Bitcoin ETF vs Buying Bitcoin Directly: Key Differences Explained

Key Takeaways

- ETFs give you convenience and safety. Professional custody, simple tax reporting, perfect for retirement accounts. You pay 0.25% annually forever.

- Direct ownership gives you control and lower long-term costs. You manage security yourself, pay fees once upfront, can use Bitcoin beyond just holding it.

- Age and technical comfort determine your choice. Traditional investors near retirement lean toward ETFs. Young crypto-savvy investors lean toward direct ownership.

- Many serious investors use both. ETFs in retirement accounts for tax benefits, direct Bitcoin for flexibility and control.

Your financial advisor says buy IBIT, but your crypto friend says buy actual Bitcoin. Both claim they’re protecting you.

$115 billion sits in Bitcoin ETFs as of early 2026. BlackRock’s IBIT alone holds $75 billion. That’s institutional money that chose the ETF route. Meanwhile, 85 million people worldwide own Bitcoin directly, choosing full control.

So which approach actually makes sense for you? Let’s break down what you actually get with each option.

Table of contents

- Bitcoin vs Bitcoin ETF: What Are You Really Buying?

- Bitcoin ETF Fees vs Direct Bitcoin Costs: The Real Price Difference

- Bitcoin ETF Security vs Self-Custody: Who Holds Your Keys?

- Bitcoin Inheritance and Estate Planning: ETFs vs Direct Ownership

- Tax Season: 1099 Forms vs. Transaction Tracking Hell

- Four Investors, Four Different Answers

- The Hybrid Strategy: 60/40 Split Between Bitcoin ETFs and Direct Bitcoin

- Bottom Line

Bitcoin vs Bitcoin ETF: What Are You Really Buying?

The difference starts with what you actually own. When you buy shares of IBIT or FBTC, you own pieces of a fund that holds Bitcoin. You can think of it like owning shares in a gold mining company instead of gold bars sitting in your safe.

The fund manages everything. You trade shares on Nasdaq during market hours, and your brokerage treats it like any stock position. Simple, familiar, institutional.

Direct Bitcoin ownership flips that completely. You’re holding the actual asset in your wallet or exchange account. You can move it anywhere, send it to anyone, use it in DeFi protocols, or store it on a hardware wallet in your drawer. The Bitcoin responds to you, not a fund manager.

This creates a practical split that shows up immediately. IBIT trades 9:30 am to 4 pm EST on weekdays. Bitcoin trades every second of every day. When major news drops at 11 pm Saturday and Bitcoin spikes 8%, direct holders can act right then. ETF holders watch and wait until Monday morning.

Trust models are quite different, too. Bitcoin ETFs collectively hold 1.14 million BTC, mostly stored by Coinbase Custody in cold wallets with multi-sig security. You’re trusting BlackRock to manage properly, Coinbase to secure the Bitcoin, your brokerage to process trades, and the SEC to maintain favorable rules. Multiple institutions, multiple points of trust. Many investors prefer that over managing the security themselves.

Direct ownership puts you in charge. You trust yourself or your chosen exchange. No intermediaries between you and your Bitcoin. That appeals to people who want real ownership, but it means accepting responsibility for security, backups, and not losing your private keys.

We have prepared a comparison tool that will help you decide.

Which Bitcoin Option Fits You?

Answer 4 quick questions to explore your options

⚠️ Disclaimer: This tool provides educational information only, not financial advice. Crypto investing is high-risk. Don’t invest more than you can afford to lose. Crypto-assets aren’t covered by government protection schemes. Do your own research and consult a financial advisor before investing.

Bitcoin ETF Fees vs Direct Bitcoin Costs: The Real Price Difference

ETF fees are dead simple. Most competitive Bitcoin ETFs charge 0.20% to 0.25% annually on your entire position. BlackRock's IBIT charges 0.25%, and so does Fidelity's FBTC. That percentage hits your investment every single year you hold it.

Run the numbers on a $10,000 position:

- First year: $25 in fees

- Five years: $125 total

- Ten years: $250 total

Direct Bitcoin has a completely different cost structure. You pay trading fees when you buy, then again when you sell. Nothing in between. Paybis charges 0.99% to 4.5%, depending on payment method.

Same $10,000 through direct purchase:

- Paybis card payment: $350 upfront (3.5% fee)

- Network fees: $3 to move to the wallet

- Total entry cost: $353

- Ongoing fees: $0

Timeline decides which is cheaper. If you hold 15+ years, direct ownership wins. If you trade frequently or invest under $500, ETF fees cost less overall.

But there is a variable to consider: Bitcoin network fees. They spiked during congestion and hit $15-20 per transaction during busy periods in 2025. ETF holders never worry about this because they're trading shares, not moving Bitcoin on the blockchain.

Bitcoin ETF Security vs Self-Custody: Who Holds Your Keys?

ETF security runs through institutional custody. Ten of twelve U.S. Bitcoin ETFs use Coinbase as custodian. They store Bitcoin in cold wallets disconnected from the internet, use multi-signature protocols requiring multiple approvals, and maintain insurance covering theft or loss.

The practical upside is that you can't lose IBIT by forgetting a password. Your brokerage has account recovery. The Bitcoin stays locked with Coinbase regardless of what happens to your login.

Direct ownership puts security entirely on you. In 2025 alone:

- 158,000 wallet compromises

- 80,000 people affected

- $713 million lost

- Phishing and social engineering attacks getting more sophisticated

Hardware wallets offer solid security, but you must store the 12-24 word recovery phrase somewhere safe. If you lose it, your Bitcoin vanishes permanently. No customer service, no password reset. Researchers estimate 20% of all Bitcoin (3.7 million BTC) is lost forever due to lost keys.

Most people aren't equipped for Bitcoin security. Multi-signature wallets take technical knowledge, and storing backup phrases requires planning. So one mistake costs everything.

But some people still prefer full ownership and responsibility. They'd rather trust themselves than Coinbase, even if they are accepting the security burden. For them, that burden feels like freedom.

Bitcoin Inheritance and Estate Planning: ETFs vs Direct Ownership

Estate planning shows the biggest divide between approaches. About 90% of crypto holders have no proper inheritance plan.

- Holding Bitcoin directly: Your heirs need your private keys to access anything. Store keys in your will? They become public record during probate, exposing them to theft. Don't store them? The Bitcoin is gone forever.

- ETF shares transfer through normal estate mechanisms. Heirs inherit IBIT shares exactly like Apple stock. No cryptography knowledge needed, no private keys to find.

For generational wealth transfer, ETFs win clearly.

Tax Season: 1099 Forms vs. Transaction Tracking Hell

Both ETFs and direct Bitcoin face the same basic tax treatment. The IRS classifies both as property. You pay capital gains taxes on profits. Short-term gains (under 1 year) get taxed as ordinary income, whereas long-term gains (over 1 year) get preferential rates.

Where they differ is in the reporting complexity.

- ETF route: Your brokerage sends you a 1099 form showing your gains or losses. You need to hand that to your accountant. Simple transaction history, clear cost basis, and no ambiguity.

- Direct Bitcoin route: Every transaction creates a taxable event. Buying, selling, trading, and using Bitcoin to buy something are all taxable.

The tracking burden is real but manageable. If you're dollar-cost averaging by buying Bitcoin 12 times throughout the year, you've created 12 separate tax lots to track. If you sell some later, you'll need to figure out which specific Bitcoin you sold, since FIFO, LIFO, and specific identification methods each produce different tax outcomes.

Software like CoinLedger automates most of this tracking. It connects to exchanges, imports transactions, and generates tax reports. Yes, it's more work than getting a single 1099 from your brokerage, but it's not the nightmare some people make it out to be. Thousands of crypto holders handle this every year without issue.

You can hold IBIT or FBTC in your IRA or 401(k). A $50,000 Roth IRA investment growing to $200,000 over 15 years generates zero taxes ever. The same investment in direct Bitcoin held in a taxable account triggers capital gains taxes when you sell.

You can also donate direct Bitcoin to charity. If you donate appreciated Bitcoin, you deduct the fair market value while avoiding capital gains tax on the appreciation. Charities are starting to accept crypto donations specifically because of this tax benefit.

So if you want Bitcoin in your retirement account, an ETF is your option. For taxable accounts, ETFs simplify your life significantly at tax time.

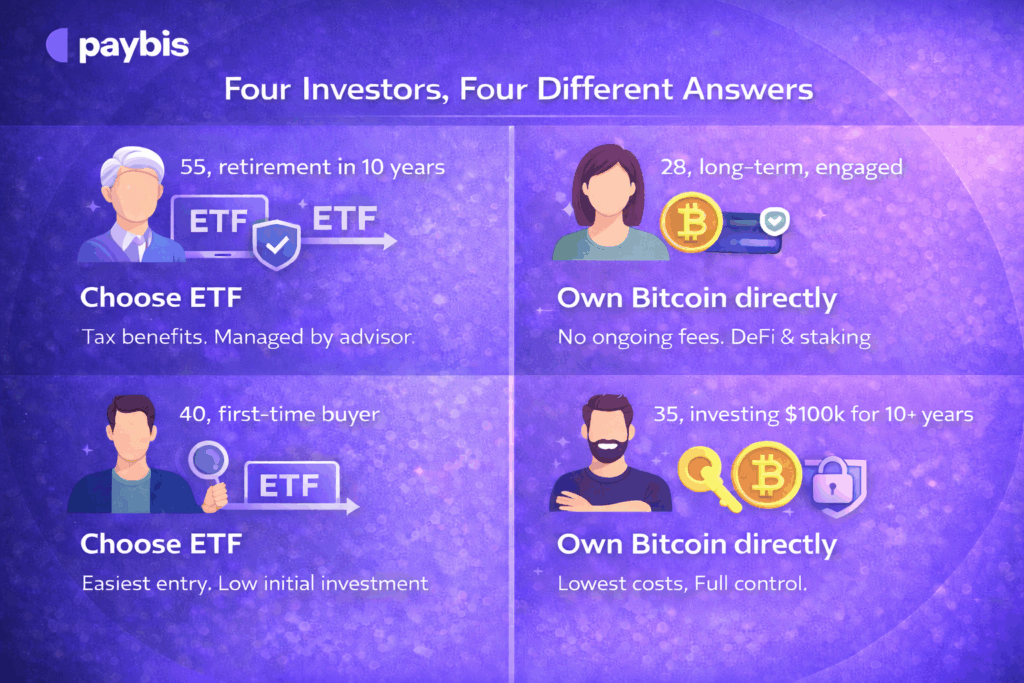

Four Investors, Four Different Answers

Let's look at real scenarios to make this concrete.

Scenario 1: You're 55, planning retirement in 10 years.

Your financial advisor manages your portfolio. You've heard about Bitcoin's potential, but don't want to learn about crypto wallets. Let's say you're investing $25,000 as 3% of your total portfolio.

Consider: Bitcoin ETF in your IRA.

You get tax-deferred growth, professional custody through Coinbase, and integration with your existing investment strategy. Your advisor can rebalance your portfolio, including Bitcoin exposure, without you touching anything. Zero technical learning curve. When you retire, you can sell shares through your familiar brokerage account.

The 0.25% annual fee costs $62.50 per year on a $25,000 investment. That's worth it for the convenience and security in this scenario.

Scenario 2: You're 28, already own some crypto, and want to add $500 monthly.

You understand private keys and feel comfortable with hardware wallets. You might want to use Bitcoin for DeFi eventually or stake it, and you also don't want fees eating your returns over 30+ years.

Consider: Buying Bitcoin directly.

Dollar-cost averaging $500/month for 30 years through an ETF costs you $1,500 in fees in just year one (assuming 0.25% on growing balance). Over 30 years, that compounds to serious money lost to fees. Direct purchases let you avoid ongoing fees entirely. You pay once per transaction, then hold without bleeding money annually.

Plus, you get actual Bitcoin you can use. Want to earn staking yields? ETFs can't do that. Want to participate in DeFi protocols? You need actual crypto. Planning to use Bitcoin for peer-to-peer transactions someday? Direct ownership is the only option.

Your technical knowledge makes the security burden manageable. You'll set up a hardware wallet properly, store backup phrases safely, and take responsibility for your own custody.

Scenario 3: You're 40, testing Bitcoin for the first time with $1,000.

You've read about it but aren't sure you'll hold long-term. So you want the easiest entry point. Security is your top concern because you don't understand crypto security yet.

Consider: Bitcoin ETF initially, maybe direct ownership later.

Open your existing brokerage account. Search for IBIT or FBTC. Buy shares like you'd buy any stock. Done in 5 minutes. You don't need a new account setup or identity verification on crypto exchanges. Also, no wallet decisions to make.

Your Bitcoin exposure is protected by the same SIPC insurance covering your other investments (up to $500,000, though crypto holdings may not fully qualify). More importantly, you can't lose it through user error. If you forget a password, you can recover your brokerage access. It matters when you're learning.

If you decide Bitcoin is for you after holding for 6 months, then consider buying directly. But starting with an ETF removes all technical barriers while you learn.

Scenario 4: You're investing $100,000 and plan to hold 10+ years.

You have time to learn proper security and you want maximum control and lowest costs over time. This is serious money you're committing to Bitcoin.

Consider: Buying Bitcoin with a hardware wallet.

A $100,000 investment in an ETF costs $250 annually in fees at 0.25%. Over 10 years, that's $2,500 minimum (more if Bitcoin appreciates). Over 20 years, $5,000+. Direct ownership means paying around $500 upfront in trading fees, then holding with zero ongoing costs.

At this investment level, the fee savings justify the effort of learning proper security. Buy two hardware wallets (one primary, one backup). Set up multi-signature if you're technically comfortable. Store recovery phrases in separate secure locations. Maybe use a professional custody service as one of the signers in a 2-of-3 multi-sig setup.

The control matters too. You own 100% of your Bitcoin and have no counterparty risk with Coinbase. Also, no trust in BlackRock. If you believe Bitcoin is valuable specifically because it eliminates intermediaries, this is the only approach that preserves that property.

The Hybrid Strategy: 60/40 Split Between Bitcoin ETFs and Direct Bitcoin

Some experienced investors split their Bitcoin holdings.

A common approach is to allocate 60% to retirement accounts via a Bitcoin ETF and 40% to direct purchases in personal accounts. This provides tax-deferred growth for the majority while maintaining some direct ownership for flexibility.

Here's how this might look with a $100,000 Bitcoin allocation:

$60,000 in a 401(k) holding IBIT shares. This portion grows tax-deferred until retirement.

$40,000 in direct Bitcoin purchases. This portion can be moved, used, or sold 24/7 without market hour restrictions.

The downside: you're managing both. You need to understand Bitcoin security for the direct portion while also monitoring your ETF holdings. That adds complexity.

Some people reverse the ratio: 70% direct, 30% ETF. Others go 80/20 in either direction. The split depends on your priorities.

Bottom Line

Bitcoin ETFs provide simplified access, but direct ownership gives control. Both work.

- Choose based on your technical comfort level. Can you secure a hardware wallet properly? Do you want to? ETFs remove that entire burden.

- Consider your time horizon. Holding for 20+ years makes direct ownership cheaper due to avoiding annual fees. Trading frequently makes ETFs more convenient since you don't pay network fees on every move.

- Think about what you'll do with your Bitcoin. Just holding for price appreciation? ETFs are perfect. Want to use Bitcoin as actual currency or in DeFi? You need direct ownership for that.

- Your tax situation matters. Bitcoin in retirement accounts strongly favors ETFs. In taxable accounts, both work, but ETFs simplify reporting significantly.

Want to buy Bitcoin directly? Paybis offers same-day verification, 20+ payment methods across 180+ countries, and transparent fees. FCA-regulated with straightforward pricing.

FAQ

Can I lose my Bitcoin ETF investment if I forget my brokerage password?

No. Your brokerage account has standard recovery procedures. You can prove your identity through documentation, security questions, or contacting customer service to regain access. The Bitcoin held by the ETF remains secure with the custodian (usually Coinbase) regardless of your login issues. With direct Bitcoin ownership, losing your private keys means permanent loss with no recovery option.

Which is actually cheaper over 10 years: Bitcoin ETF or buying directly?

It depends on your investment size and holding period. A $10,000 Bitcoin ETF position costs about $250 in fees over 10 years (at 0.25% annually). Buying $10,000 of Bitcoin directly through Paybis costs $99-$450 upfront, depending on payment method, then $0 in ongoing fees. For holdings over 10+ years, direct ownership typically costs less. For smaller amounts under $1,000 or frequent trading, ETFs might be cheaper overall.

Can I hold both a Bitcoin ETF and direct Bitcoin at the same time?

Absolutely. Many investors split their allocation, putting 60-70% in retirement accounts via Bitcoin ETFs for tax advantages, and 30-40% in direct Bitcoin for flexibility and control. This hybrid approach maximizes the benefits of both methods—tax-deferred growth in retirement accounts plus direct ownership for immediate access and potential DeFi participation.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info