Building Payout Redundancy: Multi-Acquirer Strategies and Failover Logic

Key Takeaways:Payment orchestration uses multi-acquirer cascade routing to eliminate single points of failure in payout infrastructure. With 2-5 backup acquirers, failed transactions are retried based on region, BIN, cost, and historical performance. Smart Cascade Routing with 3DS decoupling ensures authentication happens once, improving authorization rates by 11%+. Paybis provides this infrastructure with 150+ PSP integrations, covering 180+ countries, 22 payment methods, and 90+ cryptocurrencies, with $1.2B+ in annual transaction volume (as of Oct 2025).

Crypto assets can increase or decrease in value. Paybis is a payment gateway, not an investment service. This content is for informational purposes only and does not constitute financial advice.

Most product teams obsess over checkout UI while ignoring transaction declines at the acquirer level, a failure point that compounds when there is no secondary routing to catch them. Payment system disruptions cost $44.4 billion in U.S. retail and hospitality sales annually, with the average outage lasting two hours and consumers abandoning purchase attempts within seven minutes.

Single-acquirer payout systems are a liability that costs platforms gross payment volume (GPV). Implementing multi-acquirer cascade routing with 3DS decoupling is the most reliable path to payout resilience and margin protection at scale. This guide covers the exact technical framework.

Single Payout Provider Dependency Risks

Relying on one PSP means every upstream failure, policy change, or banking relationship shift becomes your problem immediately and without warning.

Lost GPV from Payout Failures

Authorization declines account for a significant share of attempted purchases globally, with e-commerce seeing materially higher rates. The damage compounds quickly: 70% of declined orders come from customers with sufficient credit limits and valid payment credentials, meaning the loss is not fraud prevention doing its job. It is infrastructure failing good customers.

When a decline happens and there is no retry logic, the session ends. That customer rarely returns for the same transaction. At any meaningful GPV volume, a persistent single-digit decline rate for a single acquirer represents a recurring revenue leak that grows in proportion to scale.

Partner Exits and Sanction Risks

Acquiring banks drop crypto and fintech clients without contractual notice. A single relationship termination can take an entire payment rail offline overnight.

Evaluating a provider’s financial stability and regulatory track record before integration is not optional. Registration with bodies such as FinCEN and FINTRAC, VASP registration, and EU authorisation are the verification checkpoints worth confirming. Paybis operates under MiCA CASP authorisation from the Bank of Latvia, which passports across all 27 EU member states, and a PSD2 Payment Institution licence from the Bank of Latvia. It also holds FinCEN registration (US), FINTRAC registration (Canada), VASP registration in Poland (RDWW-805), and FCA registration (UK). Partners operate under that coverage for covered flows from day one rather than building it independently.

Settlement Delays and Liquidity Gaps

IT disaster recovery and payment gateway failover solve different problems. DR plans handle infrastructure outages at the server and network layer. Payment failover handles scenarios where the processor is operational but declining transactions at elevated rates due to BIN-level risk flags or regional acquirer pressure.

A platform with 99.9% infrastructure uptime can still lose transactions if its single acquirer underperforms on specific card ranges or geographies. Resilient payment systems require redundancy at the acquirer layer, not just the infrastructure layer.

Structuring Your Multi-Acquirer Payouts

Eliminating single-provider risk requires configuring 2-5 acquirers in a cascade routing setup that automatically retries failed transactions based on cost, region, and BIN-level performance.

Configuring Acquirer Failover Logic

Industry best practice typically involves maintaining multiple PSPs integrated into your system, providing both competitive processing rates and a failsafe when any single processor becomes unavailable during authorization. A robust production setup commonly uses 2-5 acquirers in a cascade configuration.

57% of merchants currently use multi-acquiring strategies across payment verticals, and 40% of those still working with a single acquirer plan to change that within the next year. When the primary acquirer returns a decline, the orchestration layer routes the transaction to the next configured acquirer based on cost, regional performance, and historical approval rates for that specific BIN range.

Boost Authorization Rates via Diversified Processing

Multi-acquirer cascade routing delivers measurable authorization rate improvements. Industry benchmarks show cascading can improve authorization rates by 5-15%, translating into millions in recovered revenue for large platforms.

Paybis’ Smart Cascade Routing goes further. Paybis routes failed card transactions across multiple acquirers by BIN and region, with 3DS authentication decoupled from the retry sequence. This has produced an 11%+ increase in transaction success rates for partners compared to single-acquirer setups. A 5% authorization lift on a platform processing $10M monthly recovers $500,000 in GPV. An 11% lift recovers $1.1M, more than double the impact.

Dynamic Payout Routing by Region and Rail

Intelligent routing applies multiple criteria simultaneously, not just “try the next provider.” Modern orchestration engines evaluate BIN, currency, amount, and historical provider performance before selecting a route, with the entire decision adding minimal latency to checkout.

BIN routing directs card transactions to the acquiring bank most likely to deliver the best authorization performance for that specific card and region. Some payment providers report acquiring cost reductions of around 0.6% through BIN-based routing optimization, which can translate into significant savings at high transaction volumes.

Minimizing Declines with Intelligent Routing

The mechanics of routing directly determine how many transactions you recover. The difference between a naive retry loop and a well-designed cascade is the difference between annoying users and silently recovering GPV.

Failover Activation Thresholds

You cannot achieve 100% transaction uptime from a single PSP. It is a mathematical impossibility, which is why defining realistic, measurable thresholds matters more than aspirational SLA language.

Paybis operates at approximately 99.4% platform uptime (as reported by Paybis internal infrastructure monitoring), meaning the system is live and accepting requests, which provides a verifiable starting point for SLA discussions. Platform uptime, however, is a distinct metric from payment authorization rate: the former measures infrastructure availability, the latter measures whether transactions are being approved once the system receives them. A system can be fully operational while approval rates on a specific payment method drop due to acquirer-level factors outside the platform’s control. Monitoring both metrics separately and configuring failover thresholds for each is how payment operations teams catch degradation before it becomes visible to end users.

Configure Resilient Payout Retries

The cascade sequence follows a defined path when a transaction fails. Here is how it works in a production setup:

- Transaction initiated: Payment request arrives with amount, currency, card BIN, and customer location.

- Primary acquirer selected: The orchestration layer scores available PSPs on cost and historical approval rate for that BIN and region.

- Authorization attempt: Transaction routes to the highest-scoring acquirer.

- Decline detected: The system reads the decline error code to determine whether the failure is technical (timeout, connectivity) or behavioral (risk flag, card limit).

- Secondary acquirer routing: If a transaction declines through one channel, the orchestration layer can reroute it to another processor based on the type of decline and historical routing performance.

- 3DS data preserved: Authentication credentials pass to the next acquirer without requiring the user to re-authenticate.

- Final status returned: The cascade continues until an acquirer approves or the sequence exhausts available providers.

Multi-Acquirer Circuit Breaker Logic

Retry logic without limits creates its own problems. Each retry attempt costs gateway fees, and looping a transaction through every available acquirer without circuit breaker logic burns processing budget while degrading the user experience.

Circuit breaker logic defines the maximum number of retry attempts per transaction, the minimum time interval between attempts, and the threshold at which a provider gets temporarily removed from the routing pool due to elevated decline rates. Well-configured routing ensures every transaction takes the path most likely to succeed, based on card type, region, and historical provider performance, without spinning indefinitely on a provider that is actively underperforming.

Tracking Transaction State for Retries

3DS decoupling is the technical mechanism that makes silent failover possible. When an issuer returns a soft decline with an SCA-required response code (such as 20154), the merchant must retry with a new EMV 3DS challenge (EMV, short for Europay, Mastercard, and Visa, is the global standard governing chip-based card authentication), forcing the user to complete the verification flow again. SCA, or Strong Customer Authentication, is the regulatory requirement under PSD2 that mandates multi-factor authentication for electronic payments in the European Economic Area. That friction alone can eliminate the majority of retry conversions.

Paybis implements decoupled 3DS by separating the 3DS verification code required for transaction processing from the card payment itself. When the primary acquirer declines, the authentication token passes to the secondary acquirer without triggering a new challenge. The user sees nothing. The transaction either succeeds on the next pass or returns a clean decline after exhausting the cascade sequence.

This is the specific mechanism behind the 11%+ authorization lift. The improvement is not from adding more acquirers alone. It comes from eliminating the re-authentication friction that contributes to checkout abandonment when users encounter unexpected authentication steps mid-retry.

Proven Failover Designs for Payout Reliability

Routing logic is only half the solution. Idempotency, reconciliation, and audit infrastructure keep the accounting clean when transactions move across multiple providers.

Idempotency for Safe Payout Retries

For payout infrastructure, every transaction in a cascade sequence must carry a unique idempotency key that persists across retry attempts. When a connection error occurs mid-transaction, the key allows the system to safely repeat the request with confidence that no duplicate charge will result.

Idempotency documentation in financial services outlines a standard implementation pattern where the server stores a unique key and the result of each processing attempt. If a duplicate request arrives with the same key, the system skips reprocessing and returns the stored result, preventing double disbursements even when multiple acquirers are involved.

Reconciling Payout States Across Acquirers

When a transaction succeeds on a third acquirer after two declines, the net received and take rate calculations change. The backup acquirer may carry different fee structures, affecting the margin on that specific transaction.

Reconciliation systems should pull the acquirer-level outcome, not just the transaction-level result, to accurately attribute net received per payment method and per provider. When you use Paybis 0.49% base rate, cascade routing operates within that fee structure. You set your own end-user margins above the base rate.

Audit and Validation for Failover Systems

Every retry event should generate a structured log entry: transaction ID, idempotency key, acquirer attempted, error code returned, timestamp, and routing decision rationale. This data serves three purposes: compliance reporting, performance optimization, and dispute resolution.

For platforms operating across multiple jurisdictions, Anti-Money Laundering (AML) monitoring requires the ability to reconstruct the full transaction path. Paybis handles AML monitoring and reporting as part of the partner infrastructure, so the audit trail requirement is covered without building a separate compliance logging layer.

Testing failover logic before production deployment requires simulating specific failure modes: acquirer timeouts, BIN-level declines, 3DS authentication failures, and provider-level outages. The validation test suite should cover successful first-pass authorization, successful second-pass after primary decline, idempotency on duplicate submission, correct error code handling per acquirer, and accurate net received calculation across all routing paths.

White-Label Payout Failover Strategies

Building multi-acquirer orchestration in-house is a resource decision as much as a technical one. The math typically resolves the build-vs-buy question faster than the engineering debate does.

Build vs. Buy for Multi-Acquirer Setups

Typical vendor implementations reach production significantly faster than in-house builds. The comparable internal build, covering multi-processor infrastructure, compliance requirements, and PCI DSS scope management, can take 12-24 months or more. The cost differential is significant before a single transaction processes.

Here is how the two paths compare across the dimensions that matter to a payments product roadmap:

| Dimension | Build In-House | White-Label (Paybis) |

|---|---|---|

| Time to first live transaction | 12–24 months | Minutes (URL redirect), hours (full SDK) |

| PSP integrations available | Limited by engineering capacity | 150+ on demand |

| Compliance overhead | Full KYB/KYC build typically required | Inherited: MiCA CASP, PSD2 PI, FinCEN, FINTRAC, VASP Poland |

| 3DS decoupling | Custom engineering typically required | Pre-built |

| Ongoing PSP maintenance | Engineering team typically required | Managed by Paybis |

| Base transaction rate | Variable (staff + infrastructure) | Transparent base rate; partner sets end-user margin above it |

Streamlining Multi-Provider Payouts with Paybis Send

For platforms that need to execute mass crypto payouts without holding crypto on their balance sheet, Paybis Send provides the infrastructure layer.

Here is how it works: you pre-fund a virtual IBAN account in USD, EUR, or GBP. Payouts are executed in 90+ cryptocurrencies via API or partner dashboard to any wallet address, in near-real time, without clients holding crypto at any point. Crypto exposure windows are eliminated entirely.

For affiliate networks, payroll platforms, and PSPs executing bulk disbursements, this removes the reconciliation complexity of managing crypto balances across multiple wallets while still delivering crypto payouts to recipients who want them.

White-Label Payout Cost vs. Uptime

When you negotiate SLAs for payout infrastructure, address two separate dimensions: platform uptime (is the system operational?) and authorization rate performance (are transactions succeeding?). Both require defined penalty provisions in enterprise contracts, not just headline percentage claims.

A transparent pricing model starts at a 0.49% base rate. Net received is shown at the quote stage before any transaction is committed, so partners can compare cost per rail and transaction size against their existing setup before integrating.

Maximizing Multi-Provider Payout Uptime

Operational payout reliability requires ongoing monitoring discipline, not just a well-configured initial setup. Provider performance shifts over time as acquirer relationships change, BIN ranges get reassigned, and regional banking relationships evolve.

Authorization Rate Tracking by Provider

The authorization rate dashboard a payments team reviews weekly should segment by payment method, BIN range, region, and acquirer rather than relying on blended averages. A blended 75% approval rate can mask a 55% approval rate on a specific card range that accounts for 30% of transaction volume.

Paybis reports a 75% approval rate and 90%+ transaction success rate across its infrastructure. The distinction matters: approval rate reflects the acquirer-level authorization decision, while transaction success rate reflects the end-to-end outcome including retries. Monitoring both metrics at the payment method level provides the operational visibility needed to detect degradation before it becomes visible to end users.

“I appreciate Paybis for its ability to facilitate instant cryptocurrency purchases using my card, which significantly enhances the efficiency of my transactions. I enjoy the consistent and fast performance Paybis offers, ensuring reliable and swift operations every time I use it.” – Denis.I on G2

Minimizing Payout Downtime

High availability across 22 payment methods requires pre-tested failover sequences for each rail, not a generic “retry on decline” rule. SEPA (Single Euro Payments Area, the EU’s unified bank transfer network), SWIFT (Society for Worldwide Interbank Financial Telecommunication, the global messaging network used for cross-border bank transfers), ACH, and card payouts each have different failure modes, different error code taxonomies, and different optimal retry intervals.

Sophisticated routing systems incorporate automated fraud scoring, routing high-fraud-score transactions to gateways with robust 3DS or blocking them to prevent chargebacks that trigger acquirer relationship reviews. The same routing intelligence that improves authorization rates also prevents chargeback spikes that put provider relationships at risk. Corporate account payment rails have specific limits and routing behavior across institutional payment methods.

Identify Weak Payout Providers

A provider assessment framework should evaluate financial stability (are they regulated and solvent?), regulatory track record (any enforcement actions or sanctions?), geographic coverage (do they cover your top-10 markets by volume?), and authorization rate history (can they provide BIN-level performance data?).

Providers who cannot name their specific registration type and regulating authority during due diligence are not credible enterprise partners. Any provider claiming compliance coverage without producing registration numbers for specific jurisdictions should be treated as a single-point-of-failure risk regardless of their marketing materials.

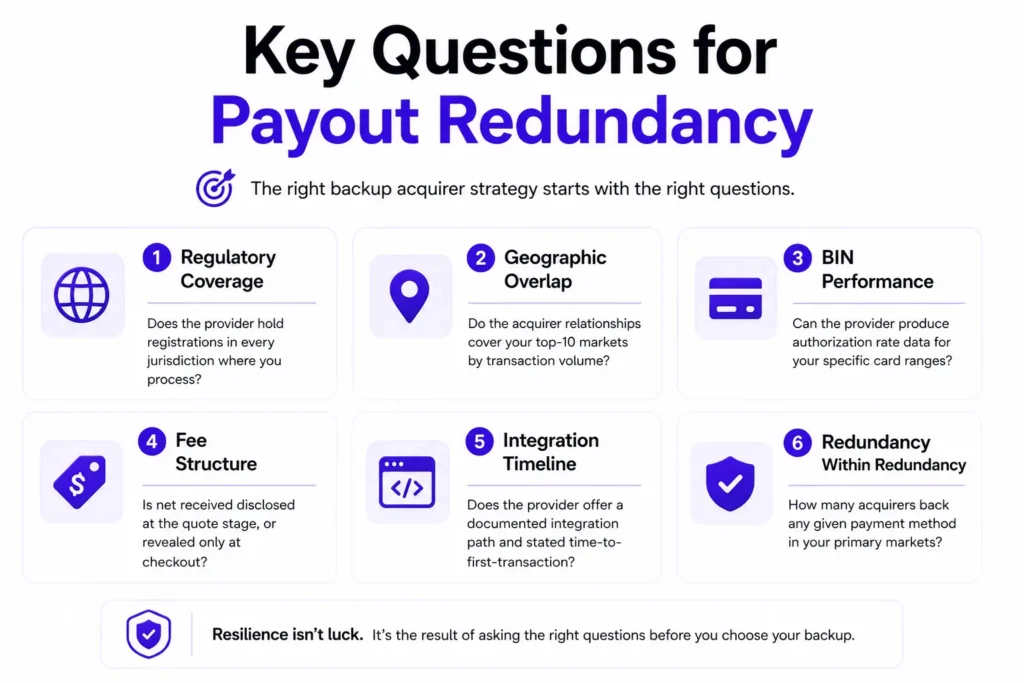

Key Questions for Payout Redundancy

Determining Your Backup Acquirer Needs

Before selecting backup acquirers, map your transaction volume by payment method, BIN range, and geography. A platform with 80% of volume on EU card payments needs different redundancy coverage than one with split exposure across ACH, SEPA, and local APMs.

The selection checklist covers these criteria:

- Regulatory coverage: Does the provider hold registrations in every jurisdiction where you process?

- Geographic overlap: Do the acquirer relationships cover your top-10 markets by transaction volume?

- BIN performance: Can the provider produce authorization rate data for your specific card ranges?

- Fee structure: Is net received disclosed at the quote stage, or revealed only at checkout?

- Integration timeline: Does the provider offer a documented integration path with a stated time-to-first-transaction via API, hosted widget, or native SDK?

- Redundancy within redundancy: How many acquirers back any given payment method in your primary markets?

Paybis operates across 180+ countries with 22 payment methods and 150+ PSP integrations on demand, covering the geographic and rail diversity that prevents any single regional acquirer failure from becoming a platform-wide payout outage.

Payout Failover Event Causes

The main triggers for a failover event fall into three categories. Technical failures include network timeouts, connectivity interruptions between the platform and the acquirer’s API, and processing infrastructure downtime at the provider level. Authorization failures include BIN-level risk flags, velocity limits on specific card ranges, and regional regulatory holds triggered by compliance monitoring. Relationship failures occur when a processor decides to block transactions due to concerns about your line of business or terminates service without advance notice, taking an entire payment rail offline.

Each trigger category requires a different response in the routing logic. Technical failures warrant an immediate retry with a different acquirer. Authorization failures typically benefit from routing to an acquirer selected using real-time signals, such as BIN, card type, and regional approval patterns, to maximise the likelihood of approval on the next attempt. Relationship failures require a pre-configured replacement provider to activate without engineering intervention.

Implementing Duplicate Payout Checks

Every retry sequence must carry an idempotency key that persists across all acquirer attempts. The key is generated at transaction initiation and stored server-side with the result of every processing attempt. If a duplicate request arrives with the same key, the server skips the operation and returns the previously stored result, preventing double disbursements regardless of how many acquirers the transaction touches.

For mass payouts executed through Paybis Send, the partner dashboard provides real-time monitoring of payout status and balance positions, giving the operations team visibility into in-flight transactions before reconciliation runs.

Choosing Your Payout Failover Strategy

The build-vs-buy decision resolves to a timeline and resource question. Building multi-acquirer orchestration in-house can take 12-24 months or more, compared to days or weeks with white-label infrastructure, and requires sustained engineering resources to maintain provider integrations as the payments landscape evolves. The opportunity cost is the work that does not get done during that period.

White-label infrastructure with Paybis compresses the same capability to minutes (URL redirect) or hours (full SDK), with 150+ pre-built PSP integrations, decoupled 3DS, and inherited compliance coverage across the US, Canada, UK, and EU. You set your own end-user margins above the 0.49% base rate on every transaction processed through the cascade.

Ready to evaluate Smart Cascade Routing against your specific payment method mix? Contact Paybis to review authorization rate performance and integration options, or review Paybis Send documentation to map mass payout infrastructure to your disbursement architecture.

Key Terminology

- Authorization rate: The percentage of payment attempts that a card issuer or acquirer approves, measured at the BIN level, by region, and by payment method for accurate performance monitoring.

- Authorization hold:A temporary hold placed on funds during a card transaction to verify availability before final settlement, ensuring the merchant can later capture the authorized amount.

- ACH (Automated Clearing House): An electronic network for financial transactions in the United States, commonly used for direct deposits, bill payments, and money transfers between banks.

- Counterparty risk: The risk that one party in a financial transaction (such as an acquirer, issuer, or PSP) fails to fulfill its obligations, leading to transaction failure or financial loss.

- APM (Alternative Payment Method): Payment methods beyond traditional credit and debit cards, including digital wallets, bank transfers, and local payment systems like PIX.

- 3DS decoupling: A technical implementation that separates the 3DS authentication token from the card payment, allowing the token to pass to a backup acquirer during a retry without triggering a new user authentication challenge.

- BIN routing: Automatic routing of card transactions to a specific acquiring bank based on the card’s Bank Identification Number (first six digits), used to optimize approval rates and reduce processing costs for specific card ranges.

- Spread: The difference between the base processing rate a payment provider charges and the end-user rate displayed at checkout. Providers who do not disclose spread until checkout make it impossible to accurately forecast net received per transaction.

- Finality:The point at which a blockchain transaction is considered irreversible and permanently recorded, ensuring that funds cannot be reversed or altered after confirmation.

FAQ

What Is Payout Redundancy in Payment Infrastructure?

Payout redundancy means configuring multiple acquirers and payment providers so that when one fails, another automatically processes the transaction without user interruption. A robust setup typically includes 2-5 acquirers in a cascade routing configuration to eliminate single points of failure.

How Does Cascade Routing Improve Authorization Rates?

Cascade routing retries failed transactions through alternative acquirers based on error code, BIN range, region, and historical approval rate. Paybis Smart Cascade Routing with 3DS decoupling delivers 11%+ improvement in authorization rates for partners, exceeding standard single-acquirer performance.

What Is 3DS Decoupling and Why Does It Matter for Payout Retries?

3DS decoupling separates the authentication token from the card payment so that when a transaction fails and routes to a backup acquirer, the user does not need to complete a new 3DS challenge. Without decoupling, each retry triggers a re-authentication step that most users abandon, eliminating the conversion benefit of the retry logic entirely.

How Many Acquirers Should a Payout System Have?

Industry research suggests a sweet spot of two to five acquirers in a cascade routing setup, providing robust redundancy across card ranges, regions, and payment methods. The specific number depends on your volume distribution by geography and payment method.

What Is an Idempotency Key and How Does It Prevent Duplicate Payouts?

An idempotency key is a unique identifier assigned to each transaction at initiation and stored server-side. If the same transaction retries across multiple acquirers, the idempotency key prevents the system from processing the payout twice.

How Does Paybis Send Enable Mass Crypto Payouts Without Holding Crypto?

Partners pre-fund a virtual IBAN account in USD, EUR, or GBP, then execute payouts in 90+ cryptocurrencies via API or dashboard. Fiat (government-issued currency such as USD, EUR, or GBP) balances are converted to crypto at the point of disbursement, so partners carry no crypto inventory risk while recipients receive crypto directly.

What Metrics Should a Head of Payments Track Weekly for Payout Reliability?

The core weekly monitoring set includes authorization rate by BIN range, authorization rate by acquirer, approval rate by payment method, decline rate by error code category, and transaction success rate (which includes retry outcomes). Blended averages mask the provider-level degradation that causes most payout reliability issues.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info