Why Crypto Users Switch Platforms (And Never Tell You Why)

- Fee surprises are interpreted as dishonesty. Users can tolerate high fees when quoted clearly upfront, but unexpected ones end the relationship permanently

- A transaction hash is not proof of delivery. Fund Movers need something they can show another person to confirm a real-world obligation was met

- Vague status updates (“pending,” “checking”) escalate into fraud accusations faster than actual delays do

- The sequence of KYC matters as much as the KYC itself. Taking payment before verification is complete is experienced as predatory

- Traders use platforms as infrastructure, not destinations. One bad corridor outcome causes rerouting, not just dissatisfaction

- One successful transfer does not build deep trust, but one bad transfer can wipe out multiple successful ones

Let’s say someone just sent $800 to cover a family member’s rent abroad. The platform said up to 10 minutes. Two hours later, the status still reads “checking” with no timeline, no update, and nobody useful on support. At that point, they don’t care about the platform’s features or its fee structure. They are thinking about whether they just lost $800 to a site they will never use again, and tell everyone they know to avoid it.

That is the world Paybis set out to understand. We have interviewed our users across two segments (Fund Movers and Traders) with one goal: to map exactly where trust forms, where it breaks, and how fast the damage spreads once it does. Here is what we have found.

Who Did We Interview

Table of contents

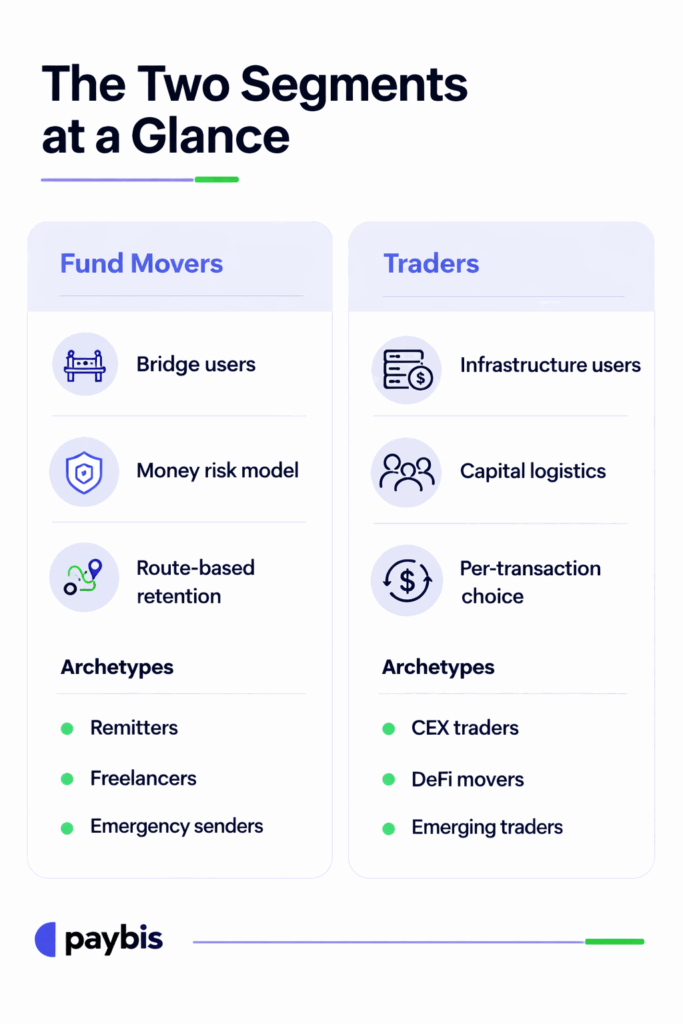

Fund Movers

Fund Movers are not here to explore a product or try new features. They found a route that works, and they want it to behave the same way every single time. Because the transfers they are making carry real stakes:

- Remitters sending money home

- Freelancers getting paid across borders

- People covering urgent bills for family members who cannot wait another day.

Many of them operate in places where local banking infrastructure is too slow or too complicated to be useful, which is what pushed them toward crypto rails in the first place.

The research identified something important about how this segment processes every interaction with a platform. They run a money risk model, reading the copy on a button, the wording of a verification request, and the tone of a support reply as evidence about whether they are about to lose access to their funds. That is why frictions that would barely register for other users can produce reactions that look disproportionate from the outside. From the inside, they are just managing real risk.

Traders

For Traders, a platform like Paybis is capital logistics. It’s the fastest practical way to move money into crypto using the rails that work in their geography, so they can reach the venue where real trading happens. Three archetypes showed up clearly in the research:

- Active CEX traders fund positions quickly and move assets to Binance, Bybit, or OKX for execution, which means they need to buy Bitcoin or another asset fast, with no friction on entry

- DeFi movers pull assets into self-custodial wallets and operate across chains and protocols

- Emerging traders start small, form their entire platform judgment from the first one or two outcomes, and reach for the word “scam” faster than any other group when something goes wrong.

Across all three, the choice is per-transaction. There is no brand loyalty in this segment, only the practical question of whether a specific route works right now for this amount with this method.

The Six Things Users Are Actually Trying to Do

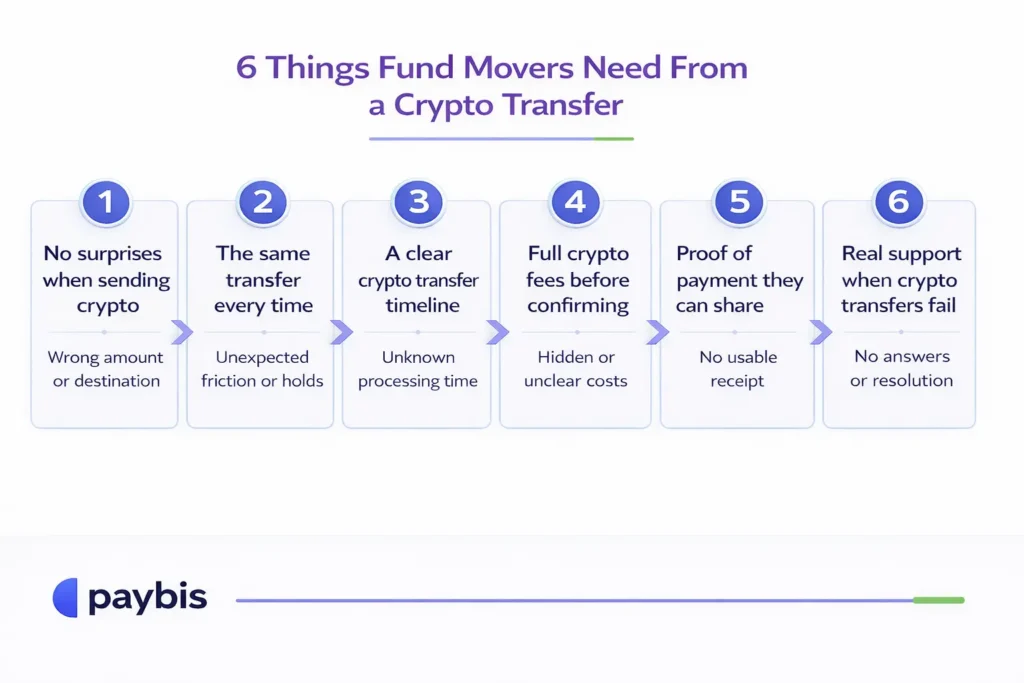

Strip away the product complexity, and both segments are trying to accomplish the same six things. Each one carries a specific expectation, and each one has a documented way it breaks.

1. Get the money there without surprises.

Fund Movers: The amount they sent needs to arrive in full, at the right place, with nothing missing and no mystery deductions. This sounds obvious, but it’s also the thing that breaks most often.

Traders: Same need, different version. The price they saw when they hit confirm needs to be the price they actually got. Slippage and unexpected execution gaps are their version of the missing money problem.

2. Have it work the same way next time.

Fund Movers: They’re not loyal to the platform, but to the route. If they did the exact same transfer last month and this month something different happens (like a hold, a new document request, a limit they didn’t know existed), the route is broken. Doesn’t matter if the platform is technically working fine.

Traders: Same psychology, different trigger. The same asset, same size, same market conditions should produce a roughly comparable result. When fills or fees behave differently for no clear reason, trust goes with it.

3. Know exactly how long it will take.

Fund Movers: A transfer that takes four hours and says it will take four hours is fine. A transfer that says ten minutes and takes three hours, though, is a lie, as far as the user is concerned. The research found people escalating to fraud claims specifically because nobody told them what was actually happening.

Traders: For them, timing uncertainty is both just frustrating and expensive. An open order during a price move isn’t a neutral experience. Every minute without clarity has a potential cost attached to it.

4. See the full cost before confirming.

Fund Movers: Platform fee, processor fee, network fee, and spread, all of it needs to be visible before they press the button. High fees are a complaint, but fee shock feels like a betrayal. People can absorb the first one, but they leave loudly over the second.

Traders: They’re reading the same information, just with more line items. Spread, commission, funding rate, conversion fees; they want all of it visible before they enter a position. Surprises at the confirmation stage kill the trade before it starts.

5. Have proof of the transfer, not just the transaction.

Fund Movers: They need a receipt. Date, amount, sender, recipient, or status, something they can forward to the person waiting on the other end. A transaction hash means nothing to a family member asking if the money arrived. The transfer isn’t done until the recipient confirms it, and the receipt has to help make that case.

Traders: They need a clean trade record. Something they can use to check their positions, sort out taxes, or push back on a fill that doesn’t look right. The confirmation is a part of how they manage their portfolio.

6. Get a real person to talk to when something goes wrong.

Fund Movers: They need to know what’s happening, what comes next, and that someone is actually on it. “We’re waiting on the payment provider” tells them nothing. There’s usually someone on the other end waiting for that money, which means vague answers create two anxious people instead of one.

Traders: A stuck position or a frozen withdrawal is costing them money in real time. They need the same things: a timeline, a next step, a human. The longer the support takes to give them that, the more expensive the silence gets.

Trust Does Not Work the Way Platforms Think It Does

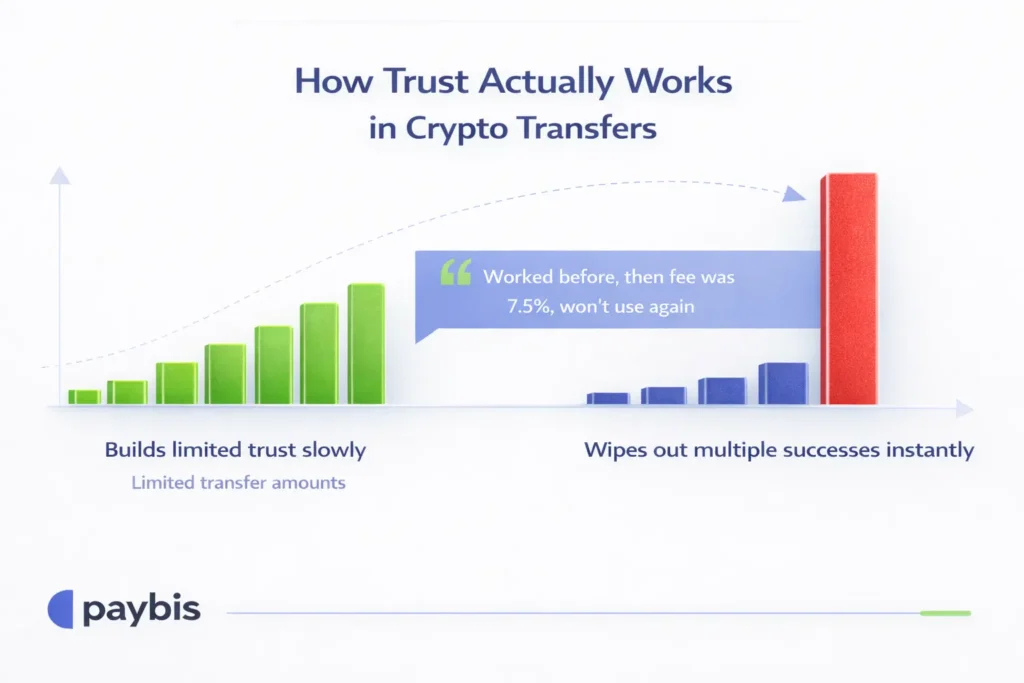

Every successful transfer does not add a brick to the trust wall. It adds permission to try again, which is a much smaller thing. The interviews captured this in real user language: “used it several times, but I keep amounts small.” That is a permanently suspicious customer who never had a bad experience bad enough to leave, and those two things are very different.

One bad transfer, though, wipes out several good ones. The research calls this the trust debt curve, and it is asymmetric in a way that should reshape how platforms think about retention. The goal is not to accumulate successful transactions. The goal is to eliminate the single bad outcome that erases them.

What this segment cannot tolerate is variance. The route that ran at 3% last month and now runs at 7.5% is not a pricing change. It is a betrayal. A platform that is fast sometimes and stuck other times destroys the predictability that Fund Movers depend on to coordinate real-world obligations. Users do not come back to platforms, either. They come back to routes: the same method, the same corridor, the same asset, and network. When any element of that combination shifts without explanation, the route feels broken regardless of what is actually happening on the backend.

The Four Levels of Losing a Crypto User

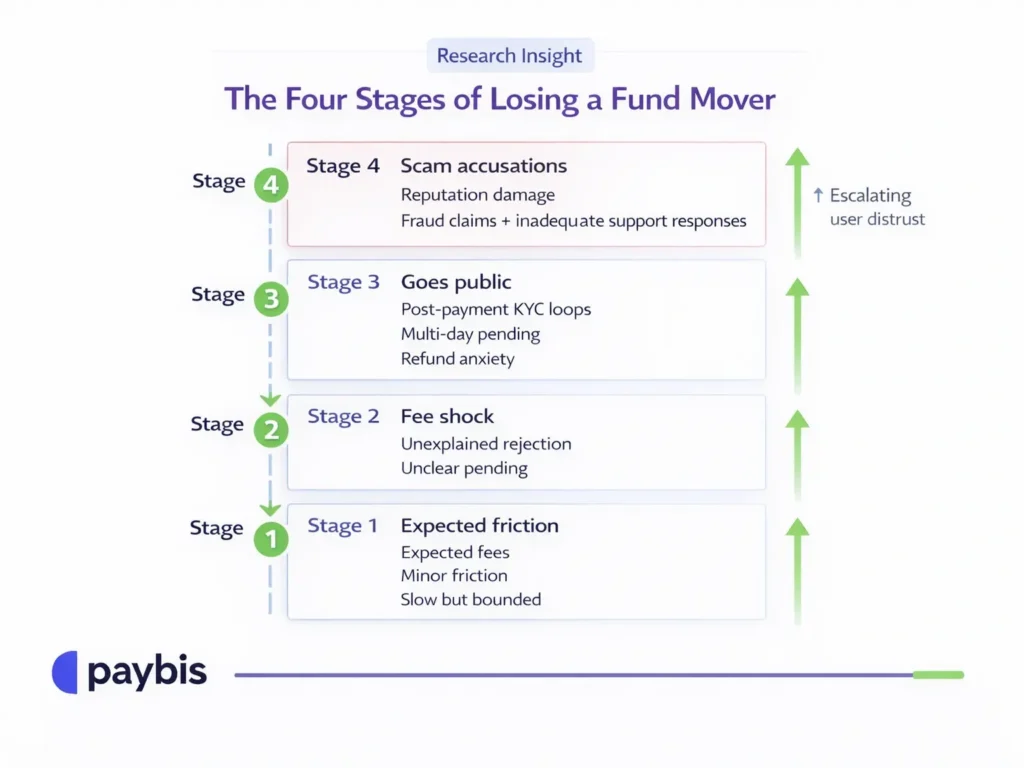

The research maps failure modes onto a severity scale, and understanding where a situation sits tells you how much damage is already being done.

- Low severity covers expected fees, minor friction that does not block completion, and processing that is slow but matches what the platform promised. Users grumble. They come back.

- Medium severity (likely churn) includes fee shock, discounts that failed to apply, extended pending that was resolved but with no clarity along the way, and rejections with no usable explanation. Users at this level often leave without saying anything publicly.

- High severity (public narrative risk) is triggered by post-payment verification loops, multi-day pending with vague support responses, perceived non-delivery, and refund timelines that feel arbitrary. At this level, users start talking: community posts, negative reviews, and direct warnings to people in their network.

- The highest severity (fraud accusation territory) occurs when unauthorized transaction claims or scam victim situations combine with dismissive support or “nothing we can do” responses. The research documents a specific escalation pattern at this level: users stop distinguishing between “platform used by scammers” and “platform complicit in the scam” when resolution feels stalled or absent. The language in the interviews here includes “thieves,” “scam site,” and “participating in crimes.” Recovery from this point is rare.

The Order of Events Is a Product Decision

One of the most specific findings in the report comes down to sequence, and it has a direct fix.

The “charged before KYC clarity” pattern produces more scam language in the dataset than almost any other failure mode. Payment is captured, KYC then intensifies or becomes open-ended, the transaction gets rejected, and the refund is delayed. Users describe this as a trap, and the verbatim from interviews is direct: “Do your KYC before charging people. Simple.” The same verification controls feel completely legitimate before payment and predatory after it. The sequence is the product decision, and it is a reversible one.

Small test transfers carry a version of the same risk. Many Fund Movers trial a platform with a tiny amount before committing to larger ones. If that small test triggers heavy verification or a hold, the story they construct is disproportionate to the amount: “If they do this for €10, what happens at €1,000?” That story poisons the route before it ever scales to the transactions that actually matter.

A Hash Is Not a Receipt

Users in both segments describe their transfers in payment language. “Sending money.” “Paying a bill.” “Paying someone abroad.” Even users who fully understand the crypto mechanics frame it this way, and that framing creates a specific expectation about what proof looks like: a receipt with a date, an amount, a sender, a recipient, and a status they can forward to someone else.

Because the definition of delivery in this segment is social. It is not “transaction submitted” or “on-chain broadcast.” It is the moment the recipient says “I got it,” and until that happens, the transfer is unresolved, regardless of what any block explorer shows. The traceability request is also often about third-party accountability, built for the recipient, the family member, the boss, or the bank. A hash does not win an argument with another person, but a clear shareable receipt does, and the platforms that generate that kind of evidence during the uncertainty window are the ones positioned to own this segment long-term.

Support Is Not a Department; It Is Part of the Product

Users judge support in failure states on decisiveness. A credible timeline, a clear next state, and evidence that someone can act on their behalf. Repetition, templated replies, and “we’re waiting on the payment provider” land as helplessness, and in a context where someone’s money is stuck, helplessness reads as untrustworthiness. The interviews document rapid escalation from frustration to fraud accusations, specifically in the cases where support could not offer a resolution path.

For active CEX traders, a hold during market volatility carries additional weight. It is a direct strategy damage: a missed entry, an exposure that cannot be reduced, a position that cannot be managed because the capital is stuck. Refund delays in this group get benchmarked against the fastest consumer refund experience users know, with direct comparisons to Amazon returns appearing across the interviews. Financial industry settlement norms are not relevant to how fairness is experienced here.

Bottom Line

Thirty-one interviews, two segments, and one consistent finding across all of them.

The platforms that retain Fund Movers and Traders are the ones that execute predictably, price transparently, communicate with clear timelines, and treat support as a functional part of the product. Neither segment is asking for innovation. Both are asking for consistency, and both will route around any platform that cannot provide it without announcing the decision to anyone except the people they warn away from the same route.

The failure modes in this research are preventable. Most of them are communication and sequencing problems, and the cost of not solving them compounds through the networks these users operate in. Because routes that break get talked about just as much as routes that work.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info