Is Crypto Exchange Verification Safe? What Happens to Your ID and Personal Data

Key Takeaways:Uploading your ID to a regulated crypto exchange is safe. Regulated platforms use industry-standard AES-256 encryption to secure your documents, the same standard banks use. KYC (identity verification) is a legal requirement for custodial exchanges and helps protect your account from fraud as much as it protects the platform. Paybis completes automated verification in under 2 minutes, holds PCI DSS Level 1 compliance, and has operated with zero security breaches since 2014. Your data is held to satisfy regulatory obligations and deleted when those obligations expire. Ready to get started? With Paybis, you can buy Bitcoin with a credit or debit card, buy BTC with a bank account, set up a crypto wallet, and use a dedicated Bitcoin wallet once your identity is verified.

Crypto assets can increase or decrease in value. Paybis is a payment gateway, not an investment service. This content is for informational purposes only and does not constitute financial advice.

You want to buy Bitcoin today, but the exchange is asking for your driver’s license and a selfie. Handing over your ID feels risky. You’ve seen news about data breaches, heard horror stories about identity theft, and you’re not sure which platforms you can trust.

Here’s what actually happens after you click “upload,” and why uploading your ID to a regulated exchange carries far less risk than most people assume.

Why Crypto Exchanges Require ID Verification

Every regulated, custodial crypto exchange must verify customer identities before processing financial transactions. This isn’t optional for platforms that hold your funds. It’s a legal requirement tied to global Anti-Money Laundering (AML) law.

KYC and AML Compliance Explained

KYC stands for Know Your Customer. AML stands for Anti-Money Laundering. Together, they form the legal backbone of regulated financial services, from banks to crypto exchanges.

Most national frameworks follow the FATF 40 Recommendations, which FATF calls upon all countries to implement. In the US, the Bank Secrecy Act (BSA) requires regulated financial businesses to verify customer identities, maintain records, and report suspicious activity.

Paybis maintains active regulatory registrations:

- FinCEN (US): US entity #31000272911973, PL entity #31000277275964

- FINTRAC (Canada): PL entity C100000816, CA entity C100000646, registration M22061209

- Revenue Chamber in Katowice (VASP in Poland): RDWW-805

Both FinCEN and FINTRAC require ongoing compliance with strict identity verification and data handling rules. You can read more about how these obligations apply in practice in Paybis’s guide to PayPal crypto regulations and compliance.

How Verification Protects You From Fraud

KYC isn’t just a checkbox for the exchange. It’s one of your account’s strongest protections against fraud. When a platform verifies your identity, it ties your account to a real, verified person. That makes it significantly harder for a bad actor to open an account in your name, drain funds, or use your identity to push money through the platform.

Without KYC, anyone can create an account using a stolen name and email, turning your funds into a target. Regulated verification stops synthetic identity fraud (where criminals combine real and fake data to create new identities) before it starts. Understanding why crypto users switch platforms often comes down to exactly these security and compliance differences.

Can’t Withdraw Funds Without ID

Anonymous accounts face legal restrictions by design. Under BSA and FATF rules, exchanges operating as regulated MSBs must verify customer identities before allowing fund withdrawals. This rule protects every verified user on the platform by keeping unverified accounts from accessing the withdrawal infrastructure.

Paybis’s support article on buying crypto without ID verification explains exactly which verification thresholds apply to different transaction sizes.

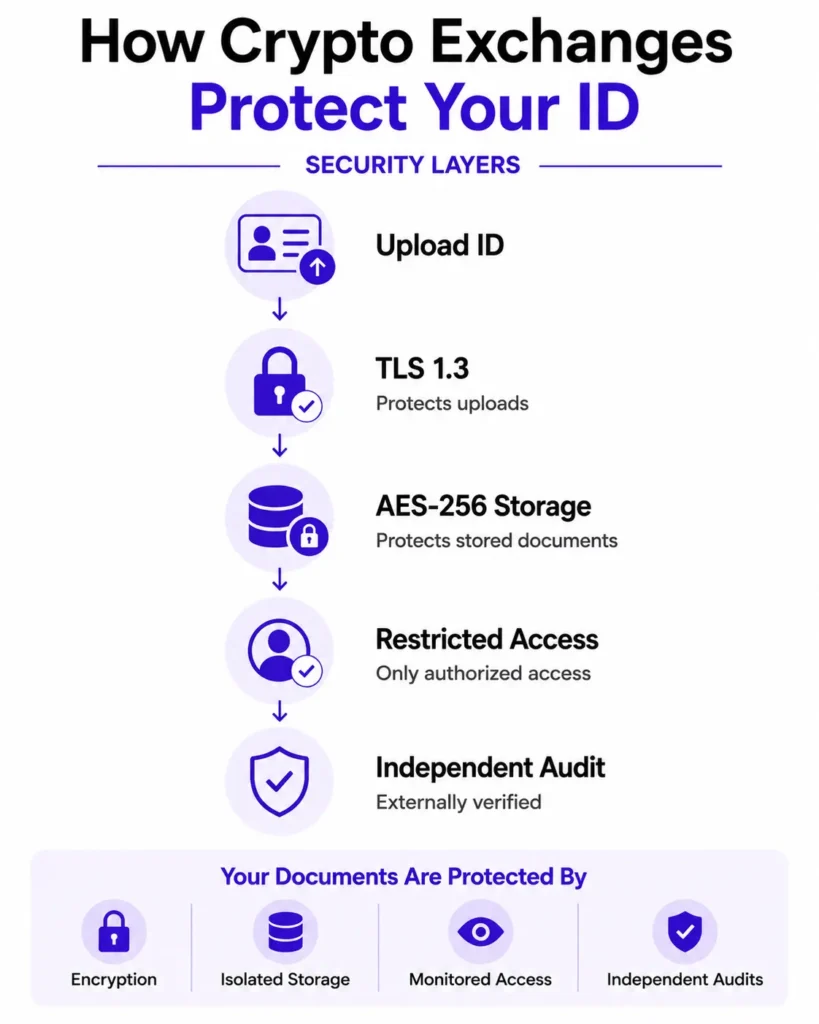

How Crypto Exchanges Protect Your ID Documents

After you upload your documents, they don’t sit in an open folder. Regulated exchanges apply layers of security that most users never see but absolutely rely on.

Data Secured by AES-256 and TLS

Your ID document travels through two phases: transit (the upload) and rest (storage). Regulated platforms protect both.

- In transit: Transport Layer Security (TLS 1.3) creates an encrypted tunnel between your browser and the exchange’s servers. TLS 1.3 is the current NIST benchmark for securing data moving across networks, ensuring no one can intercept your upload mid-transfer.

- At rest: AES-256 encryption (Advanced Encryption Standard with a 256-bit key) locks stored documents. Banks and government agencies use the same standard. Even if attackers physically accessed a server, they couldn’t read the data without the decryption key. NIST’s AES guidelines confirm AES-256 has never been broken in over two decades of real-world deployment.

ID Document Storage Systems

Regulated exchanges typically store ID documents separately from account login and transaction history databases. Best practice in financial data security involves limiting access to identity documents so that each system operates with only the permissions required for its specific function. This data minimization principle means that even if attackers compromised one part of the platform, they couldn’t automatically access your identity documents.

Paybis’s approach to custody and data protection is outlined in its guide to custodial risk management, which explains how different systems are isolated to protect user assets and information.

Monitoring and Limiting Data Access to Your ID

Regulated exchanges are required to maintain audit trails for access to sensitive customer data under FinCEN, FINTRAC, and EU licensing frameworks, meaning access to identity documents is logged and attributable.

Regulated exchanges implement internal access controls designed to limit exposure of identity documents to authorised systems and personnel only.

Third-party Security Audits

Credible exchanges prove security through external audits, not just internal claims. ISO/IEC 27001 is the internationally recognized standard for information security management, requiring organizations to identify, assess, and manage data security risks systematically. SOC (System and Organization Controls) 2 covers security, availability, processing integrity, confidentiality, and privacy, with independent auditors verifying that controls actually operate as documented, not just that they exist on paper. Knowing how to choose which exchange to buy Bitcoin from starts with checking for exactly these kinds of third-party certifications.

Strict Standards for Your Information Security

Regulated exchanges don’t write their own security rules. They operate inside globally enforced legal frameworks that define exactly how personal data must be handled.

GDPR Compliance for EU Users

If you’re in the EU (or the UK under UK GDPR), the General Data Protection Regulation gives you the right to request deletion of your personal data, known as the “Right to be Forgotten.” Under GDPR Article 17, organizations must delete your data when it’s no longer necessary for its original purpose or when you withdraw consent. The key exception: financial services platforms must retain certain records for a legally mandated period before deletion can apply.

How SOC 2 Protects Your ID Data

SOC 2 defines five trust service principles: security, availability, processing integrity, confidentiality, and privacy. For exchanges that undergo SOC 2 audits, an independent auditor verifies that controls are in place and operating effectively across all five dimensions. A third party with no financial stake in the outcome confirms that the platform is demonstrably protecting your data, not just claiming to.

How FinCEN and FINTRAC Secure Your Data

Both FinCEN (US) and FINTRAC (Canada) require registered MSBs to maintain customer identity records, implement AML controls, and report suspicious activity. These registrations also subject exchanges to regulatory examination, meaning government auditors can inspect compliance at any time.

Paybis holds active FinCEN registration and FINTRAC registration, placing it under ongoing oversight across multiple jurisdictions.

How PCI DSS Protects Your Card Information

PCI DSS Level 1 is the highest certification available for payment card data security, and Paybis holds it. The PCI Security Standards Council requires Level 1 certified entities to undergo annual on-site assessments by a Qualified Security Assessor and quarterly network scans. Your card data and identity documents are processed within an audited, enterprise-grade security environment.

Your ID’s Journey on Crypto Exchanges

Understanding the lifecycle of your data from upload to deletion removes most of the anxiety around the process.

Secure Steps to Verify Your ID

Most exchanges offer two primary verification approaches: document upload (a photo of your passport or driver’s license plus a selfie) or manual review (a human agent examines the documents). Here’s how they compare:

| Method | Speed | Security Level | User Friction |

|---|---|---|---|

| Document upload + selfie (Paybis) | Under 2 minutes | PCI DSS Level 1 certified | Low |

| Manual review (other regulated exchanges) | Hours to days | Regulatory compliant | High |

Paybis uses automated document upload with a photo ID and selfie. The process takes under 2 minutes for most users, compared to manual review queues at other regulated exchanges that can stretch to hours or days. The full Paybis KYC verification walkthrough is available on their YouTube channel, and a quick account verification guide covers specific steps for new users. An independent review by TradingFinder also covers the process from a third-party perspective.

Stopping Fraud With Transaction Data

After verification, your identity documents are cross-referenced against your transaction behavior. If an account suddenly starts sending large amounts to unfamiliar wallet addresses from a new device and IP address, fraud detection flags the activity. Your verified identity creates a behavioral baseline, so unusual activity stands out immediately and triggers review before funds move. For a broader look at how exchanges approach security and trust, the Paybis crypto exchange trust scores overview explains the metrics used to evaluate platform reliability.

Securely Deleting Your Personal Information

One of the most common fears is that your ID will be stored forever. Here’s how retention and deletion actually work.

Exchange Data Storage Periods

The Bank Secrecy Act requires most financial records, including customer identity records, to be retained for at least five years. Exchanges don’t choose this retention period. Anti-money laundering laws require it to maintain an audit trail. The five-year clock typically starts from account closure. After that period, platforms must purge records that no longer serve a legal purpose.

Removing Your ID From the Exchange

Under GDPR (for EU/UK users), you can formally request data deletion through the Right to Erasure process. The platform must respond within 30 days. Outside the EU, most regulated exchanges offer account closure processes that trigger data review and deletion in compliance with their registered jurisdiction’s retention laws.

Paybis: When Your ID Data Is Deleted

Paybis retains KYC data for the legally mandated period under MiCA, CASP, FinCEN (US), FINTRAC (Canada), and relevant EU/UK frameworks. Once those obligations no longer apply, the data is purged. This policy is consistent with how banks and traditional payment processors handle regulated identity records. Further details are available in Paybis’s privacy and security documentation.

Safeguard Your ID: Limit Exchange Data Access

Uploading your ID to a regulated platform is safe. But your personal security doesn’t stop there. Here’s what you control on your end.

Avoid Private Key Theft and Scams

No regulated exchange needs your wallet’s private key or your account password to process a transaction. Your private key is the unique code that proves ownership of your crypto. Sharing it with anyone is the equivalent of handing someone your bank account credentials. If anyone claiming to be support staff asks for your private key, end the conversation immediately. The Paybis crypto security overview covers the top scam tactics targeting crypto users, including private key phishing.

Protect Your Crypto Account Login

Use a unique, strong password for your Paybis account and don’t reuse it across other platforms. Password managers generate and store complex passwords without requiring you to memorize them. A breach on an unrelated platform can’t compromise your crypto account if the passwords are different. It’s also worth understanding how often you should buy Bitcoin and whether your account activity patterns align with the security habits that keep accounts safest.

Protect Your 2FA Codes From Scammers

Two-factor authentication (2FA) adds a second layer beyond your password. Authenticator apps are more secure than SMS codes because they can’t be intercepted through SIM-swapping attacks. Never share a 2FA code with anyone over chat, email, or phone. Paybis’s guide on SMS verification issues helps users troubleshoot without compromising account security.

Spotting Scam Crypto Exchanges

Before uploading your ID to any platform, run through this checklist:

- Regulatory registration: Is the platform registered with FinCEN, FINTRAC, FCA, or another major regulator? Registrations are publicly searchable on government websites.

- Transparent fees: Does the platform show all fees before you confirm the transaction? Post-transaction fee surprises are a red flag.

- Verifiable business identity: Is there a registered business address and company registration number? Paybis Ltd is registered in Scotland, company number SC533961, at 1 West Regent Street, Glasgow.

- Support availability: Can you reach a human before making a purchase? Test the live chat before committing funds.

- Track record: How long has the platform operated? Does it appear on independent review sites like Trustpilot?

- No KYC required: Platforms that let you buy large amounts of crypto without any verification operate outside regulated frameworks and carry far greater security risks than completing a standard ID check.

For a detailed breakdown of what separates trustworthy platforms from risky ones, the guide to choosing the best crypto app is a useful reference before committing to any exchange.

How Paybis Protects Your Personal Information

Paybis has processed over $1.2 billion in annual transaction volume (last 12 months as of October 2025), served 5M+ retail users across 180+ countries, and supports 20+ payment methods and 90+ cryptocurrencies. It has done this since 2014 with zero security breaches, and that track record is independently verifiable.

Security Certifications and Compliance

Paybis maintains active regulatory licences and registrations:

- MiCA CASP authorisation (EU): issued by the Bank of Latvia, passporting across all 27 EU member states.

- Payment Institution (PI) licence (EU): issued under PSD2 by the Bank of Latvia.

- FinCEN (US): US entity #31000272911973, PL entity #31000277275964.

- FINTRAC (Canada): PL entity C100000816, CA entity C100000646, registration M22061209.

- VASP (Poland): registration RDWW-805, entered in the virtual currency activities register maintained by the Tax Administration Chamber in Katowice.

An independent review by Benzinga confirms Paybis’s regulatory standing, and Paybis’s UK registration is independently verifiable on the FCA Financial Services Register.

How Paybis Encrypts Your ID

Paybis applies industry-standard AES-256 encryption to stored identity documents and uses TLS for data in transit, covering both primary attack vectors: interception during upload and unauthorized access to stored files. The payment infrastructure is PCI DSS Level 1 certified, covering card processing alongside identity data protection under a unified enterprise-grade security framework.

Verify Your ID in 2 Minutes

The verification process on Paybis is automated and takes under 2 minutes for most users: upload a photo of your government-issued ID and take a selfie. The automated system checks document authenticity in real time with no multi-day manual review queue.

Here’s how that compares:

- Upload your government-issued ID (passport or driver’s license)

- Take a selfie for liveness verification

- Automated system checks document authenticity in real time

- Verification complete and ready to purchase

Manual verification at other regulated exchanges has been reported to take anywhere from hours to several days for new users, depending on document volume and review queues. Paybis’s step-by-step KYC guide walks through the verification process.

How Paybis Handles Your Verified ID

Once verified, documents move to isolated, encrypted storage with access controls limiting internal viewing permissions. Data is retained for the legally mandated period under relevant financial regulations in each registered jurisdiction, then purged. The Paybis safety overview addresses these security practices for users who want a visual walkthrough.

Trusting Crypto Verification: Common Concerns

Preventing ID Theft from Uploaded ID

When you upload your ID to a regulated exchange, the document isn’t stored as an open file. It’s encrypted immediately, logged under your account, and accessible only through controlled internal systems. The regulated audit trail means any access is logged, timestamped, and attributable.

Exchange Hack: Is My ID Exposed?

Data breaches do happen across the tech industry, but AES-256 encrypted data is unreadable without the decryption key, even if a server is physically accessed. The Paybis crypto safety overview emphasizes that strong encryption renders stolen data computationally useless for any practical attacker. Paybis has operated since 2014 without a single confirmed security breach.

Trust Signals for Crypto Exchanges

Paybis has 31,430+ Trustpilot reviews with a 4.1 “Great” rating, and active government registrations across three major financial jurisdictions. These are independently verifiable signals, not self-reported claims.

Paybis requires 2FA for account access and applies identity verification across all transaction tiers as part of its regulatory compliance under FinCEN and FINTRAC.

Is Uploading My ID Safer than Not Verifying?

“No-KYC” platforms might seem more private, but they carry a significantly higher risk of operating without regulatory oversight. Without FinCEN or FINTRAC registration, there’s no government examination, no legal obligation to protect your data, and no recourse if the platform disappears with your funds. Uploading your ID to a FinCEN-registered, PCI DSS Level 1-certified exchange like Paybis is demonstrably safer than trusting an anonymous platform that skips verification entirely.

Paybis accounts can be opened online. Identity verification is automated and takes under 2 minutes for most users. The platform shows complete fee transparency, fees start from 1.49%, and the complete breakdown (service, processing, and network fees) is displayed before confirmation.

Key Terminology

- KYC (Know Your Customer): The legal process by which regulated financial institutions verify customer identity using government-issued documents. Custodial exchanges are required to complete KYC checks under FATF-aligned AML frameworks in their registered jurisdictions.

- AES-256 (Advanced Encryption Standard, 256-bit): The encryption algorithm used to secure stored data, including identity documents, at rest. It is the same standard used by banks and government agencies and has never been broken in practical deployment according to NIST cryptographic standards.

- PCI DSS Level 1: The highest certification level issued by the PCI Security Standards Council for entities that handle payment card data. It requires annual on-site security assessments by a qualified auditor. Paybis holds this certification for its payment infrastructure.

- TLS (Transport Layer Security): The encryption protocol that secures data while it travels between your device and a server. When you upload your ID, TLS creates an encrypted tunnel that prevents interception. TLS 1.3 is the current NIST-recommended standard for financial data transmission.

- SOC 2: A security auditing framework created by the AICPA evaluating a service organization’s controls across five trust principles: security, availability, processing integrity, confidentiality, and privacy. External auditors verify that controls are not just documented but actively operating.

- 2FA (Two-Factor Authentication): A security feature that protects accounts by requiring a second verification method, such as a one-time code or biometric check, in addition to a password.

- AML (Anti-Money Laundering): A set of compliance procedures used by financial companies to identify suspicious activity, verify customer identities, and prevent illegal funds from entering the financial system.

FAQ

How long does Paybis keep my ID after I verify?

Paybis retains KYC documents for the legally mandated period required under its registered jurisdictions, which is a minimum of five years post-account closure under the Bank Secrecy Act. After that period, data no longer needed for legal compliance is purged.

Does Paybis sell my personal data to third parties?

Paybis holds identity data to satisfy AML/KYC regulatory requirements under its FinCEN and FINTRAC registrations. Personal information may be shared with third-party service providers for KYC/AML verification and document verification checks, and may also be shared with financial institutions, insurance companies, or other companies in the event of a merger, divestiture, or other corporate reorganization. Paybis may report aggregate, non-identifying statistical data about user browsing actions and patterns to advertisers; this data does not identify any individual and is not personal data.

What happens if Paybis gets hacked? Is my ID exposed?

Paybis has had zero security breaches since its founding in 2014. Even in the event of a breach, AES-256 encrypted data is computationally unreadable without the decryption key, making stolen documents practically unusable for identity theft.

Can I use Paybis without uploading my ID?

Very limited transactions may be possible at the lowest tier, but full account access, including the ability to withdraw funds, requires identity verification. This is a legal requirement under AML regulations across all of Paybis’s registered jurisdictions.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info