Navigate Crypto Fees: What You Actually Pay and How to Reduce It

- The amount you pay for crypto is built from several separate costs, not a single fee. Seeing them apart is the first step to paying less.

- The advertised fee percentage rarely tells the full story. What matters is net received, the amount of crypto or cash that actually reaches your account after every cost.

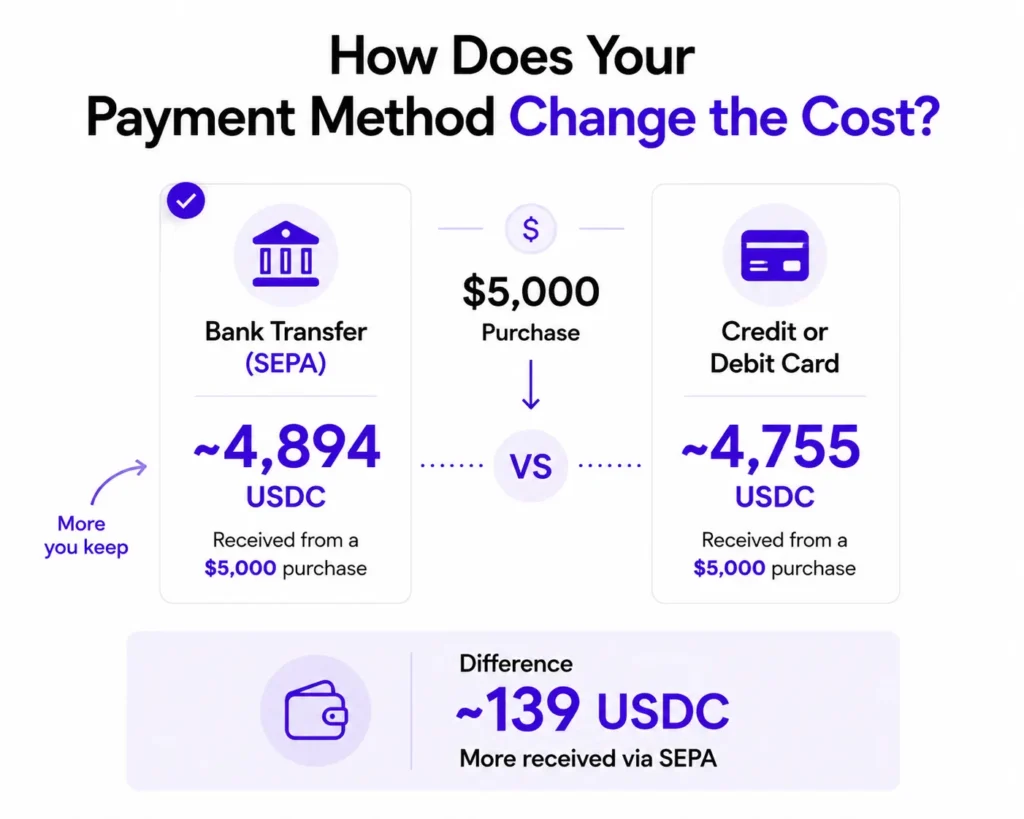

- Your payment method changes the result more than most people expect. Bank transfers carry less overhead than card payments because fewer intermediaries sit in the middle.

- On a $5,000 USDC purchase, choosing a bank transfer over a card can leave around 139 USDC more in your wallet, on the same platform and the same asset.

- Paybis shows each fee as a separate line at the quote stage, so you see the full cost before you confirm. You can buy crypto on Paybis and see the breakdown for yourself.

When you buy $100 of Bitcoin, the amount that leaves your account is usually a little more than $100. Other times, the crypto you receive is worth slightly less than you expected. Either way, the gap has a name. Fees.

Most people know fees exist. Far fewer know how many there are, where each one goes, or how much of the final price they get to control. That last part is the useful one, because some of these costs depend on choices you make before the transaction even starts.

This guide breaks down what you actually pay when you buy or sell crypto and where each cost comes from. It also covers the practical ways to keep more of your money. The figures here come from Paybis research that measured real outcomes across more than 20 platforms and every major payment method.

What are crypto fees, and why do you pay them?

Crypto fees are what you pay to buy or sell a digital asset and have it settle. Some of that money keeps the platform running, while the rest goes to the blockchain and to whoever processes your payment.

Think of changing money before a trip. The board shows a rate, you hand over your cash, and you get back a little less than the headline number suggested because the exchange takes a margin on top. Crypto works in a similar way. The difference is that more than one party is involved at the same time, and each one adds a small cost for the part it handles.

So the fees are not arbitrary. A platform charges to cover the cost of running a secure service and keeping support available. The blockchain charges to record your transaction. The card network charges when you pay by card. Once you can see which cost belongs to which player, the final price stops looking like one mysterious number and starts looking like something you can influence.

What makes up the price when you buy crypto?

The price has more than one part, and each part is charged by a different player. Most platforms fold them into a single number at checkout, which is exactly why the total can feel hard to read. Seeing them apart makes it easier to tell where your money goes.

- The service fee. This is what the platform charges to run things, from the technology behind the scenes to the support team available around the clock. It usually shows up as a percentage of the order, often with a small minimum for very small purchases.

- The payment processing cost. This depends entirely on how you pay. Bank transfers move through fewer intermediaries, so they cost less. Card payments include a fee from the card network, which is why paying by card tends to land at the higher end.

- The network fee. This one does not go to the platform at all. It goes to the blockchain that records your transaction, and it rises or falls with how busy that network is at the moment.

- The exchange rate spread. This is the least visible cost. It is the gap between the real market price of an asset and the price you are offered, folded quietly into the rate rather than listed as a line item.

Why the advertised fee doesn’t match what you actually pay

The advertised percentage can be misleading because it often leaves out the spread. A platform promoting a 1% fee can still deliver less crypto than one charging 2%, if its exchange rate is wider. The headline number only describes part of the cost.

This is why net received matters more than any single fee. Net received is the amount of crypto or cash that reaches your account once every cost has been taken out. It is the one figure that captures the whole picture, because it already includes the spread that a percentage can hide.

Paybis research measured outcomes this way on purpose. Rather than comparing advertised fees, it tracked how much crypto you receive for a fixed amount of money spent. The logic is simple. If you spend the same amount on two platforms and one sends you more crypto, that platform gave you the better deal, whatever each one calls its charges.

How does your payment method change the cost?

Your payment method is one of the biggest factors you control, and you decide it before the transaction even begins. Bank transfers such as SEPA in Europe and ACH in the US carry the least overhead, because the money passes through fewer hands. Cards cost more, since the card network adds its own fee on top.

The size of that gap surprises most people. On a $5,000 USDC purchase, choosing a bank transfer over a card can leave around 139 USDC more in your wallet. Same platform, same asset, with the only difference being the rail the money travelled on.

Digital wallets such as Apple Pay or Google Pay usually sit somewhere between the two. The point is not that one method is always correct. It is that the choice is yours, and it has a real cost attached before you have bought anything.

These are data observations from a point-in-time comparison, not financial advice.

Does the transaction size affect how much you can save?

Yes. The larger the transaction, the more your payment method matters. At small amounts the difference between rails is real but minor. As the amount climbs into the thousands, the same percentage gap turns into a much larger figure in your wallet.

A few cents saved on a $100 order is easy to ignore. The same percentage applied to a $5,000 order is meaningful money. This is the reason a careful choice of rail rewards larger buyers the most, and why it is worth pausing on the payment screen before a big purchase rather than after it.

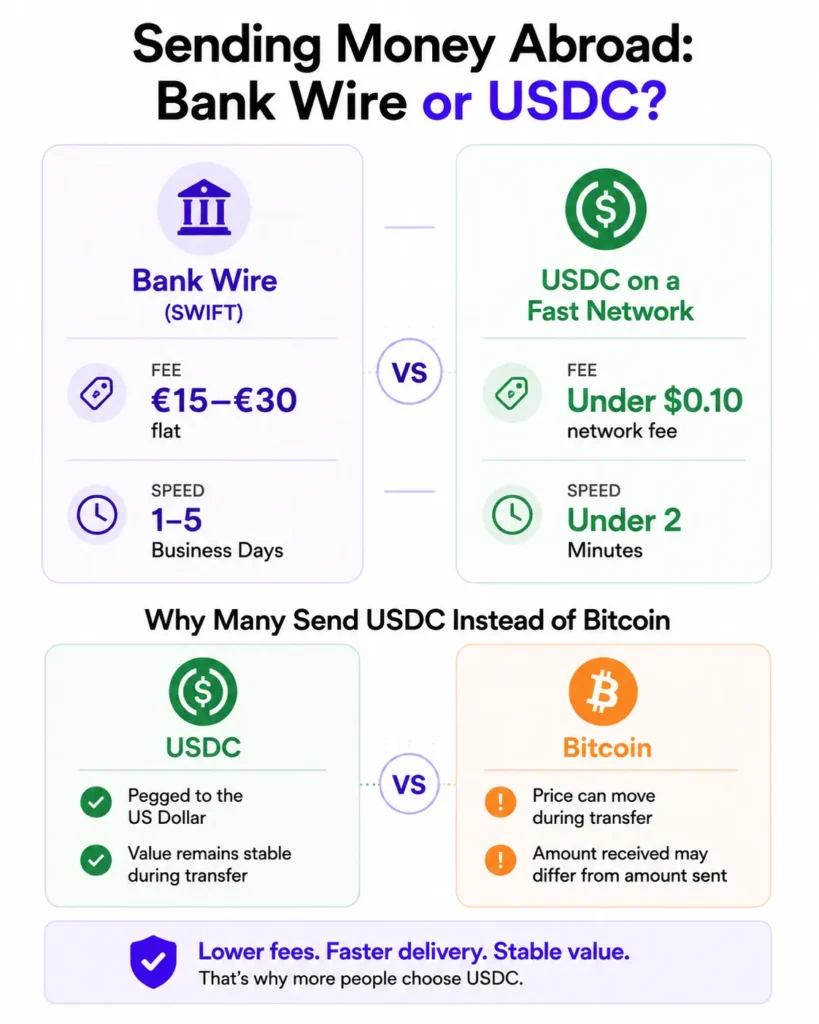

What about selling crypto or sending it across borders?

Selling works on the same logic as buying, and the rail you choose still decides how much cash reaches you. When you sell crypto for euros, a bank transfer such as SEPA tends to be the most cost-effective way to receive the money.

Sending crypto abroad adds one more decision: which asset to send. Some people buy stablecoins in Europe and send them to family overseas, where the funds are converted to local currency. Bitcoin’s price can move between the moment you send and the moment it arrives, so the amount received may differ from the amount sent. USDC is pegged to the US dollar, which keeps the value steady in transit and means what you send is close to what arrives.

Seeing the fee and the settlement time side by side makes the trade-offs clear, so you can match the method to the situation in front of you.

How can you reduce what you pay in fees?

Most of the savings come from two decisions you make before you start: how you pay, and whether you are buying or selling. A few habits cover the rest.

- Pay by bank transfer when you can. SEPA and ACH carry the least overhead, so more of your money ends up as crypto rather than as fees.

- Judge platforms by net received, not the headline percentage. The amount that reaches your wallet already includes the spread, which makes it the honest basis for any comparison.

- Match the asset to the job. For transfers where stability matters, a dollar-pegged stablecoin such as USDC avoids the price swings that come with assets like Bitcoin.

- Check the breakdown before you confirm. A platform that shows each fee as a line item lets you see the cost while you can still change your payment method, rather than discovering it once the order is placed.

How Paybis works: fee guide

Paybis charges a service fee of 1.49%, with a minimum of 2 USD on very small orders All fees are shown beforehand. That fee also covers the foreign exchange cost, and common currencies such as USD, EUR, and GBP tend to sit at the lower end. The network fee is shown separately and goes to the blockchain, never to Paybis.

There is also a 0% service fee on your first purchase of each asset with a card. Paybis takes nothing on top for that first buy. It applies to each asset on its own, so a first Bitcoin purchase and a first USDC purchase each qualify. The service fee line still appears at checkout, showing zero, so you can see exactly what is happening.

| Component | What it covers | Where it goes |

|---|---|---|

| Service fee (1.49%, min 2 USD) | Running the platform and the FX cost | Paybis |

| Payment method cost | Depends on how you pay | Card network or bank rail |

| Network fee | Recording your transaction | The blockchain |

Every component appears as its own line at the quote stage, in real currency, before you confirm. Many platforms only reveal the full cost once you reach checkout, after card details are entered.

This design was not a guess. When Paybis researched how people want to see fees, 84.9% preferred a full breakdown over a single bundled total, and 88.9% wanted exact amounts in their own currency rather than percentages. The quote screen was built around what that research showed.

Bottom Line

The real cost of buying crypto is rarely the number on the banner. It is the sum of a few separate charges, plus the spread that hides inside the exchange rate. The good news is that the largest part of it sits in your hands. Pay by bank transfer where you can, judge platforms by what actually reaches your wallet, and check the breakdown before you confirm.

Crypto is still new for a lot of people. The fees around it do not need to be complicated.

About Paybis

Paybis has operated since 2014 and now serves more than 6.9 million users across over 190 countries, with support for more than 90 cryptocurrencies. The platform holds a MiCA CASP licence and a Payment Institution licence, both issued by the Bank of Latvia. The Payment Institution licence covers crypto-related activities only, and the CASP licence passports across all 27 EU member states and the wider EEA.

Paybis is also registered with FinCEN in the US (MSB #31000272911973) and FINTRAC in Canada (#C100000816). It holds a VASP registration in Poland (#RDWW-805) and is registered with the FCA in the UK. Client funds are held separately from Paybis’ assets.

Paybis holds a 4 out of 5 rating on Trustpilot across more than 30,000 reviews. Support is available around the clock and typically responds within one to two minutes across the web platform and the iOS and Android apps.

This article is published for informational and educational purposes only. Nothing here constitutes financial, investment, or legal advice. Figures reflect a point-in-time comparison and may change as market conditions and pricing evolve.

Notice to Readers: This blog’s content is not intended for the UK audience. For a detailed understanding of associated cryptocurrency risks, consult our Risk Disclosure page.

FAQ

What is net received, and why does it matter more than the fee percentage?

Net received is the amount of crypto or cash that actually reaches your account once every cost has been deducted. It already includes the service fee, the payment cost, the network fee, and the exchange rate spread, so nothing is left hidden. A headline percentage only describes one slice of the cost, which is why two platforms with the same advertised fee can hand you different amounts of crypto. The spread is the usual reason for that gap, because it sits inside the rate rather than on a separate line. When you compare offers, the amount that lands in your wallet is the figure that tells the truth. That is the number worth checking before you confirm anything.

Is it cheaper to buy crypto with a bank transfer or a card?

Bank transfers such as SEPA in Europe and ACH in the US are usually the cheaper route, because the money passes through fewer intermediaries on its way to the platform. Card payments add a fee from the card network, which is why they tend to cost more for the same purchase. The gap is small on tiny orders but grows as the amount rises. On a $5,000 USDC purchase, a bank transfer can leave around 139 USDC more in your wallet than a card would, on the same platform and the same asset. Digital wallets sit somewhere in between. Your situation decides which method is practical, but the cost difference is real and worth a look before you pay.

What is the crypto network fee, and does Paybis keep it?

The network fee is paid to the blockchain that records your transaction, and it does not go to Paybis. It exists because the network needs to be paid for the work of settling and confirming your transfer. The amount moves with how busy the network is, so a quieter network costs less and a congested one costs more. This is why the same transaction can carry a different network fee at different times of day. Paybis shows this fee as its own line before you confirm, so you can see the exact amount rather than finding it folded into a single total.

Does the first purchase on Paybis really carry a 0% service fee?

Yes. The first time you buy a given asset with a card, Paybis takes nothing on top as a service fee. It applies to each asset separately, so a first Bitcoin purchase and a first USDC purchase each qualify on their own. The service fee line still appears at checkout, simply showing zero, so the breakdown stays clear and you can see what is happening. The network fee and any payment cost are shown separately, since those go to the blockchain and the payment rail rather than to Paybis. After that first purchase of an asset, the standard service fee applies to later buys of the same asset.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info