Crypto Tax UK 2026: HMRC Rules, Rates, and How to Report

- HMRC treats crypto as property. Capital Gains Tax applies when you sell, trade, or spend it

- CGT rates changed on 30 October 2024: basic rate taxpayers pay 18%, higher and additional rate taxpayers pay 24%

- The annual CGT allowance is £3,000 for both the 2025/26 and 2026/27 tax years

- Crypto-to-crypto swaps are taxable in the UK. Swapping Bitcoin for Ethereum is treated as selling Bitcoin at its GBP value on the day

- From 1 January 2026, UK exchanges must report all user transaction data to HMRC under CARF. The first reports cover the full 2026 calendar year

Most people who buy crypto in the UK assume tax only applies when they cash out to pounds. That assumption is expensive.

HMRC has been clear since 2018: crypto is a capital asset, not a currency. Every time you dispose of it, a potential tax liability arises. That includes swaps, spending, and gifts. Holding does not trigger anything, but selling does.

The tax rules have not changed dramatically in 2026, but the enforcement picture has. CARF came into force on 1 January 2026, which means UK exchanges now automatically send user transaction data to HMRC. The days of crypto operating in an information blind spot are over.

This guide covers every taxable event, the current rates, how HMRC calculates what you owe, and exactly how to report it.

Before we get into it, if you’re buying crypto in the UK, Paybis is FCA-registered and supports buying Bitcoin, Ethereum, USDT, and 90+ other cryptocurrencies with a credit or debit card, PayPal or bank account.

Does HMRC tax cryptocurrency?

Yes. HMRC treats cryptocurrency as a capital asset, not a currency. This means Capital Gains Tax applies to profits from disposals, and Income Tax applies to crypto earned through mining, staking, and employment.

The keyword is disposal. A disposal happens when you sell crypto for GBP, trade one cryptocurrency for another, spend crypto on goods or services, or give it away as a gift. Each of these creates a potential tax event in the year it occurs.

Buying crypto and sitting on it creates no liability. The clock only starts ticking when you do something with it.

What are the UK crypto tax rates for 2026?

CGT rates on crypto changed on 30 October 2024. Basic rate taxpayers now pay 18% and higher and additional rate taxpayers pay 24% on gains above the annual allowance.

The annual CGT allowance is £3,000 for both 2025/26 and 2026/27. Gains below that threshold in a given tax year are not taxed. If you made £2,800 in crypto gains and nothing else, you owe nothing.

Here’s how the rates apply based on your total income:

| Taxpayer | CGT Rate on Crypto |

|---|---|

| Basic rate (income up to £50,270) | 18% |

| Higher rate (income £50,271 to £125,140) | 24% |

| Additional rate (income above £125,140) | 24% |

One thing worth knowing: if your gain pushes your total income over the basic rate threshold, the portion of the gain above the threshold is taxed at 24%, not 18%. The two rates can both apply within the same tax year.

For crypto earned as income (staking rewards, mining, payment for work), Income Tax applies instead. That’s taxed at your marginal rate, between 0% and 45%, depending on your total annual income.

What crypto transactions are taxable in the UK?

Any disposal of crypto triggers a potential taxable event. That covers selling for GBP, swapping one crypto for another, spending crypto, and receiving it as income.

Here’s what counts as a taxable disposal:

- Selling crypto for GBP: The most straightforward case. You sold Bitcoin at a higher price than you paid. The difference is your gain.

- Trading one crypto for another: Swapping ETH for SOL is treated as selling ETH at its GBP market value on the day of the trade. Any gain over your ETH cost basis is taxable.

- Spending crypto: Using Bitcoin to pay for a laptop counts as a disposal. HMRC calculates the GBP value at the time of the purchase and compares it to your cost basis.

- Gifting crypto: Giving crypto to anyone other than a spouse or civil partner is treated as a disposal at market value on the day of the gift.

- Receiving crypto as payment for work: Taxable as Income Tax at the GBP value on the day you received it.

- Staking and mining rewards: Generally treated as miscellaneous income when received, at the GBP value on the day of receipt. If you later sell those tokens at a profit, CGT applies to any additional gain.

What crypto transactions are not taxable?

Buying crypto, holding it, and transferring it between wallets you own are not taxable. The tax event happens at disposal, not acquisition.

Three things that do not trigger a liability:

- Buying crypto with GBP: The price you pay becomes your cost basis for future calculations. No tax at the point of purchase.

- Holding: Sitting on crypto for months or years with no transactions creates no obligation until you sell or trade.

- Transferring between your own wallets: Moving Bitcoin from one personal wallet to another is not a disposal. Keep records of these transfers anyway, as HMRC may ask you to demonstrate the wallets are yours.

One nuance worth knowing: transfer fees paid in crypto (rather than GBP) may themselves count as a disposal in HMRC’s view. It is a small amount in most cases, but it is worth tracking.

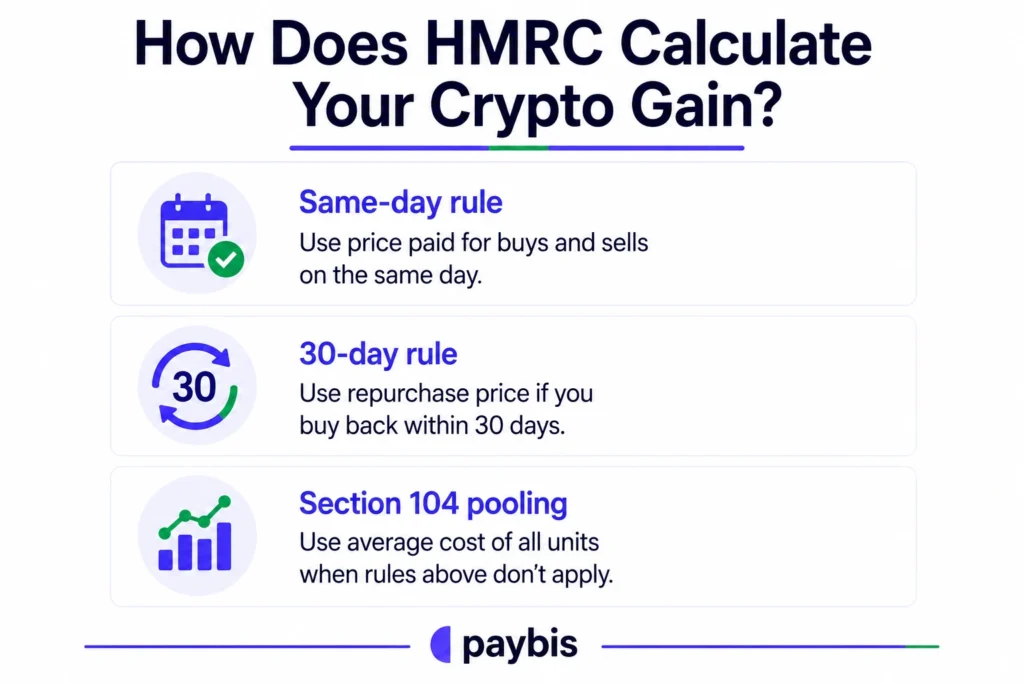

How does HMRC calculate your crypto gain?

HMRC requires you to use three cost basis rules in a specific order: the same-day rule, the 30-day bed and breakfasting rule, and Section 104 pooling. You cannot choose the method that produces the lowest gain.

The rules work in sequence:

- Same-day rule: If you buy and sell the same cryptocurrency on the same day, the cost basis for the sale is the price paid on that day.

- 30-day rule: If you sell a cryptocurrency and buy it back within 30 days, the cost basis uses the repurchase price rather than the original purchase price. This prevents bed and breakfasting, where someone sells to crystallise a gain or loss and immediately buys back.

- Section 104 pooling: When neither of the above rules applies, HMRC uses a pool. You calculate the average cost of all units of a given cryptocurrency you have ever bought, and that average becomes the cost basis for each disposal. Every new purchase updates the pool average.

Here’s a simple example using Section 104:

- You buy 1 BTC for £30,000 in January

- You buy 1 more BTC for £50,000 in March

- Your pool average is now £40,000 per BTC

- You sell 1 BTC in June for £60,000

- Your gain is £60,000 minus £40,000 = £20,000

- After the £3,000 allowance, £17,000 is taxable at your CGT rate

You cannot cherry-pick the cheapest Bitcoin you hold to minimise the gain. The pool average applies across your entire holding of that coin.

How do you report crypto on your UK tax return?

Crypto gains go on the Capital Gains Summary (SA108) in your Self Assessment return. Crypto income goes on the SA100. The online filing deadline is 31 January following the end of the tax year.

The UK tax year runs from 6 April to 5 April the following year. For gains made between 6 April 2025 and 5 April 2026, you report them by 31 January 2027.

You must file a Self Assessment return if:

- Your total crypto gains exceed the £3,000 allowance

- Your total disposals (gross proceeds) exceed £50,000, even if your actual gain is below the allowance

- You received crypto as income

For each disposal, you need: the date, the GBP proceeds, your cost basis, any allowable fees, and the resulting gain or loss. With many transactions, crypto tax software like Koinly or CoinTracker pulls this data from exchange accounts and generates HMRC-ready reports.

HMRC also has a voluntary disclosure service for crypto. If you have unreported gains from previous years, coming forward before HMRC contacts you generally results in significantly lower penalties.

Can HMRC see your crypto transactions?

Yes, and their visibility expanded significantly from 1 January 2026. Under CARF, all UK crypto exchanges are now legally required to collect and report user transaction data to HMRC automatically.

CARF (the Crypto-Asset Reporting Framework) took effect on 1 January 2026. Every regulated UK exchange must report customer names, National Insurance numbers, addresses, transaction volumes, and GBP values. First reports cover the entire 2026 calendar year and are due to HMRC between January and May 2027.

Around 50 UK exchanges are currently in scope, with more expected to fall within the framework as the new FCA licensing regime comes into force in October 2027.

HMRC also already has data from earlier periods. Between 2024 and 2025, HMRC sent approximately 65,000 nudge letters to crypto holders it suspected of non-compliance. Blockchain transactions are also publicly visible by design, and HMRC has the tools to trace wallet activity.

What happens if you don’t report crypto to HMRC?

HMRC can assess up to 20 years of historical gains for deliberate non-disclosure. Penalties reach up to 200% of the tax owed. Criminal prosecution is also possible in serious cases.

The most common situation is not deliberate evasion. Most people who fail to report crypto gains simply didn’t know the rules applied to crypto-to-crypto trades or small amounts. HMRC’s position is the same regardless: the obligation exists, and ignorance of the rules is not a defence.

For penalties, HMRC uses a sliding scale based on whether the failure was careless, deliberate, or deliberate and concealed:

- Careless: 0% to 30% of tax owed

- Deliberate: 20% to 70% of tax owed

- Deliberate and concealed: 30% to 200% of tax owed

Voluntary disclosure reduces penalties at every level. If HMRC contacts you first, you lose that reduction.

Bottom Line

HMRC’s position on crypto has been consistent for years. It is a capital asset, disposals are taxable, and the rates since October 2024 are 18% and 24%, depending on your income bracket. CARF means the information gap that some holders relied on is closing fast.

The admin side is manageable with the right tools. Crypto tax software handles most of the calculation work. But the records need to exist, the Self Assessment needs to be filed, and losses need to be registered within four years to count.

FAQ

Is crypto-to-crypto trading taxable in the UK?

Yes. Every swap between cryptocurrencies is treated as a disposal by HMRC. When you trade Bitcoin for Ethereum, HMRC calculates the GBP value of the Bitcoin at the moment of the trade and compares it to your cost basis. Any gain is subject to CGT in that tax year. This is one of the most commonly missed obligations among UK crypto holders.

Do I pay tax on staking rewards in the UK?

Yes, at the point of receipt. HMRC treats staking rewards as miscellaneous income, taxable at your marginal Income Tax rate based on the GBP value when you received them. If you later sell those tokens at a profit, CGT applies to any gain above the value at the time you received them.

What records do I need to keep for HMRC?

For every transaction: the date, the cryptocurrency involved, the amount, the GBP value at the time, and the purpose. Exchange statements and wallet history exports are the most practical source. HMRC requires you to keep records for at least 22 months after the end of the tax year for Self Assessment returns, though most advisers recommend keeping them indefinitely given the 20-year assessment window for deliberate non-disclosure.

Can I offset crypto losses against gains?

Yes. If you sell crypto at a loss, that loss can be offset against gains in the same tax year, reducing your total taxable gain. Losses can also be carried forward indefinitely to offset future gains. You must register the loss with HMRC within four years of the end of the tax year in which it occurred, or it is forfeit.

Is transferring crypto between my own wallets taxable?

No. Moving crypto between wallets you own is not a disposal. The cost basis carries over unchanged. Keep records of the transfer to demonstrate the wallets belong to you if HMRC ever asks.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info