Are Crypto ETFs Safe? A Complete Guide To Understand Risks and Security

- Crypto ETFs protect against exchange collapse and lost passwords – Your Bitcoin is held by regulated custodians in cold storage, separated from the ETF provider’s assets.

- You’re fully exposed to Bitcoin’s price volatility – When Bitcoin drops 20%, your ETF drops 20%. Professional custody doesn’t cushion price movements.

- Trading limited to market hours – Bitcoin trades 24/7, but ETFs only trade 9:30am-4pm ET on weekdays. You can’t react to weekend crashes.

- Management fees compound over time – Most charge 0.20-0.25% annually, which adds up to $500+ over 20 years on a $10,000 position.

- SIPC insurance covers brokerage failure, not market losses – Protected if your brokerage goes bankrupt, not if Bitcoin’s price crashes.

$115 billion sits in U.S. crypto ETFs as of early 2026. That’s serious institutional money betting on the safety of these products. But “safe” is a tricky word when we’re talking about an asset class that can drop 20% in a weekend.

The answer is complicated, because “safe” means different things depending on what you’re worried about. Safe from hacks? From the exchange collapse? Or from Bitcoin dropping 40% in a month? These are completely different risks, and crypto ETFs protect you from some but not others.

Let’s break down what actually keeps your investment secure and where the real risks still live.

Table of contents

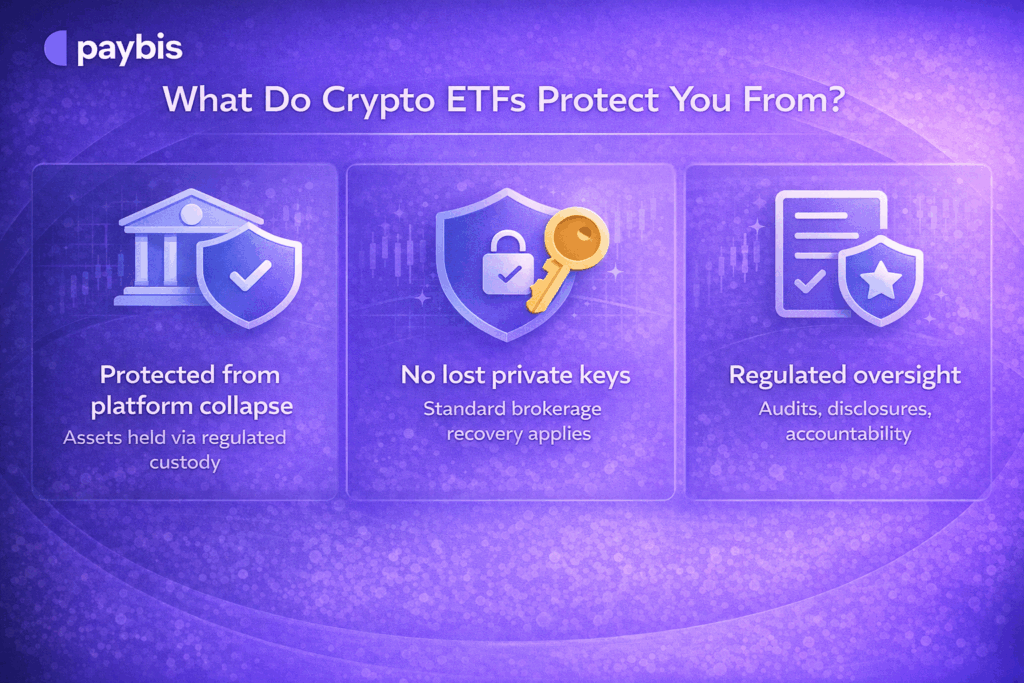

What Do Crypto ETFs Protect You From?

Let’s start with what crypto ETFs solve, because this is where they genuinely shine compared to other options.

Short answer: No. The Bitcoin is held separately by a custodian (usually Coinbase Custody) in a legal structure isolated from the ETF issuer’s assets. If BlackRock fails, your shares still represent a claim on that Bitcoin.

You can’t lose your investment to exchange failure. When you buy IBIT or FBTC shares, you’re buying a regulated security trading on Nasdaq. The actual Bitcoin sits with a custodian like Coinbase Custody, and it’s held in a separate legal structure from BlackRock’s own assets. If BlackRock somehow collapsed tomorrow, your shares represent a legal claim on that Bitcoin. It doesn’t vanish with the company.

This matters because we’ve watched major platforms implode. FTX took $8 billion in customer funds down with it in November 2022. Celsius, Voyager, and BlockFi were all gone within months of each other. Customers are still fighting in bankruptcy court years later, trying to recover any remaining assets. That specific failure mode can’t happen with ETFs because of how the custody structure works legally.

You can’t lose your investment by forgetting a password. This sounds trivial until you realize roughly 20% of all Bitcoin ever created is estimated to be lost forever because someone lost their private keys. With an ETF, you’re using your normal brokerage account.

Forgot your password? Your brokerage has recovery procedures. Lost your phone with two-factor authentication? You can prove your identity and regain access. The Bitcoin itself stays locked in Coinbase’s vaults regardless of what happens to your login credentials.

Regulatory oversight creates actual accountability. The SEC monitors crypto ETFs with mandatory audits and ongoing disclosure requirements. ETF issuers file regular reports. Custodians face regulatory standards for security and insurance. When something goes wrong, there are rules about what happens next and who’s responsible. That framework doesn’t prevent every problem, but it creates consequences for failure that don’t exist in less regulated parts of crypto.

These protections are real and meaningful. They’re why crypto ETFs appeal to people who want Bitcoin exposure without handling the technical and security burden alone.

How Bitcoin ETF Custody Actually Works

The security comes down to custody, and the custody setup is actually pretty interesting once you understand how it works.

- Cold wallets physically disconnected from the internet

- Multi-signature protocols requiring multiple approvals

- Geographically distributed vaults with institutional security

- Hardware security modules protecting private keys

- Insurance covering theft or loss (with limitations)

Most U.S. Bitcoin ETFs use Coinbase Custody to store the actual Bitcoin. They keep it in cold wallets, which are hardware devices physically disconnected from the internet and locked in geographically distributed vaults. They provide the kind of security you’d expect for storing billions of dollars. We’re not talking about USB drives in someone’s desk drawer. This is institutional-grade storage built specifically for holding massive amounts of cryptocurrency without ever touching the internet.

The authorization process adds another layer. Multi-signature protocols mean multiple parties have to approve any Bitcoin movement. One person can’t authorize a transfer even if they somehow compromised a single key. Hardware security modules encrypt and protect the private keys themselves with tamper-resistant technology. There’s insurance covering theft or loss, too. However, the coverage is often less comprehensive than it sounds on paper.

What does all this actually protect you from? Even if Coinbase’s offices got ransacked, even if their website suffered a major hack, even if an employee decided to go rogue, the Bitcoin stays locked in those cold wallets. The custody structure deliberately separates the Bitcoin from every operational failure point you could realistically imagine.

But here’s what it doesn’t protect against: Bitcoin’s price crashing, regulatory crackdowns, or broader market collapses. The Bitcoin itself is secure. Its value? That still swings with market forces completely outside anyone’s control.

The Risks That Crypto ETFs Don’t Eliminate

Now for the less comfortable part. Crypto ETFs solve specific custody and operational risks, but plenty of risk remains.

- Bitcoin’s price volatility (if Bitcoin drops 50%, your ETF drops 50%)

- Trading hour limitations (can’t sell on weekends when Bitcoin moves)

- Management fees compounding over decades

- Regulatory changes affecting crypto

- Operational failures at custodians (low risk, but not zero)

Bitcoin’s volatility hits ETF holders just as hard as direct holders. When Bitcoin dropped 20% in late 2025, every Bitcoin ETF dropped roughly 20% with it. The professional management and institutional custody don’t cushion price movements at all. If Bitcoin crashes 50% next month, your ETF shares crash 50%. You’re making the exact same bet on Bitcoin’s price performance, just wrapped in a different legal structure.

The trading hour mismatch creates problems during volatile periods. Bitcoin trades every second of every day. Your ETF shares trade from 9:30 am to 4 pm ET on weekdays only. Major Bitcoin moves happen on weekends regularly. If Bitcoin dumps 25% on Saturday night, ETF holders can’t do anything until Monday morning. By then, the price might have bounced back or crashed further. Either way, you were locked in watching it happen. That illiquidity during crucial moments is a real disadvantage.

Management fees compound over time and eat returns. Most Bitcoin ETFs charge 0.20-0.25% annually. That’s $25 per year on a $10,000 position, which sounds minor. But over 20 years, you’re paying $500+ in fees that direct holders don’t pay. Those fees come out of your returns regardless of whether Bitcoin goes up or down. The convenience costs money, and over long time horizons, that money adds up.

Regulatory risk still exists and could hurt values. The SEC could change rules around crypto ETFs. Congress could pass restrictive crypto legislation. International regulatory crackdowns could affect Bitcoin’s global price even if U.S. ETFs stay legal. The regulatory environment for crypto is far from settled, and unfavorable changes could impact your investment significantly, even though the Bitcoin itself remains safely stored.

Counterparty and operational risks haven’t disappeared completely. Yes, the custody model is secure. But it’s not physically impossible for things to go wrong. Operational failures, gaps in insurance coverage, and legal custody disputes are much lower than holding crypto on sketchy platforms. However, they’re not zero. You’re still trusting multiple institutions to do their jobs correctly.

What SIPC Insurance Actually Covers (And Doesn’t)

People hear “SIPC insurance” and assume they’re protected from losses. That’s only partially accurate and needs clarification.

SIPC covers up to $500,000 if your brokerage fails and your shares disappear. It does NOT cover Bitcoin price drops; you still own the shares, they’re just worth less.

SIPC covers up to $500,000 per customer if your brokerage fails and your securities disappear. Notice what triggers coverage: brokerage failure, not investment losses. If your brokerage goes bankrupt and your ETF shares vanish, SIPC protects you. If Bitcoin crashes and your ETF shares lose 60% of their value, SIPC does absolutely nothing because you still own the shares. They’re just worth less.

The custodian insurance works separately. Coinbase Custody maintains insurance for the Bitcoin it holds, covering theft or physical loss of the Bitcoin itself. But that insurance doesn’t cover Bitcoin’s market price declining. If hackers somehow broke through all the security layers and stole Bitcoin from cold storage, insurance pays out. If Bitcoin’s price drops from $100,000 to $40,000, insurance doesn’t apply at all because the Bitcoin is still there.

So, “insured” and “protected” sound comprehensive but only apply to specific failure scenarios, not to normal market movements or volatility.

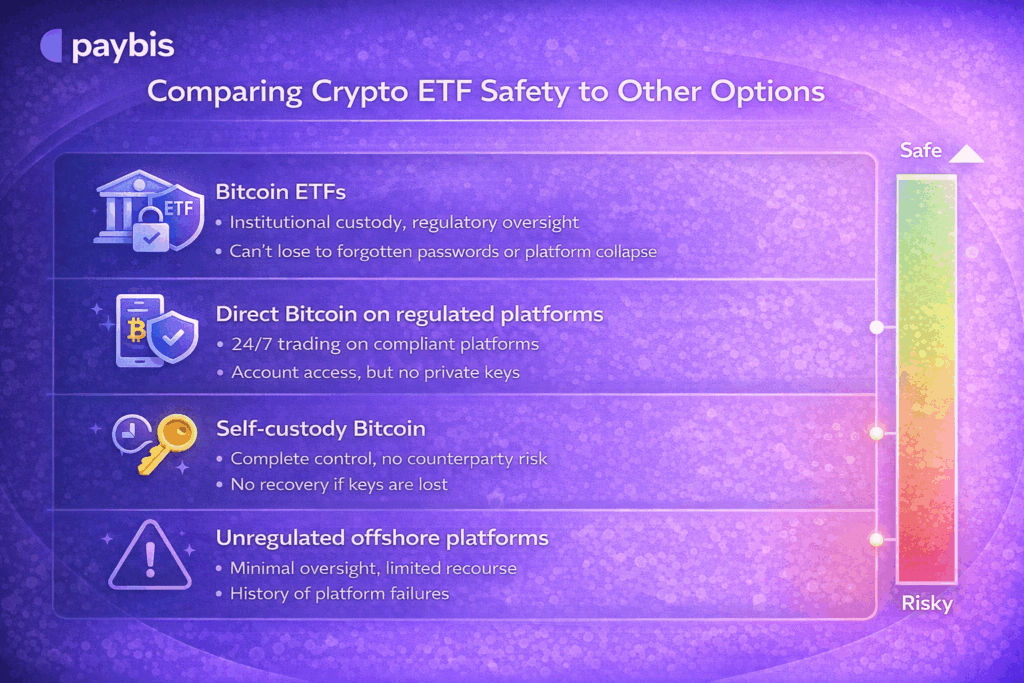

Comparing Crypto ETF Safety to Other Options

Put crypto ETFs in context with alternatives to see where they actually sit on the risk spectrum.

- Bitcoin ETFs: Institutional custody, regulatory oversight, can’t lose to forgotten passwords or platform collapse. Still fully exposed to Bitcoin’s price volatility. Trading is limited to market hours. Management fees ongoing.

- Direct Bitcoin on regulated platforms: You maintain more control over when to buy and sell (24/7 trading). Regulated platforms like Paybis operate under financial authority oversight with compliance requirements and customer protections. You’re responsible for securing your account, but you’re not managing private keys if you leave Bitcoin on the platform. No ongoing management fees after purchase.

- Self-custody Bitcoin: You control private keys completely and eliminate every form of counterparty risk. Maximum control, maximum responsibility. Lost keys mean lost Bitcoin permanently with no recovery. This option makes sense for people comfortable with technical security practices and willing to accept that burden.

- Unregulated offshore platforms: Minimal oversight, limited recourse if something goes wrong, and a huge history of platform failures. It’s a higher risk category that experienced crypto users might navigate carefully, but newcomers should definitely avoid.

The right choice depends entirely on what risks concern you most and what tradeoffs you’re willing to accept. Crypto ETFs optimize for convenience and institutional protection. Direct ownership optimizes for control and avoiding ongoing fees. Neither is universally “safer”; they just protect against different failure modes.

Bottom Line

Crypto ETFs are safe from platform collapse or custody failures. You also don’t need to worry about lost password scenarios. But ETFs are not safe from Bitcoin’s price volatility, regulatory changes, or the ongoing cost of management fees.

If you’re investing through a retirement account or want Bitcoin exposure without managing security yourself, ETFs solve real problems. If you want 24/7 trading control and don’t want fees eating your returns over decades, direct ownership makes more sense.

“Safe” depends entirely on which risks you’re trying to avoid. Both approaches work. Neither eliminates Bitcoin’s volatility.

FAQ

Can I lose my crypto ETF investment if Bitcoin gets hacked?

No. Bitcoin ETFs store Bitcoin in institutional cold wallets physically disconnected from the internet. Even if someone hacked Coinbase’s website or compromised online systems, the Bitcoin stays secure in those offline vaults. What you can lose money from is Bitcoin’s price dropping. If Bitcoin crashes 40%, your ETF shares drop 40% too. The custody protects against theft and hacks, not market volatility.

Is my crypto ETF covered by SIPC insurance?

Yes, but only for specific scenarios. SIPC covers up to $500,000 if your brokerage fails and your ETF shares disappear. It does NOT protect you from Bitcoin’s price declining. If Bitcoin drops 50% and your shares lose value, SIPC doesn’t apply because you still own the shares. They’re just worth less. The insurance protects against brokerage failure, not investment losses.

Are crypto ETFs safer than buying Bitcoin on an exchange?

They protect against different risks. Crypto ETFs eliminate the risk of platform collapse (like FTX) and lost password scenarios through institutional custody and brokerage recovery systems. Direct Bitcoin on regulated exchanges like Paybis gives you 24/7 trading access and no ongoing fees, but you’re responsible for account security. Neither protects you from Bitcoin’s price volatility. “Safer” depends on which specific risks concern you most.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info