Crypto Regulation in Europe: What’s Changing and Why It Matters

- MiCA, the EU’s unified crypto regulation, came into full force in December 2024. It is the most comprehensive crypto framework in the world.

- Before MiCA, a crypto exchange could serve millions of EU users with little more than a basic AML registration. That is no longer legal.

- Under MiCA, exchanges must keep your funds separate from their own, show fees before you confirm a transaction, and follow a formal complaints process.

- Any platform serving EU users now needs a CASP licence, issued by a national financial regulator after a full review of the business.

- FTX collapsed without any of these rules applying. MiCA exists largely because of what happened when they did not.

- More regulation is coming. DeFi and NFT markets are under active review for a follow-on framework.

In December 2024, every crypto exchange operating in Europe either had formal authorization from a financial regulator or was breaking the law. That was new. As recently as 2023, you could run a crypto platform serving millions of European users with nothing more than a registration number and a basic anti-money laundering policy. The bar was low. The protections for users were minimal. And the consequences of that showed.

MiCA changed it. Europe built the most comprehensive crypto regulatory framework in the world, and it came into full force in December 2024. This article covers what actually changed, why it happened, and what it means if you buy or hold crypto in Europe today.

What Is MiCA and What Did It Change?

MiCA stands for Markets in Crypto-Assets Regulation. It is the EU’s unified legal framework for cryptocurrency, and it replaced a patchwork of inconsistent national rules that had been in place since Bitcoin went mainstream.

Before MiCA, each EU country handled crypto its own way. Germany had its own licensing regime. France ran a separate registration system. Some countries had almost nothing. An exchange authorized in one country had no automatic right to serve users in another, which meant the rules varied dramatically depending on where your platform happened to be based.

MiCA ended all of that. One regulation now applies uniformly across all 27 EU member states. Every crypto platform serving users in the EU operates under the same rules, enforced by the same framework. A single authorization in any member state covers the entire European market of 450 million people. That passporting mechanism is one of the most significant practical changes MiCA introduced, and it means that where a platform is registered now tells you far less than whether it holds a valid CASP licence.

If you buy crypto through a licensed platform in Europe today, you are buying through a business that a financial regulator has reviewed and approved. That was not guaranteed before December 2024.

Why Did Europe Build New Crypto Regulation?

The short answer is FTX. The longer answer starts a few months earlier.

In May 2022, the Terra/Luna ecosystem collapsed. Roughly $40 billion in value was wiped out in under 48 hours. A token that millions of people held as a stable store of value went to zero. There was no regulated redress. There was no regulator with jurisdiction to investigate. There were no protections because no framework required them.

Six months later, FTX filed for bankruptcy. An exchange that had been one of the largest in the world by trading volume turned out to have been using customer funds for its own purposes. Approximately $8 billion in customer assets were missing by the time administrators started counting. Again, the users who lost money had no protected legal claim to their funds, because the rules that would have required segregation simply did not exist in the jurisdictions where FTX operated.

Europe had been building MiCA since 2020. Both collapses accelerated the political momentum to finish it. The European Parliament passed the regulation in April 2023, and by December 2024 the full framework was in force. The goal was to make the EU a place where people could use crypto through platforms held to the same standards as any other regulated financial services provider. The rules that FTX was allowed to ignore are now mandatory under MiCA.

What Do the New Rules Actually Require From Crypto Platforms?

MiCA places significant obligations on any platform operating in the EU. Some of them are about protecting users directly. Others are about ensuring the platform can actually survive the pressures that the industry regularly generates.

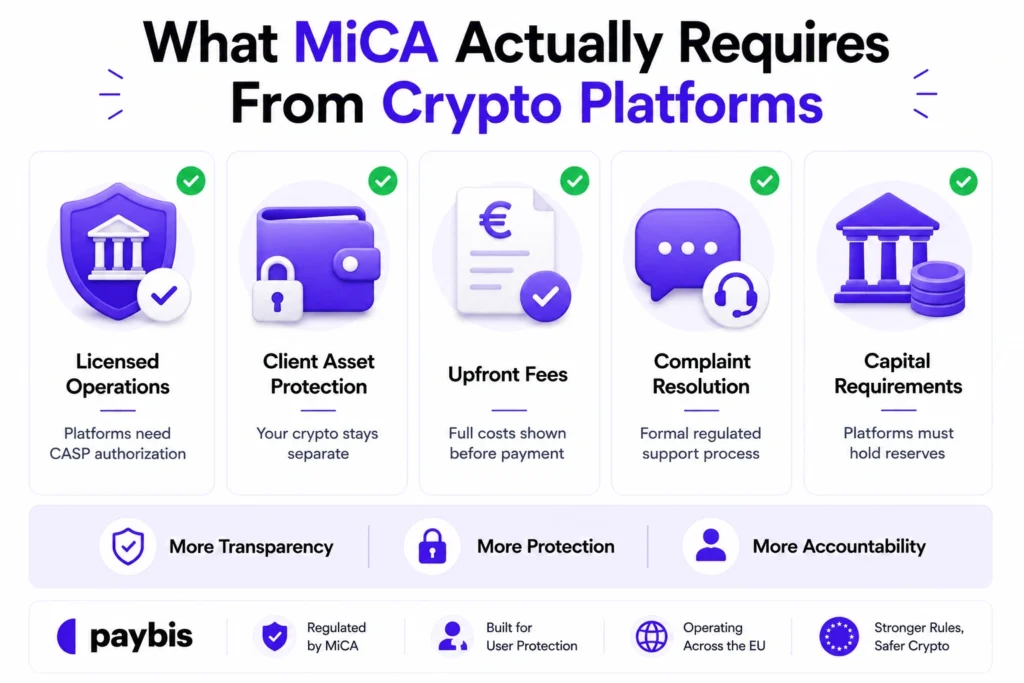

- Authorization before operating. A platform cannot serve EU users without first obtaining a CASP licence from a national financial regulator. Getting that licence requires a full review of the business, covering governance, capital, the people running it, and how the technology is secured. It is a financial services authorization, not a registration.

- Segregation of client assets. A licensed platform must hold your crypto separate from its own funds at all times. This is the rule FTX broke. Under MiCA, it is a non-negotiable condition of the licence. If a platform becomes insolvent, your assets are not treated as company property.

- Upfront fee disclosure. Before you confirm any transaction, the platform must show you the full cost. Hidden fees revealed only after the fact are prohibited.

- Complaint handling. Every licensed platform must have a formal process for receiving and resolving user complaints within defined timeframes. If something goes wrong, you have a regulated channel to use.

- Capital requirements. Platforms must hold minimum reserves appropriate to the scale of their operations. This prevents the scenario where a platform running on paper-thin margins collapses the moment markets move against it.

For a full breakdown of what platforms must comply with under the new rules, the crypto exchange regulations guide goes through each requirement in detail.

What Rights Do Crypto Users in Europe Have Now?

The practical effect of MiCA for anyone buying or holding crypto in Europe is a meaningful upgrade in user protections.

Your funds are legally required to be kept separate. Before MiCA, whether a platform segregated client assets was largely a matter of its own policy. Now it is a legal obligation enforced by the regulator that issued the platform’s licence.

You are entitled to see fees before you commit to a trade. Platforms that previously buried their costs in exchange rates or disclosed fees only at the point of completion can no longer do so legally.

If something goes wrong, you have a formal complaints route. That does not mean every complaint results in a refund, but it does mean the platform is required to take it seriously and respond within a regulated timeframe.

You also benefit from minimum capital requirements applying to the platform. A licensed exchange has to demonstrate it holds adequate reserves. That is not a guarantee against failure, but it does mean the platform has been assessed as financially viable before it was allowed to hold user funds.

All of this comes with one condition: the platform you are using needs to actually hold a valid CASP licence. None of these protections apply on an unlicensed platform, regardless of how professional it looks or how long it has been operating. To understand the full picture of what is legal and what is protected, the Is Crypto Legal in Europe guide covers it in detail.

How Do You Know If a Crypto Platform Is Compliant?

The quickest way is to check the public register of the relevant national financial regulator. Most EU national regulators publish the list of authorized CASPs on their websites. The check takes about a minute and tells you whether the platform has been through the authorization process.

Beyond the register check, there are signals worth looking for on the platform itself. A licensed CASP will display its regulatory status, the authority that issued the licence, and in many cases its licence number. Regulatory information buried in a footer, absent entirely, or pointing only to an AML registration rather than a full licence should prompt a closer look.

The distinction between an AML registration and a CASP licence matters significantly. A registration confirms the platform told a regulator it exists. A licence confirms the regulator reviewed the platform and decided it met the standard for handling your funds. The protections described above apply only to the latter.

If you are comparing platforms and one holds a MiCA CASP licence while another holds only an AML registration, you are comparing two different levels of regulatory oversight. They are not equivalent.

Does Crypto Regulation Vary Across European Countries?

On platform regulation, much less than it used to. MiCA created a single standard that applies across all 27 member states. Whether a platform is authorized in Latvia or the Netherlands or Germany, it operates under the same MiCA rules. The days when shopping around for the most lightly regulated EU jurisdiction gave platforms a meaningful competitive edge are over.

What still varies by country is how crypto is taxed. Germany exempts capital gains on crypto held for more than one year. Spain treats gains as taxable capital income on a progressive scale. The Netherlands takes a different approach through its wealth tax system. Each country applies its own framework, and the differences can be significant if you are making substantial gains.

Some national regulators have also moved faster than others on enforcement and authorization approvals. Latvia’s Bank of Latvia, Germany’s BaFin, and the Netherlands’ AFM have been among the more active. But the rules they are applying are identical. MiCA does not allow national regulators to add extra requirements or grant lighter treatment. The standard is the same everywhere.

What Is Coming Next in European Crypto Regulation?

MiCA was built with a review clause because the EU recognized that the technology moves faster than legislation. The European Commission is required to submit a review of the regulation’s scope to Parliament by December 2025, with particular focus on DeFi, NFTs, and any gaps that have emerged in the two years since the regulation passed.

DeFi is the area most likely to see follow-on legislation. The current MiCA framework largely excludes fully decentralized protocols with no identifiable legal entity behind them. Regulators globally have been watching the space carefully, and the EU’s follow-on framework is expected to address how obligations apply when there is no single operator to license.

NFTs are also under scrutiny. MiCA includes carve-outs for genuinely unique, non-fungible assets. In practice, many NFT collections function more like fungible assets, and the regulation includes provisions for regulators to reassess classification where that is the case.

For users, the most relevant near-term change is that more platforms are working through the CASP authorization process. The transition period for platforms that held pre-MiCA national registrations has a defined end date. By the time it closes, the population of authorized CASPs will be more clearly defined, and platforms still operating on legacy registrations will face a harder choice: get licensed or exit the EU market. The Paybis MiCA content hub covers new developments as they happen.

Is Paybis Regulated Under the New European Rules?

Paybis holds the MiCA CASP licence, issued by the Bank of Latvia in May 2026. It covers crypto-asset services across all 27 EU member states and the broader EEA through MiCA passporting. Alongside it sits the Payment Institution licence under PSD2, also issued by the Bank of Latvia. Both are full licences granted after a regulatory review.

The official announcement covers what the licences involved and what they mean in practice. On top of the EU authorizations, Paybis holds FCA authorization in the UK, FinCEN registration in the US, FINTRAC registration in Canada, and VASP registration in Poland.

Under MiCA’s requirements, client funds at Paybis are held separately from the company’s own assets. Fees are shown before you confirm a transaction. Live chat support is available around the clock.

Paybis has operated since 2014 and serves 6.9 million+ users across 190+ countries. You can buy Bitcoin and buy Ethereum through a platform operating under the EU’s full CASP authorization framework.

Bottom Line

European crypto regulation changed fundamentally in December 2024. MiCA replaced years of inconsistent national rules with a single framework that holds platforms to the same standard as regulated financial services firms. For users, the change means real protections around fund segregation, fee transparency, and complaint handling, but only on platforms that have actually obtained CASP authorization. The regulation did not make crypto in Europe safer by existing. It made it safer for users who choose licensed platforms over unlicensed ones.

FAQ

Does MiCA apply to me as a crypto user, or only to platforms?

MiCA’s rules apply primarily to platforms and token issuers, not to individual users. As someone buying, holding, or trading crypto in Europe, you are not directly regulated by MiCA. What the regulation does is set the rules for the platforms you use, which means your protections as a user depend on whether the platform you are using is actually authorized under MiCA. Your own crypto activity remains subject to national tax rules, which vary by country and are separate from MiCA entirely.

What happened to crypto platforms that were registered before MiCA?

Platforms that held national VASP or crypto registrations in EU member states before MiCA applied were given a transition period to upgrade to full CASP authorization. The length of that period varied by country. Once the transition window closes in a given jurisdiction, operating on a legacy registration becomes illegal. Many platforms are currently working through the CASP authorization process. Others have exited certain EU markets rather than meet the new requirements. If a platform you are using has not yet obtained CASP authorization, it is worth checking what their plans are.

Is my crypto safe if I use a MiCA-authorized platform?

A MiCA CASP licence provides meaningful protections. Licensed platforms are required to keep your assets separate from their own, maintain adequate capital reserves, and disclose fees upfront. Those are real safeguards. They are not a guarantee against every possible risk, including market volatility, security incidents, or unexpected business difficulties. A licence is a strong positive signal, and it means the platform has been reviewed and held to a regulated standard. It does not remove the need to choose carefully and keep track of what you hold and where.

Will MiCA affect which cryptocurrencies I can buy?

For the most part, no. Bitcoin, Ethereum, and the vast majority of cryptocurrencies are not affected by MiCA’s asset-side rules. The regulation focuses on token issuers and service providers, not on the assets themselves. Where MiCA has a practical effect is on new token offerings: any new crypto-asset offered to EU investors must now have a compliant white paper with defined disclosures. That may affect the availability of new or smaller tokens on regulated EU platforms, but it does not restrict access to established assets.

How is European crypto regulation different from the US approach?

Europe took a comprehensive, unified approach with MiCA, creating one framework that applies across all member states simultaneously. The US has taken a more fragmented path, with different agencies claiming jurisdiction over different asset types, state-level licensing requirements that vary dramatically, and ongoing regulatory and legislative debate about how crypto fits into existing securities law. For users, the practical difference is that a MiCA-authorized platform in Europe operates under a clear and consistent standard. In the US, the regulatory picture is still being defined.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info