Crypto Tax Canada 2026: What You Owe and How to Report It

- The CRA treats cryptocurrency as a commodity, not currency. That means tax applies every time you dispose of it

- 50% of your capital gain is added to your taxable income for the year

- Buying bitcoin and holding it are not taxable. Tax only applies when you dispose of it

- Crypto-to-crypto trades are taxable. Swapping Bitcoin for Ethereum is treated the same as selling Bitcoin for cash

- Not reporting crypto gains to the CRA is not a grey area. The agency has been actively auditing crypto holders since 2020

Canada has some of the clearest crypto tax rules in the world. The CRA made its position official in 2013 and has been building on it ever since. The framework is not complicated, but most first-time crypto holders get at least one thing wrong.

Usually, it’s this: they think tax only applies when they cash out to Canadian dollars. It doesn’t.

This guide covers every taxable event, how the CRA calculates what you owe, and exactly how to report it on your return.

Before we get into it, if you’re ready to buy crypto in Canada today, Paybis supports credit and debit card purchases across 90+ cryptocurrencies.

Table of contents

- Does Canada tax cryptocurrency?

- What crypto transactions are taxable in Canada?

- What crypto transactions are not taxable?

- How does the CRA calculate your crypto gain?

- Capital gains or business income: how does the CRA decide?

- How do you report crypto on your Canadian tax return?

- What happens if you don’t report crypto to the CRA?

- Bottom Line

Does Canada tax cryptocurrency?

Yes. The CRA treats crypto as a commodity under the Income Tax Act. Every time you sell it, trade it, or spend it, that’s a taxable event.

Canada has taxed crypto since at least 2013, when the CRA first published guidance on the subject. The framework hasn’t changed at its core: crypto is property, not currency. That distinction matters because currency transactions aren’t taxed the same way property transactions are.

The moment you sell, trade, or spend crypto, expect a tax obligation. The only question is whether it’s treated as a capital gain or business income. That classification is what determines how much of the profit actually gets taxed.

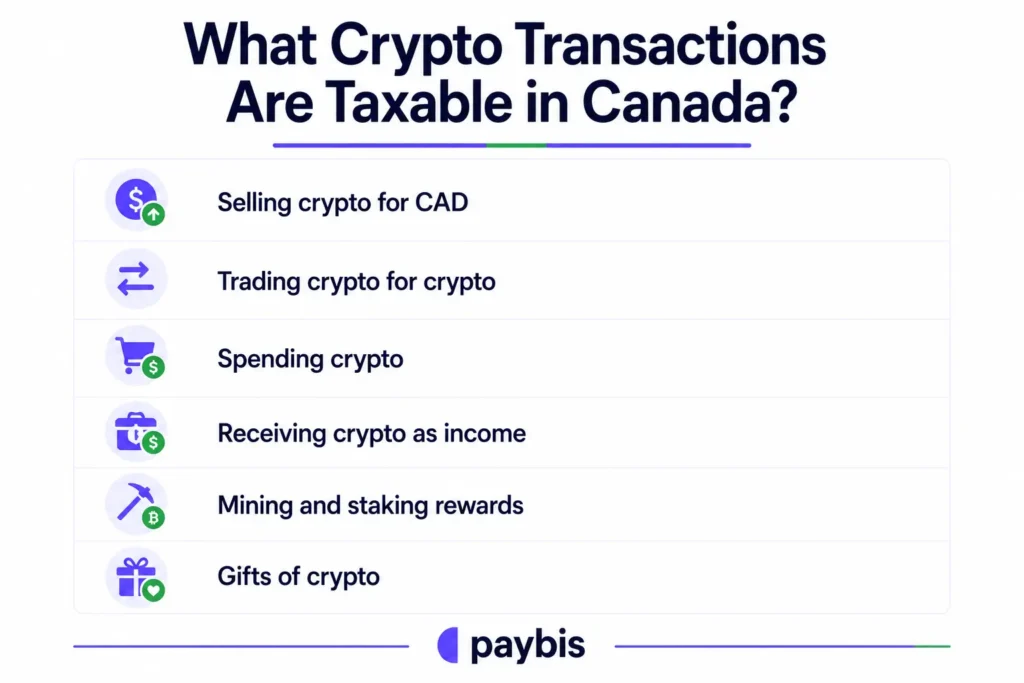

What crypto transactions are taxable in Canada?

Any disposal of crypto creates a taxable event. Selling for CAD is the obvious one, but so is trading one crypto for another, spending it, or receiving it as payment for work.

Here’s a breakdown of what triggers tax:

- Selling crypto for CAD: The most obvious one. You sold Bitcoin for $10,000 and originally paid $6,000. The $4,000 difference is your capital gain.

- Trading crypto for crypto: Swapping ETH for SOL counts as disposing of ETH at its current market value. The CRA sees this as the same as a sale.

- Spending crypto: Used Bitcoin to pay for a service? The CRA treats that as selling Bitcoin at the market value on the day of the transaction.

- Receiving crypto as income: If someone pays you in crypto for work or services, that amount is taxable as business or employment income at the fair market value on the day you received it.

- Staking and mining rewards: Generally treated as income when received, based on market value at the time. If you later sell those coins, any additional gain is also taxable.

- Gifts of crypto: Giving crypto away is treated as a disposal at fair market value on the day of the gift.

What crypto transactions are not taxable?

Buying crypto and holding it are not taxable. The tax event happens at disposal, not acquisition. Moving crypto between wallets you own falls into the same category.

Here’s what doesn’t trigger a tax event:

- Buying crypto with CAD: No tax owed at purchase. The price you pay becomes your cost base for future calculations.

- Holding: Sitting on crypto for months or years with no transactions creates no tax liability until you sell or trade.

- Transferring between your own wallets: Moving Bitcoin from one wallet to another you control is not a disposal. Keep records of the transfer anyway, since the CRA may ask you to prove the wallets belong to you.

How does the CRA calculate your crypto gain?

Your taxable gain equals the proceeds minus your adjusted cost base (ACB). For capital gains, 50% of that amount is added to your taxable income.

The ACB is the average cost of all units of a given cryptocurrency you hold, updated every time you buy more. This matters because you can’t cherry-pick which coins you “sold” to minimise your gain. The CRA uses the average cost method across your entire holding of that coin.

Here’s a simple example:

- You buy 1 BTC for $40,000 in January

- You buy 1 more BTC for $60,000 in March

- Your ACB is now $50,000 per BTC (average of the two)

- You sell 1 BTC in June for $70,000

- Your capital gain is $70,000 minus $50,000 = $20,000

- 50% of $20,000 = $10,000 is added to your taxable income

That $10,000 gets taxed at your marginal rate, not a flat crypto rate. The higher your total income that year, the higher the rate.

Capital gains or business income: how does the CRA decide?

If you trade frequently, with intent to profit, the CRA may classify your activity as business income. In that case, 100% of the gain is taxable, not 50%.

The distinction matters significantly. Capital gains treatment means only half your profit is taxed. Business income treatment means all of it is.

The CRA looks at several factors to decide which applies:

- Frequency: Dozens of trades per week point toward business activity

- Intent: Did you buy to hold long-term, or to flip quickly for profit?

- Time spent: Are you actively managing positions as a primary or secondary occupation?

- Knowledge: Professional-level market knowledge and tooling weigh toward business income

- Financing: Using leverage or borrowed money to buy crypto is a business income signal

Casual investors who buy and occasionally sell are almost always in capital gains territory. Active day traders typically are not. If you’re unsure, a Canadian tax professional is worth consulting before you file.

How do you report crypto on your Canadian tax return?

Capital gains go on Schedule 3 of your T1 General return. Business income goes on Form T2125. You need records of every transaction to complete either form accurately.

For capital gains, Schedule 3 asks for:

- Description of the property (e.g., Bitcoin)

- Date of acquisition

- Proceeds of disposition

- Adjusted cost base

- Outlays and expenses (transaction fees)

- Net gain or loss

For each crypto you traded during the year, you’ll need to calculate your ACB across every purchase, then apply it to each sale. With dozens of transactions, this adds up fast. Most Canadians use crypto tax software like Koinly or CoinTracker to generate the Schedule 3 data automatically by connecting their wallets and exchange accounts.

The CRA does not require you to submit transaction logs with your return, but you are legally required to keep them for six years in case of an audit.

What happens if you don’t report crypto to the CRA?

The CRA actively pursues unreported crypto income. Gross negligence penalties alone can reach 50% of the tax owing. Criminal prosecution is also on the table for serious cases.

The enforcement picture changed significantly in 2026. The Crypto-Asset Reporting Framework (CARF) took effect on January 1, 2026. Under CARF, Canadian exchanges are now required to collect and report user transaction data directly to the CRA, with the first reports expected in 2027. Automatic data sharing is coming, not just reactive requests during audits.

That’s on top of a dedicated 35-person CRA crypto audit team that has already recovered over $100 million in unpaid tax across three years. Courts have granted formal data requests against Canadian exchanges on multiple occasions, including against Dapper Labs.

The most common mistake is not deliberate evasion but genuine misunderstanding. People assume crypto is untraceable or that small amounts don’t count. Neither is true. The CRA treats a $500 crypto gain the same way it treats a $50,000 one: it’s taxable income and needs to be declared.

Voluntary disclosure is available if you’ve missed reporting in previous years. Coming forward before the CRA contacts you generally results in reduced penalties.

Bottom Line

Canada’s crypto tax framework is clear. The CRA taxes disposals, not holdings. Capital gains get 50% inclusion, frequent trading can push you into business income territory, and 2026 is the year the enforcement infrastructure got meaningfully stronger with CARF.

The admin side is real, especially if you’ve been active across multiple exchanges. Crypto tax software handles most of the calculation work. But the records still need to exist, and the declaration still needs to be made.

If you’re buying crypto and want to start on the right foot, Paybis lets you buy Bitcoin and 90+ other cryptocurrencies with a credit or debit card. Your transaction history exports cleanly, which makes filing considerably less painful.

This article is for educational purposes only and does not constitute tax or financial advice. Canadian tax rules can change. Consult a qualified Canadian tax professional for advice specific to your situation.

FAQ

Do I owe tax on crypto I haven't sold yet?

No. Unrealised gains are not taxable in Canada. You only owe tax once you dispose of the crypto. Holding at a profit, for a week or for three years, creates no immediate tax obligation.

Is crypto-to-crypto trading taxable in Canada?

Yes. Every crypto-to-crypto trade is treated as a disposal. When you swap Bitcoin for Ethereum, the CRA treats that as selling your Bitcoin at its current market value in CAD. Any gain over your ACB for that Bitcoin is taxable in the year the trade occurred.

What records do I need to keep for the CRA?

For every transaction: the date, the CAD value at the time, and the purpose. Exchange statements and wallet history exports are the most practical way to maintain this. You’re required to keep records for six years.

Are staking rewards taxed in Canada?

Yes, generally as income. When you receive staking rewards, the CRA treats them as income at their fair market value on the day you received them. If you later sell those tokens at a higher price, the additional gain is also taxable as a capital gain.

Can the CRA see my crypto transactions?

Yes, and their visibility just got significantly wider. As of January 1, 2026, Canadian exchanges are required under CARF to collect and report user transaction data directly to the CRA, with the first reports going out in 2027. On top of that, blockchain transactions are publicly visible by design. Using a foreign exchange doesn’t insulate you either. CARF is being adopted internationally, and cross-border data sharing is part of the framework. Assuming crypto is invisible to tax authorities is one of the more costly assumptions a Canadian investor can make.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info