on a per-payout basis. For split-currency arrangements, the system executes two separate API calls per merchant payout period: one for the crypto payout via Send and one for the fiat payout via the Fiat Payouts product. Both calls should be tagged with a shared internal reference ID linked to the NGR calculation for the relevant settlement period, ensuring reconciliation treats them as a single logical payout event.

Reducing Crypto Settlement Lag

Settlement lag in traditional payout infrastructure stems from two sources: banking clearance cycles (1-5 days for wires) and manual review queues (24-48 hours for high-value payouts). Pre-funding a vIBAN eliminates both. The pre-funded fiat balance sits in a dedicated IBAN under your company name. When the payout API call fires, Paybis converts at the locked quote rate and dispatches the crypto to the merchant’s wallet via blockchain, 24/7. Blockchain confirmation on Polygon or Solana takes seconds to minutes. Banking hours are no longer a constraint on your settlement schedule.

Test Paybis Send before going live. Request API credentials, validate payout flows at your target volume tier, and confirm net received outputs before moving to production. Timelines vary based on compliance requirements and integration scope. Get sandbox access or contact our B2B team for volume-based pricing.

Key Terminology

- Net Gaming Revenue (NGR): The revenue base used to calculate operator-to-merchant payout amounts, equal to Gross Gaming Revenue minus bonuses, transaction fees, taxes, and other contractually defined deductions. Every revenue share settlement amount derives from this variable.

- AML (Anti-Money Laundering): A set of controls and procedures used to detect and prevent the use of financial systems for illicit activity, such as money laundering or terrorist financing.

- Infrastructure Inversion: The structural shift forcing iGaming operators to own or outsource their financial settlement rails rather than rent legacy banking infrastructure that classifies gambling as high-risk and imposes rolling reserves, restrictions, and elevated fees.

- Net Received: The actual amount received by the settlement recipient after all fees, spreads, and conversion costs are applied. The only reliable metric for comparing payout provider costs, since stated fee percentages exclude embedded FX spread.

- KYC (Know Your Customer): The process of verifying the identity and business details of clients to assess risk and comply with regulatory requirements.

- Authorization hold: A temporary hold placed on funds during a payment or transaction to confirm availability before final settlement or capture.

- VASP (Virtual Asset Service Provider): A regulatory designation for businesses handling crypto-asset exchange, transfer, or custody on behalf of others.

FAQ

What Is the Maximum Number of Recipients in a Single Paybis Send API Batch Call?

Batch recipient limits depend on your integration configuration and account tier. For confirmed limits applicable to your volume, consult the Paybis API documentation or request specifics from the B2B team during onboarding. Pre-production testing options and supported cryptocurrencies are confirmed during the integration and onboarding process with the B2B team.

What Is Paybis's Base Rate for B2B Merchant Payouts?

B2B partner rates start at 0.49% per transaction. Custom volume-based pricing requires a sales conversation for operators exceeding defined monthly payout thresholds.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info