The Complete Guide to Crypto ETFs: Everything You Need to Know in 2026

Updated January 9, 2026

Key Takeaways

- SEC approved 11 Bitcoin ETFs in January 2024 after 10 years of rejections. They pulled $10 billion in 3 days and hit $107 billion by year-end

- BlackRock’s IBIT dominates with $67.6 billion AUM, capturing 60% of daily inflows and growing faster than any ETF in history

- ETFs cost 0.20-0.25% annually and only trade during stock market hours, while direct crypto offers 24/7 trading, staking yields (3-4% for Ethereum), and zero management fees

- Institutions now control over 7% of all Bitcoin through ETFs and corporate treasuries

- 100+ new crypto ETFs will launch in 2026 with projected inflows doubling to $63+ billion

Crypto ETFs changed everything in January 2024. SEC approved 11 Bitcoin ETFs after a decade of rejections. These funds pulled $10 billion in their first 3 days, which was a record that took gold 3 years to reach.

Institutions poured money in immediately. BlackRock’s Bitcoin ETF alone pulled $53 billion in its first year. That’s faster growth than any ETF in history across all asset classes.

So what are Crypto ETFs? This guide covers everything: how crypto ETFs work, which ones exist now, what’s coming in 2026, and whether you should buy the ETF or the actual crypto.

Table of contents

- What Is Crypto ETF?

- Why Did It Take 10 Years to Approve Bitcoin ETFs?

- Which Crypto ETFs Can You Actually Buy Right Now?

- What Happened to Crypto ETFs in 2025?

- What Happens When Institutions Control 7% of Bitcoin?

- Should You Buy the ETF or the Actual Crypto?

- Which ETFs Are Winning (And Why IBIT Dominates)

- What Can Go Wrong With Crypto ETFs?

- How to Buy Your First Crypto ETF in 4 Steps

- How Crypto ETF Taxes Actually Work

- Bottom Line

What Is Crypto ETF?

Crypto ETF is an exchange-traded fund that tracks cryptocurrency prices. You buy shares on regular exchanges like Nasdaq or the NYSE, and those shares represent a stake in the fund’s cryptocurrency holdings.

The process is simple: when Bitcoin’s price moves, the ETF’s share price moves with it. You’re getting full crypto exposure without ever creating a Coinbase account or memorizing seed phrases. With ETFs, you also don’t need to worry about which wallet supports which blockchain.

There are two flavors worth knowing about. Spot ETFs hold actual cryptocurrency; real Bitcoin sitting in cold storage vaults managed by custodians like Coinbase. Futures ETFs hold contracts betting on future prices, which sounds similar but creates tracking issues we’ll get into later. For now, just know that spot ETFs are what most investors actually want.

Spot ETFs vs Futures ETFs: What Is the Difference?

The difference comes down to what the fund actually owns.

Spot ETFs hold actual cryptocurrency. BlackRock’s Bitcoin ETF, for instance, has actual Bitcoin sitting in cold storage vaults managed by Coinbase Custody. When you buy shares, you’re buying a slice of that physical (well, digital) stockpile.

Futures ETFs hold contracts predicting future prices. This creates a structural problem. Those contracts expire monthly and force the fund to “roll” them into new contracts. That rolling process bleeds money. It’s like paying a fee every month just to maintain your position, as these costs quietly eat into your returns over time.

This is why futures ETFs have existed since October 2021 but never gained serious traction. Spot ETFs only got approved in January 2024, and the moment they launched, the choice became obvious. Spot ETFs track Bitcoin’s price accurately because they own the thing they’re tracking. Futures ETFs can drift from actual Bitcoin prices depending on market conditions, and those rolling costs piling up.

Most investors now treat futures ETFs as relics: useful only for specific trading strategies that need derivatives exposure. If you just want to own Bitcoin through an ETF, spot is the clear answer.

Want to buy crypto directly? Paybis offers same-day verification, 20+ payment methods, and access to 90+ cryptocurrencies. FCA-regulated with transparent fees.

Why Did It Take 10 Years to Approve Bitcoin ETFs?

Asset managers started filing Bitcoin ETF applications back in 2013, and the SEC rejected every single one for the next decade. Gary Gensler, then SEC Chair, had concerns mainly about market manipulation and custody security. Fair enough, except the SEC had already approved Bitcoin futures ETFs in October 2021, which made their spot ETF rejections look inconsistent.

Grayscale saw the contradiction and sued in 2022 after its own application got denied. A federal appeals court sided with them. They ruled the SEC had “acted arbitrarily and capriciously” by greenlighting futures products while blocking spot products. The court essentially said: you can’t approve one Bitcoin derivative and reject another without explaining why.

So the SEC’s hand was forced. On January 10, 2024, they approved 11 spot Bitcoin ETFs simultaneously from BlackRock, Fidelity, Grayscale, ARK Invest, VanEck, Bitwise, Invesco, WisdomTree, Valkyrie, Franklin Templeton, and Hashdex.

Trading started January 11, 2024. First-day volume hit $4.6 billion. By the end of year one, these ETFs had accumulated $107 billion in assets under management.

Gensler made sure to clarify the approval in his statement: “The SEC did not approve or endorse Bitcoin. Investors should remain cautious about the risks associated with Bitcoin and products whose value is tied to crypto.” Translation: we’re approving this because the court made us, not because we think it’s a good idea. Legal compliance, not enthusiasm.

Most “top crypto” ETFs end up looking simpler on the surface than they actually are. The overfunded effect you’re seeing usually comes from premiums, liquidity gaps, or how the fund custodies the underlying assets. Crypto ETFs don’t behave like S&P index funds because the underlying market is fragmented and custody risk still exists. So the ETF price drifting above actual NAV isn’t unusual.

Yogurtclosettall on Reddit

Which Crypto ETFs Can You Actually Buy Right Now?

The crypto ETF market has exploded to 39 funds trading in the US as of January 2026. Here’s what’s actually available and which ones matter:

Bitcoin ETFs (11 funds)

These were the original wave that launched in January 2024, except for Grayscale’s GBTC, which converted from an existing trust structure. The market has already picked its winners. BlackRock’s IBIT dominates with $67.6 billion in assets, followed by Fidelity’s FBTC at $13 billion. Grayscale’s GBTC still holds significant Bitcoin from its trust days, but it’s been bleeding assets since conversion because of its 1.50% fee. It’s around six times higher than the 0.20-0.25% most competitors charge.

Collectively, Bitcoin ETFs now hold 710,777 BTC, which represents about 3.6% of Bitcoin’s total supply. That’s a meaningful chunk of a finite asset, and it’s growing.

Ethereum ETFs (9 funds)

These launched in July 2024 once the SEC finally approved spot Ethereum products. The usual suspects showed up: BlackRock’s ETHA, Fidelity’s FETH, and Grayscale’s ETHE lead the pack. What’s surprising is how fast they’ve grown; Ethereum ETFs pulled $9.6 billion in 2025, their first full trading year. That’s four times what Bitcoin ETFs managed in 2024, despite launching mid-year.

However, there’s a significant catch: Ethereum ETFs can’t offer staking rewards. The SEC required issuers to exclude staking functionality to get approval. This means investors miss out on the 3-4% annual yield that direct ETH holders earn just for holding. If you’re buying Ethereum purely for price appreciation, the ETF works fine. If you care about that yield, you’ll need to own ETH directly.

Solana ETFs (7+ funds)

Launched October 2025 following the SEC’s September approval of generic listing standards. This new fast-track process cut approval times from months to weeks.

Solana ETFs pulled $765 million in their first 2 months. It’s smaller than Bitcoin or Ethereum, but solid considering Solana’s smaller market cap.

XRP ETFs (6+ funds)

Launched November 13, 2025. The newest major crypto ETF category.

XRP ETFs have pulled in $1.2 billion since their launch, which is more than Solana has in less time. The timing aligned with regulatory clarity around Ripple’s legal status and growing institutional adoption of XRP for cross-border payments.

Other Altcoin ETFs

Litecoin, Dogecoin, Cardano, Chainlink, HBAR, and others have ETFs in various approval stages. As of December 2025, 125+ ETF filings awaited SEC approval.

Galaxy Research predicts 100+ new crypto ETFs will launch in 2026 with $50 billion+ in combined inflows.

What Happened to Crypto ETFs in 2025?

2025 ended rough for Crypto. Bitcoin ETFs had their worst two-month stretch ever in November-December 2025. They bled $4.57 billion in net outflows as Bitcoin’s price dropped 20% from its October peak of $126,000 down to around $95,000 by year-end. Ethereum ETFs lost another $2 billion during the same selloff.

But January 2, 2026 saw $645.8 million flow back into crypto ETFs. That didn’t happen randomly. Institutional investors had been tax-loss harvesting in Q4, deliberately selling at year-end to offset gains on their tax returns, then buying back once the new tax year rolled around. It’s a predictable pattern once you know to look for it.

Total 2025 inflows: $31.77 billion across all crypto ETFs

- Bitcoin: $21.4 billion (down from $35.2 billion in 2024)

- Ethereum: $9.6 billion

- Solana: $765 million

- XRP: $1.2 billion (2 months only)

However, crypto ETFs didn’t meet the hype expectations that built up during 2024’s bull run. Bitcoin hit new all-time highs above $126,000, yet many altcoins never reached their previous cycle peaks. The traditional four-year boom-bust cycle that crypto traders have relied on for a decade seems to be breaking down as institutional money changes how these markets move.

What Happens When Institutions Control 7% of Bitcoin?

The floodgates opened in 2025 when Morgan Stanley, Wells Fargo, and Merrill Lynch gave their wealth management clients access to crypto ETFs. These firms collectively manage $44 trillion, and financial advisors who previously couldn’t touch crypto due to compliance restrictions suddenly had a green light.

Now 56% of advisors are willing to allocate client money to crypto through ETFs, according to Bitwise research. Bernstein analysts project institutional ownership will hit 40% of all Bitcoin ETF holdings in 2026, nearly double the 2024 levels.

Supply Dynamics Change

Bitcoin ETFs have accumulated 710,777 BTC since January 2024, which is more than twice the amount Bitcoin miners produced during that same period. The math gets tight: miners create roughly 450 BTC daily, while ETF purchases regularly exceed 1,000 BTC per day. This creates a structural supply squeeze where less Bitcoin becomes available for retail buyers, which naturally pushes prices higher when demand spikes.

If you add in corporate treasuries like Strategy (formerly MicroStrategy) holding 671,268 BTC (about 3.2% of total supply), you realize institutions now control over 7% of all Bitcoin that will ever exist. For an asset capped at 21 million coins, that’s meaningful concentration.

Bitcoin Becomes More Like a Stock

But institutional ownership comes with a tradeoff: Bitcoin is starting to behave like just another risk asset. Its correlation with the NASDAQ 100 jumped to 0.52 in 2025, up from 0.23 in 2024. That’s a massive shift in just one year.

What this means in practice: when tech stocks sell off, Bitcoin follows. When the Fed cuts rates, Bitcoin rallies alongside other risk assets. The “digital gold” narrative that positioned Bitcoin as a portfolio hedge against traditional markets weakened considerably in 2025. Because Bitcoin moved in lockstep with tech stocks during tariff shocks and rate decisions. It’s becoming less of an uncorrelated hedge and more of a leveraged bet on liquidity and risk appetite.

Regulatory Clarity Accelerates

The regulation problem was finally solved in September 2025 when the SEC approved generic listing standards for crypto ETFs. This was a bigger deal than it sounds. Previously, every single ETF needed individual review that dragged on for 6-12 monthsç since the SEC essentially treated each application like a novel legal question. Under the new standards, qualifying crypto assets can launch ETFs within weeks. That’s how Solana, XRP, Litecoin, and others got approved so quickly in late 2025.

The regulatory progress extended beyond just ETFs. The GENIUS Act provided much-needed clarity around stablecoins, while Europe’s MiCA regulation created harmonized rules across all EU countries—ending the fragmented patchwork where each nation had different crypto policies.

And 2026 is shaping up to accelerate this trend further. Paul Atkins took over SEC leadership with a notably more crypto-friendly stance than his predecessor. Expect faster ETF approvals as the standard-setting, and don’t be surprised if the SEC relaxes its restrictions around staking for Ethereum ETFs.

Should You Buy the ETF or the Actual Crypto?

This comes down to what you’re actually trying to accomplish. Both approaches work, but they solve different problems.

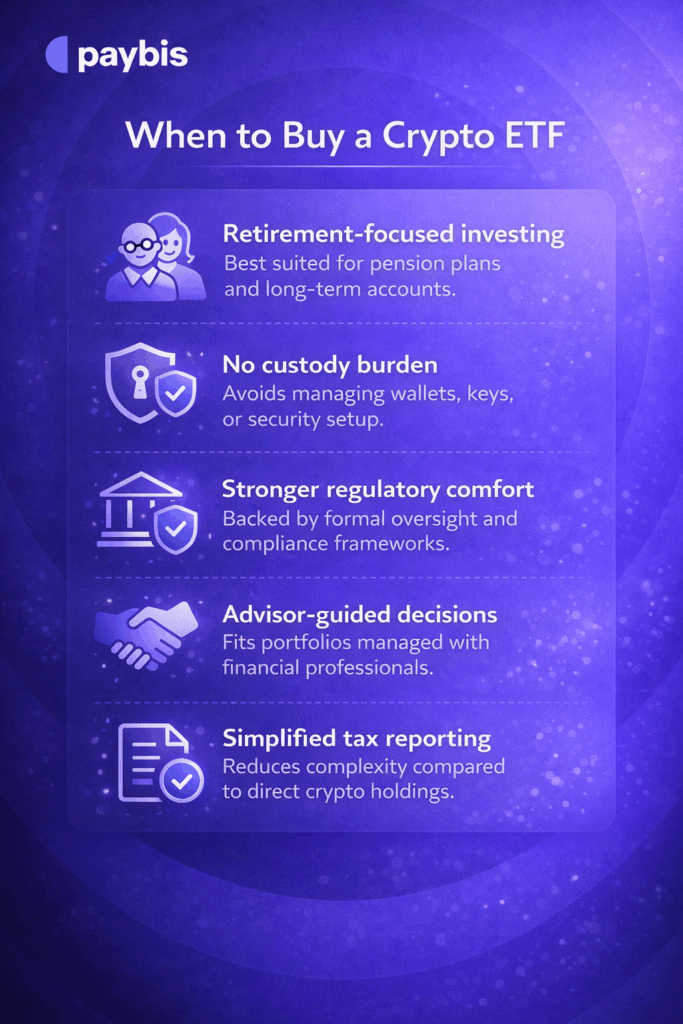

When to Buy the ETF

- You want it in a retirement account. Most IRA and 401(k) providers will hold ETFs but won’t touch actual cryptocurrency, which means the ETF is often your only path to crypto in tax-advantaged accounts. That’s a big advantage, since decades of tax-free compounding beats the small management fee.

- You don’t want custody responsibility. ETFs solve the security problem that scares off a lot of potential crypto buyers. BlackRock uses Coinbase Custody with institutional-grade cold storage, multi-signature wallets, and insurance coverage. You never see a private key, never worry about losing a seed phrase. The tradeoff is you’re trusting institutions. But for many investors, that’s exactly what they want.

- You value regulatory oversight. ETFs trade on SEC-regulated exchanges with investor protections baked in. SIPC insurance covers up to $500,000 if your brokerage fails, though that only protects against brokerage bankruptcy, not Bitcoin price drops. Still, it’s a layer of protection that doesn’t exist when you’re holding crypto on an exchange.

- You’re investing with a financial advisor. Advisors operate within compliance frameworks that allow ETF recommendations but rarely extend to direct crypto purchases. If you want professional guidance on your crypto allocation, the ETF is likely your only option.

- You want simplified tax reporting. Your brokerage sends you a 1099 form with everything calculated automatically. No tracking cost basis across multiple wallets and exchanges, no figuring out which transactions are taxable events. It just shows up on your tax forms like any other investment.

Fees: 0.20-0.25% annually for most Bitcoin ETFs. That’s $20-25 per year per $10,000 invested.

Trading hours: 9:30am-4pm ET, Monday-Friday. You can’t trade outside stock market hours even if Bitcoin moves overnight or on weekends.

When to Buy Crypto Directly

- You want true ownership. “Not your keys, not your crypto” is a core principle in the crypto community. When you control the private keys, no institution can freeze, seize, or restrict your access. That sovereignty matters to some investors more than convenience.

- You plan to use it for transactions. You can’t spend an ETF share, but you can spend Bitcoin or Ethereum. If you’re holding crypto for payments, DeFi protocols, or cross-chain transactions, you need the real thing. ETF shares sit in your brokerage account and do nothing except track price.

- You want 24/7 trading access. Crypto markets never close. If Bitcoin drops 15% on Saturday, you can react immediately. ETF holders wait until Monday morning. That liquidity difference matters during volatile periods, especially if you’re actively managing your position.

- You want to maximize returns. Direct Ethereum holders earn 3-4% staking yields that ETFs can’t provide due to SEC restrictions. Over the years, that yield difference compounds. Plus, you only pay trading fees when you buy or sell. No ongoing management fees are eating into returns.

- You’re willing to learn security practices. Hardware wallets, private key backups, and two-factor authentication protect your holdings. But they require effort to learn and discipline to maintain. Lost private keys mean lost crypto permanently. There’s no customer service number to call, no “forgot password” link. That finality scares some people and excites others.

Fees: Trading fees vary by exchange (0.1-0.5% per trade typically). Network fees apply when moving crypto between wallets. No ongoing management fees once you own it.

Risk: You’re responsible for security. Lost private keys = lost crypto permanently. No recovery process exists.

Which ETFs Are Winning (And Why IBIT Dominates)

Let’s look at the list of ETFs dominating the market.

BlackRock IBIT

IBIT has pulled $67.6 billion in assets in just over a year, capturing 50-60% of daily inflows across all Bitcoin ETFs. On January 2, 2026, for example, IBIT alone pulled $280.1 million out of $463.9 million total across all Bitcoin ETFs. That’s 60% market share in a single day.

BlackRock’s institutional credibility made IBIT the default choice for wealth managers and retirement plan administrators. When a financial advisor needs to add Bitcoin exposure to a client portfolio, they’re reaching for IBIT first. It’s now the fastest-growing ETF in history across all asset classes, not just crypto.

Expense ratio: 0.25% (first 12 months waived for early investors)

Fidelity FBTC

FBTC has accumulated over $13 billion since it has benefited heavily from Fidelity’s existing distribution network. Many retirement plans already use Fidelity as their 401(k) provider, so adding FBTC to plan menus was a natural extension. The brand recognition doesn’t hurt either. For investors who’ve trusted Fidelity with their retirement accounts for decades, FBTC feels like a safer bet than newer players.

Expense ratio: 0.25%

Grayscale GBTC

GBTC’s story is more complicated. It converted from a closed-end trust structure that used to trade at wild premiums and discounts to its actual Bitcoin value. Once it became a proper ETF, the floodgates opened for exits. Grayscale charges 1.50% annually, six times what BlackRock charges, and investors weren’t willing to pay that premium once they had alternatives. Many simply swapped their GBTC shares for IBIT or FBTC the moment the conversion allowed easy exits.

Despite the bleeding, GBTC still holds significant Bitcoin from early investors who got in years ago and haven’t bothered moving. Inertia is powerful, even when it costs you 1.25% extra per year.

Expense ratio: 1.50%

ARKB has accumulated over $3 billion, which is solid but nowhere near the BlackRock/Fidelity tier. Cathie Wood’s ARK Invest partnered with 21Shares for this offering, and it appeals to investors who already follow ARK’s innovation-focused philosophy. If you’re the type who owns ARKK or ARKW (ARK’s other thematic ETFs), ARKB feels like a natural addition to that portfolio.

The challenge is that institutional buyers tend to favor the bigger, more established names. ARKB does well with retail investors who like ARK’s brand, but it’s not winning the wealth management channel the way IBIT dominates.

Expense ratio: 0.21%

VanEck HODL

VanEck went aggressive on fees, charging just 0.20% to undercut most competitors by a few basis points. For large allocations, that 0.05% difference between VanEck and BlackRock actually matters. A $10 million Bitcoin position saves $5,000 annually with HODL versus IBIT.

The ticker “HODL” is a nice touch for crypto natives (it’s an old meme from a typo meaning “hold on for dear life”), but VanEck hasn’t captured massive market share despite the fee advantage. Distribution matters more than cost for most investors. Still, VanEck has carved out a respectable position by being the low-cost option for price-sensitive allocators.

Expense ratio: 0.20%

What Can Go Wrong With Crypto ETFs?

ETFs solve a lot of problems, but they create some new ones. Here’s what you’re actually risking.

Volatility Hasn’t Disappeared

Bitcoin ETFs track Bitcoin’s price with near-perfect accuracy, which sounds great until you remember what Bitcoin’s price actually does. When Bitcoin dropped 20% in November-December 2025, ETF holders lost 20% right alongside direct holders. The professional wrapper and SEC oversight don’t cushion the blow at all.

If Bitcoin crashes 50% tomorrow, your ETF crashes 50% with it. The regulatory structure changes, the custody arrangements change, but the underlying asset’s volatility doesn’t. You’re still riding the same wild price swings that make crypto, well, crypto.

Management Fees Compound Over Time

0.25% doesn’t sound significant. But over 30 years, it matters.

$10,000 invested at 8% annual returns:

- With 0.25% fees: $87,550 after 30 years

- With no fees: $100,627 after 30 years

The difference: $13,077 or 13% of your ending balance. For large portfolios, this adds up fast. A $1 million Bitcoin position pays $2,500 annually in management fees, every single year, regardless of whether Bitcoin goes up or down. Direct ownership has one-time trading fees when you buy or sell, but nothing ongoing.

Limited Trading Hours Create Risk

Bitcoin trades 24/7. ETFs trade 9:30 am-4 pm ET weekdays only. The difference creates real problems during volatile periods.

If Bitcoin crashes 30% on Sunday night (which has happened before), ETF holders just watch helplessly until Monday morning. By the time markets open, the damage is done, and you’re selling into panic. Direct crypto holders can react the moment it happens. That liquidity difference might not matter if you’re holding for years, but it absolutely matters if you need to exit during a crisis.

Tracking Error Exists

Most spot ETFs track Bitcoin’s price closely, but not perfectly. ETFs can trade at slight premiums or discounts to the actual Bitcoin price, usually around 0.1-0.3%. During high volatility, that spread can widen as market makers struggle to keep up with rapidly changing prices.

Futures-based ETFs have worse tracking error because of rolling costs and contango in futures markets. Over time, these costs accumulate and create noticeable performance drag compared to just holding Bitcoin directly.

Counterparty Risks Can Still Bite You

ETFs are more secure than sketchy crypto exchanges, but you’re still trusting multiple parties. The ETF issuer needs to manage the fund properly. The custodian needs to store Bitcoin safely without getting hacked. The exchange needs to settle trades correctly. Regulators need to maintain favorable rules and not suddenly ban crypto holdings.

FTX collapsed in November 2022 and vaporized $9 billion in customer funds overnight. That was an exchange, not an ETF, so the comparison isn’t perfect. But it proves that institutional failure happens in crypto, even with entities that looked legitimate and well-funded. ETFs have better oversight and insurance, but they’re not immune to catastrophic failure. The risk is lower, but never zero.

Staking and DeFi Are Off Limits

Ethereum ETF holders miss out on 3-4% annual staking yields because the SEC required issuers to exclude staking functionality. Bitcoin ETF holders can’t use Lightning Network for instant payments or participate in DeFi protocols that let you lend, borrow, or earn yield on your holdings.

ETFs give you pure price exposure and nothing else. If you care about earning yield or actually using crypto for its intended purposes beyond speculation, you need direct ownership. The ETF wrapper is convenient, but it walls you off from the broader crypto ecosystem.

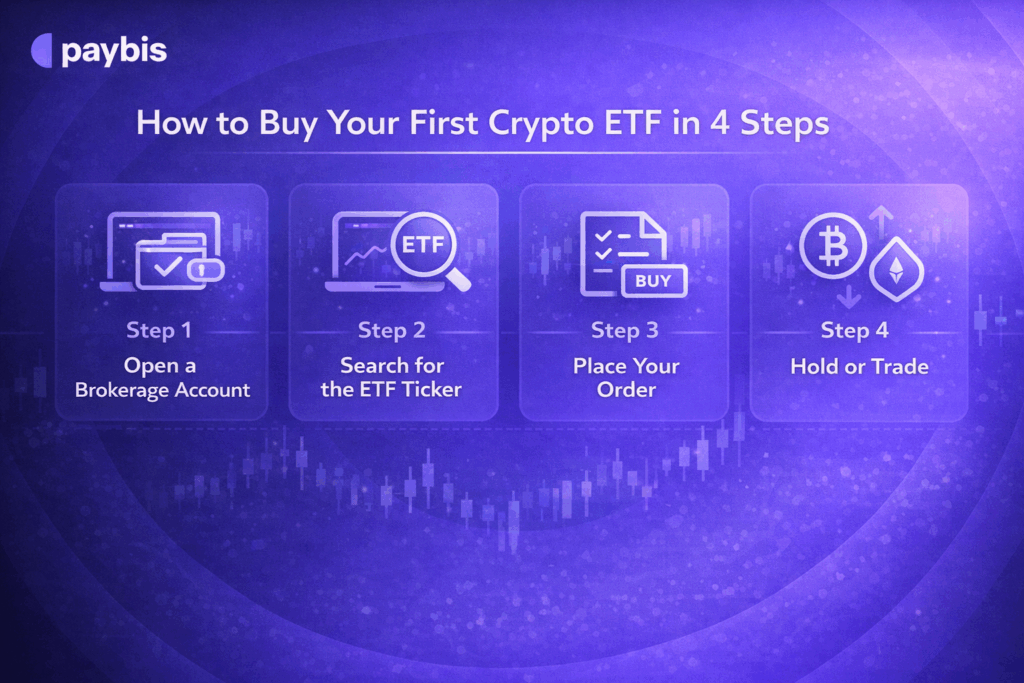

How to Buy Your First Crypto ETF in 4 Steps

The process is straightforward. If you’ve bought a stock before, you already know how to do this.

Step 1: Open a Brokerage Account

Any major brokerage offers crypto ETFs: Fidelity, Charles Schwab, Vanguard, TD Ameritrade, Robinhood, and Interactive Brokers. Pick whichever one you already use or whichever interface you like best. They all offer the same ETFs at the same prices.

Account approval typically takes 1-3 business days. Fund it via bank transfer, and you’re ready to go.

Step 2: Search for the ETF Ticker

Type the ticker symbol into your brokerage’s search bar just like you would for any stock

Bitcoin ETFs:

- IBIT (BlackRock)

- FBTC (Fidelity)

- ARKB (ARK 21Shares)

- HODL (VanEck)

- BITB (Bitwise)

Ethereum ETFs:

- ETHA (BlackRock)

- FETH (Fidelity)

- ETHE (Grayscale)

Solana, XRP, and others have multiple options, too. Search by ticker symbol in your brokerage platform.

Step 3: Place Your Order

For most people, a simple market order works fine. Click buy, enter how much you want to invest, and you’ll get shares at the current price within seconds. If you’re investing a large amount and want more control over your entry price, use a limit order instead to specify the exact price you’re willing to pay.

ETF shares trade exactly like stocks, and most brokerages let you buy fractional shares. This means $50 and $5,000 work equally well. You’re not forced to buy in whole-share increments.

Step 4: Hold or Trade

What you do next depends entirely on your strategy. Buy-and-hold investors might check their portfolio once a quarter. Active traders watch daily price movements. Neither approach is wrong, they’re just different.

The one thing that matters regardless of strategy is rebalancing. If crypto rips higher and suddenly represents 15% of your portfolio when you intended 5%, you probably need to trim some back. Most financial advisors recommend keeping crypto between 1-5% of a diversified portfolio, rarely more than 10% even for aggressive investors. That discipline prevents crypto volatility from dominating your entire portfolio’s performance.

How Crypto ETF Taxes Actually Work

The tax treatment is refreshingly simple compared to direct crypto ownership.

ETFs in Regular Accounts

Crypto ETFs get treated exactly like stock ETFs. When you sell shares at a profit, capital gains taxes apply based on how long you held them.

- Hold less than 1 year: Short-term capital gains taxed as ordinary income (10-37% depending on bracket)

- Hold more than 1 year: Long-term capital gains (0%, 15%, or 20%, depending on income)

Your brokerage handles all the reporting and sends you a 1099-B form at tax time with everything calculated. You just copy the numbers onto your tax return. That’s it.

ETFs in Retirement Accounts

This is where ETFs really shine. Inside a traditional IRA or 401(k), you pay no taxes until you withdraw in retirement. Gains compound completely tax-free for decades. Roth IRAs are even better if you follow the withdrawal rules; you never pay taxes on the gains at all.

Compare that to direct crypto, where moving Bitcoin between wallets triggers a taxable event. Want to rebalance your crypto holdings? That’s taxable. With an ETF inside an IRA, you can buy, sell, and rebalance as much as you want without any immediate tax consequences. The tax advantages alone justify the 0.25% management fee for many investors.

Direct Crypto Tax Treatment

Every single crypto transaction is a taxable event. Buying coffee with Bitcoin? Taxable. Swapping Bitcoin for Ethereum? Taxable. Moving coins between your own wallets? Potentially taxable depending on how you do it.

You’re responsible for tracking several factors at the moment of every trade. Most crypto exchanges provide terrible tax reporting, if they provide any at all. Third-party tax software like CoinTracker or Koinly can help, but that’s another $100-300 per year in costs, plus hours of your time reconciling transactions.

If simplifying your tax life matters to you, the ETF wins easily.

Bottom Line

Crypto ETFs pulled $107 billion in their first year. That’s faster adoption than any ETF category in history, and it happened after a decade of the SEC saying no.

The market will keep expanding in 2026. More coins getting ETFs, faster approvals, and potentially staking for Ethereum funds. Galaxy Research expects 100+ new launches with $50 billion in inflows.

ETF or direct crypto? Depends what you need. Retirement account and simple taxes? ETF. Staking yields and actual control? Direct ownership. Neither is wrong, as they just solve different problems.

Whether you buy IBIT or actual Bitcoin, you’re betting on the same price moves. Pick whichever wrapper fits your situation and stop overthinking it.

FAQ

What's the difference between a crypto ETF and buying Bitcoin directly?

A crypto ETF gives you Bitcoin price exposure through your brokerage account. You don’t own actual Bitcoin, you own shares of a fund that holds Bitcoin. Direct ownership means you control the actual cryptocurrency and private keys. ETFs trade during stock market hours (9:30am-4pm ET) with 0.20-0.25% annual fees. Direct crypto trades 24/7 with no management fees but requires you to handle security yourself.

Are crypto ETFs safe?

Crypto ETFs are regulated by the SEC and trade on major exchanges like Nasdaq. SIPC insurance covers up to $500,000 if your brokerage fails (doesn’t protect against Bitcoin price drops). BlackRock uses Coinbase Custody with institutional-grade cold storage and insurance. However, Bitcoin’s price volatility remains. If Bitcoin drops 50%, your ETF drops 50%. The regulatory wrapper doesn’t eliminate crypto’s price swings.

Which crypto ETF should I buy?

BlackRock’s IBIT (0.25% fee) dominates with $67.6 billion in assets and captures 60% of daily inflows. Fidelity’s FBTC (0.25% fee) is second with $13 billion. VanEck’s HODL offers the lowest fee at 0.20%. For Ethereum, BlackRock’s ETHA and Fidelity’s FETH are the top choices. Avoid Grayscale’s GBTC – it charges 1.50%, which is 6x higher than competitors.

Can I hold crypto ETFs in my IRA or 401(k)?

Yes. This is one of the biggest advantages of ETFs over direct crypto. Most retirement account providers allow ETF holdings but don’t allow direct cryptocurrency. You can get Bitcoin and Ethereum exposure inside traditional IRAs, Roth IRAs, and many 401(k) plans. Gains grow tax-free until withdrawal (or tax-free forever in a Roth IRA if you follow withdrawal rules).

Why can't Ethereum ETFs offer staking rewards?

The SEC required issuers to exclude staking to get approval. Direct Ethereum holders earn 3-4% annual yields by staking their ETH to secure the network. Ethereum ETF holders miss out on this income entirely. Paul Atkins taking over as SEC Chair in 2026 could change this policy. If staking gets approved for ETFs, they’ll become significantly more competitive with direct ETH ownership.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info