Why Bitcoin Taxes and Regulations Are A Good Thing

Disclaimer: The information provided in this is only for educational purposes and does not constitute financial advice. The information is also updated only up to the article’s publication date. Some of the information may become outdated in the future. Consult a financial professional before making any investment decisions.

In 2008, Satoshi Nakamoto published the Bitcoin whitepaper. This document came at a time when the world was facing a major financial crisis triggered by some of the biggest banks. As people lost their homes, their trust in the banking system also diminished.

The launch of Bitcoin was meant to bring a new, decentralized financial system. A system that Satoshi envisioned would protect consumers from the whims and fancies of traditional financial institutions.

You can read more about this in the History of Bitcoin.

So, decades after the introduction of Bitcoin to the world – has Nakamoto’s goal been achieved?

Admittedly, there have been positive changes, and Bitcoin is continuing to gain traction as a global currency.

However, not everything has unfolded the way the creator intended. Bitcoin was supposed to be a censor-proof digital currency, free from any third-party control, whether that be by government or financial institutions.

The crypto landscape, as it stands today, suggests that regulation and taxation could help bring Nakamoto’s vision closer to reality. Let’s dive deeper into this.

Table of contents

- What’s the Big Deal with Regulations, Bitcoin, and Taxes?

- Why Bitcoin Shouldn’t Be the Wild, Wild West

- Better regulations lead to more adoption

- Who Defines the Regulations?

- Crypto Companies Already Know How to Toe the Line

- How Do Cryptocurrency Taxes Impact the Common Man?

- How to File Bitcoin Taxes?

- What Happens if You Don’t Report Cryptocurrency on Taxes?

- Where Can You Find The Best Crypto Tax Software?

- How to Not Pay Taxes on Bitcoin: Reduce Taxable Income

- Bitcoin Mining Taxes: Capital Gains Tax or Income Tax?

- Crypto Tax Rates Across All Countries

- Conclusion

- Keep Up with All-Things Crypto on Paybis

What’s the Big Deal with Regulations, Bitcoin, and Taxes?

Bitcoin and taxes are seldom used in a sentence together because several Bitcoin maximalists hold a negative opinion towards taxation. However, to stay compliant within a jurisdiction, honest tax reporting is crucial.

Bitcoin’s place as the top cryptocurrency has prevailed over the years. Many still think of it as the digital replacement of traditional currencies.

Increased usage and network maturity are usually cited as the top reasons for Bitcoin’s growth so far. However, this doesn’t mean it hasn’t shown drawbacks.

To start, global governments, with the exception of a few countries, have shown an open distrust towards Bitcoin. A primary reason for this has been a lack of regulatory clarity.

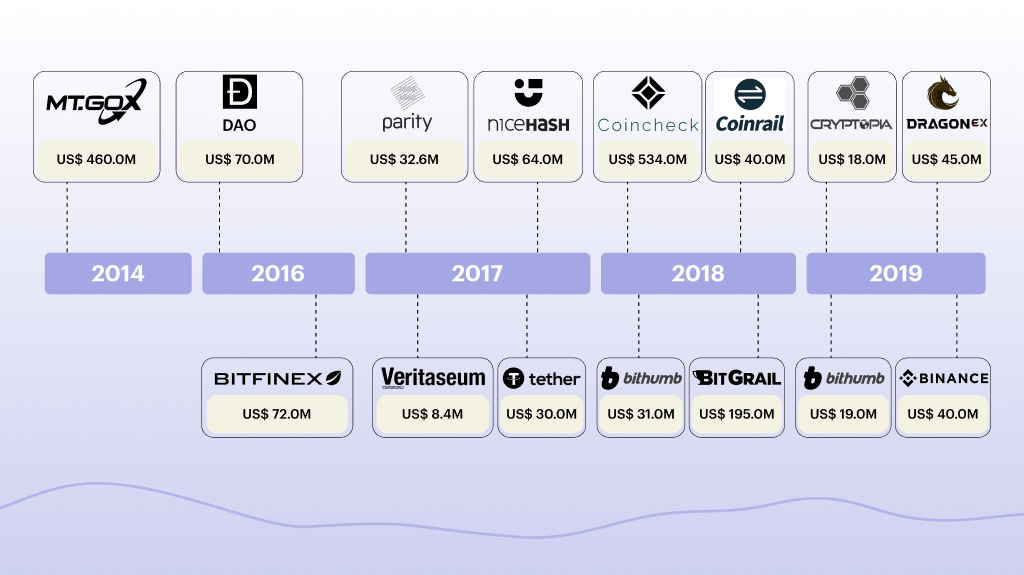

On top of that, Bitcoin has also been hit by numerous scams and thefts, which have seen more than $4 billion worth of BTC either lost or stolen since 2011.

While authorities have focused on the need to regulate cryptocurrencies, the responsibility often falls on wallet providers and crypto trading platforms that act as intermediaries.

A lack of supervision of these intermediaries poses a real threat to investors, as it puts them at risk of fraud and scams.

For instance, a major crypto exchange’s founder passed away and took the private keys for the exchange’s wallets with him. This left thousands of users with nothing more than a cautionary tale to warn others with.

Taxation brings accountability and trust. It keeps the crypto market more organized, preventing money laundering and other illegal activities.

Regulations can also provide security to investors who are looking to invest in cryptocurrencies. These laws protect them from being exploited by malicious actors and help create a climate of trust within the community.

Robust regulations and diligent taxation play a pivotal role in safeguarding consumer interests and maintaining a clear and accountable financial framework.

It’s imperative to acknowledge that cryptocurrency investments are not exempt from these crucial obligations; rather, they must fully align with the legal mandates of the specific jurisdiction in which they function.

By adhering to established financial regulations, the cryptocurrency space can foster transparency, mitigate risks, and ensure the well-being of both investors and the broader financial ecosystem.

Why Bitcoin Shouldn’t Be the Wild, Wild West

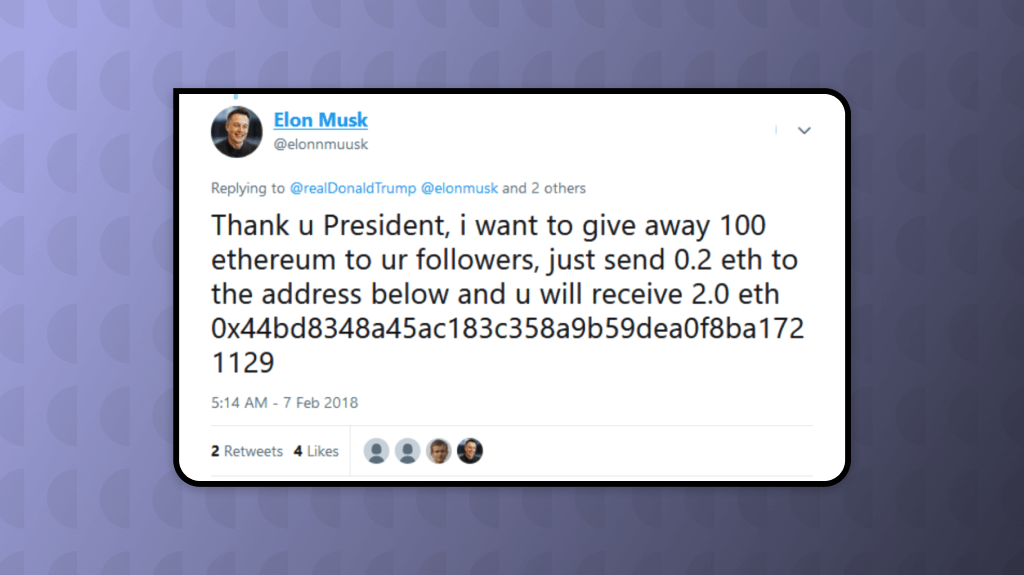

The lack of clear regulation has not only led to huge amounts of lost funds but also to illicit activity. In the digital age, criminal organizations host their work online and are often leveraging cryptocurrency’s pseudo-anonymity to engage in illegal activities. Here’s an example:

Have you ever seen Ethereum giveaway posts on Twitter? Been asked to invest in an ICO for a company that will revolutionize the world (hint: Bitconnect)?

Some time back, a U.S. Senate Committee held a hearing on crypto regulations, focusing on whether current policies and regulations sufficiently tackle the crypto industry.

The committee heard how regulations that apply to traditional banks and funds could also be applied to the growing cryptocurrency sector.

While the initial reaction to cryptocurrencies is often negative, it is good news for crypto enthusiasts that lawmakers are trying to look at the wider picture instead of simply banning cryptocurrencies outright.

After all, when have bans and witch hunts ever succeeded in silencing the voice of the people?

Better regulations lead to more adoption

The number of companies accepting crypto as payment has shot up in the last few years. Behemoths like MicroStrategy and Tesla, among others, have begun including Bitcoin on their balance sheets.

Recent patterns show that more clarity on Bitcoin regulations, and especially taxes, has convinced companies that it is now relatively safer to invest in or accept crypto.

Moreover, clear regulations have also begun to streamline the crypto sector in several countries and jurisdictions around the world.

Companies are already finding it easier to set up businesses in countries with unambiguous regulatory frameworks related to cryptocurrencies.

One example is U.S-based Circle Financial, which used to own the Poloniex exchange (now sold to the Tron Foundation). The firm moved a part of its crypto exchange operations to Bermuda, to better provide its services to its users.

The fact is that, with better and more straightforward regulations in the U.S., Circle probably wouldn’t have had to do this.

Unlike the US, Japan is taking leaps of progress, as it has been doing a great job with its regulatory framework for Bitcoin.

But what made the headlines in recent times is the European Union’s Markets in Crypto-Assets Regulation (MiCA). The MiCA bill established the most clearly defined among developed countries for businesses and individuals dealing with crypto assets. This move could be considered the spark that ignited the fire for most countries to come up with their own regulatory frameworks while drawing inspiration from EU.

Who Defines the Regulations?

While each country has its own financial regulator that oversees banking and fin-tech sectors, the crypto sector has largely been the wild-wild west with little to no oversight.

Bitcoin will greatly benefit from a regulatory structure that clearly defines it at a national level. At present, there is no single source of truth when it comes to launching a crypto business. The same is true for investing in cryptocurrencies – you are largely at the mercy of your lawyers and CPAs.

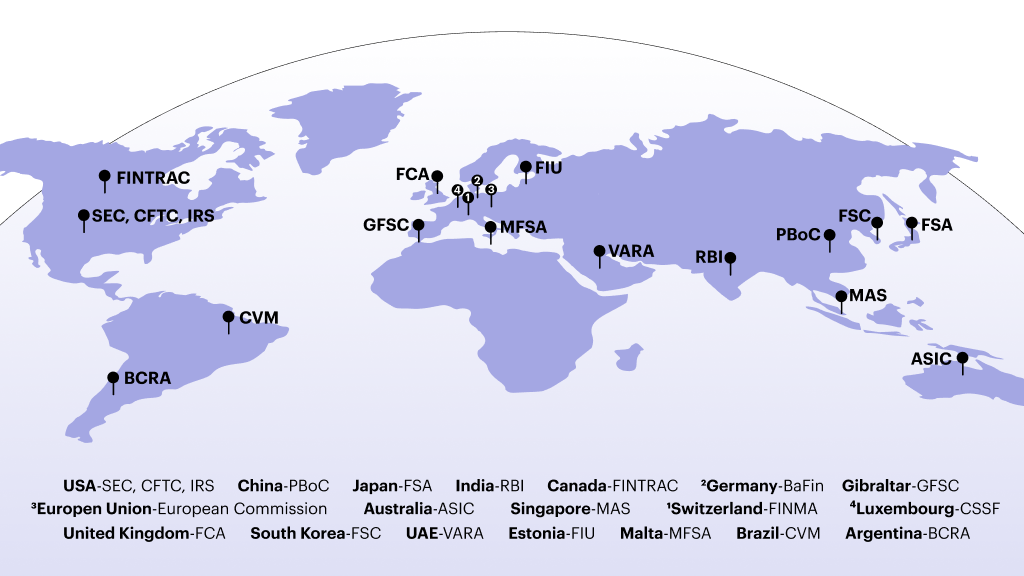

Below is a detailed list of countries, government agencies, and regulators that are involved in Bitcoin (and other cryptocurrencies) regulation around the world:

Country |

Regulatory Authorities |

Role |

| USA | Securities and Exchange Commission (SEC) | Regulates cryptocurrencies that are considered to be securities |

| USA | Commodity Futures Trading Commission (CFTC) | Regulates cryptocurrencies that are considered to be commodities |

| USA | Internal Revenue Service (IRS) | Taxes cryptocurrency transactions as property |

| China | People’s Bank of China (PBoC) | Has banned cryptocurrency trading and mining |

| India | Reserve Bank of India (RBI) | Is considering a bill that would ban cryptocurrencies or regulate them heavily |

| European Union | European Commission | Is in the process of developing a regulatory framework for cryptocurrencies |

| Canada | Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) | Requires cryptocurrency businesses to register with FINTRAC and comply with anti-money laundering regulations |

| Germany | Federal Financial Supervisory Authority (BaFin) | Regulates cryptocurrency exchanges and custodians |

| Japan | Financial Services Agency (FSA) | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with the FSA |

| South Korea | Financial Services Commission (FSC) | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with the FSC |

| United Kingdom | Financial Conduct Authority (FCA)* | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with the FCA |

| Australia | Australian Securities and Investments Commission (ASIC) | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with ASIC |

| Singapore | Monetar Authority of Singapore (MAS) | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with MAS |

| Switzerland | Swiss Financial Market Supervisory Authority (FINMA) | Regulates cryptocurrency exchanges and custodians |

| Estonia | Financial Intelligence Unit (FIU) | Requires cryptocurrency businesses to register with the FIU and comply with anti-money laundering regulations |

| Malta | Malta Financial Services Authority (MFSA) | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with the MFSA |

| Gibraltar | Gibraltar Financial Services Commission (GFSC) | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with the GFSC |

| Luxembourg | Commission de Surveillance du Secteur Financier (CSSF) | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with the CSSF |

| Brazil | Brazilian Securities and Exchange Commission (CVM) | Regulates cryptocurrency exchanges and requires cryptocurrency businesses to register with the CVM |

| Argentina | Central Bank of Argentina (BCRA) | Requires banks to block cryptocurrency transactions |

| UAE | Virtual Asset Regulatory Authority (VARA) | VARA is responsible for licensing and supervising cryptocurrency businesses, as well as enforcing anti-money laundering regulations. |

*The UK’s Financial Conduct Authority (FCA) is central to regulating cryptocurrency exchanges and businesses in the country. Cryptocurrency enterprises in the UK are obligated to register with the FCA and comply with anti-money laundering (AML) and know-your-customer (KYC) regulations, reinforcing security, consumer safeguarding, and responsible industry practices.

Crypto Companies Already Know How to Toe the Line

No one should think that cryptocurrency is totally averse to regulations.

Cryptocurrency-related companies in the U.S. and abroad have taken action to comply with rules governing other financial institutions. These include Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations.

Adhering to these standards and processes does not affect Bitcoin’s core principles of decentralization. Additionally, it is these same checks that have allowed Bitcoin to expand its reach beyond the shady darknet and forums in which its life began.

How Do Cryptocurrency Taxes Impact the Common Man?

One of the biggest debates in the crypto community regarding regulations is the issue of taxes on crypto.

Taxation has one fundamental objective: to help authorities raise the money needed to build and maintain a country’s infrastructure: hospitals, schools, roads, etc. There is often an instinctively negative reaction to any kind of taxes on crypto.

A common misconception among many taxpayers is that tax regulation brings with it psychological torment, bureaucracy, and big chunks of lost money they would rather keep. This general feeling hits a fever pitch when new laws that raise tax rates come into effect.

However, there needs more information about the importance and overall benefits of the policy. These will help people understand the reason why taxing Bitcoins can be both necessary and positive.

How to File Bitcoin Taxes?

If you have ever interacted with Bitcoin, be it as an investor or a miner, then you owe taxes (or at least report your financials to regulatory bodies). That’s right; there are tax regulations related to cryptocurrencies. But how do you file for these cryptocurrency taxes?

As tax regulations for cryptocurrencies are still in their rudimentary stages in most countries around the world, you might feel slightly overwhelmed if you’re trying to figure it out all by yourself. The process of how to file Bitcoin taxes varies across regions. Some commonalities may include the following:

- Recording all your transactions/trades

- Calculating your gains or losses

- Filing the appropriate crypto tax forms with government agencies

- Submitting tax payments, if applicable

- Keeping records as proof of taxes paid if you’re audited.

In addition to that, many countries are also actively investing in blockchain technology and providing financial incentives for cryptocurrency startups. This is a good sign that governments are embracing cryptocurrencies and digital assets, which should make filing taxes easier with time.

What Happens if You Don’t Report Cryptocurrency on Taxes?

One of the most asked questions is “What happens if you don’t report cryptocurrency on taxes?”

In general, failure to report income is considered tax evasion and is a criminal offense in many countries. In the United States, for example, taxpayers who fail to report virtual currency transactions may be subject to civil penalties or even criminal prosecution.

Simply put, not paying your taxes is punishable by law. You must report all gains (and losses) from crypto trading to your tax agency.

This means you have to keep records of transactions that result in a taxable event, such as when you trade, sell, or trade Bitcoin for other cryptocurrencies.

As tax laws may differ from country to country, it is best to look at your local tax register to find out more about the taxes you’ll need to pay.

Furthermore, many tax agencies around the world have begun to focus on crypto traders. In 2019, a Swedish trader was penalized 300% of his actual profits for not properly filing his taxes.

The US has also been active, and at the moment, thousands of people are receiving notices concerning unpaid taxes on their Bitcoin holdings.

As a crypto holder, you should know that failure to pay Bitcoin taxes is engaging in tax fraud. Not paying your deeds could see you risk time in jail or heavy financial penalties.

Ignorance is never an acceptable excuse when it comes to matters of the law. So, claiming you ‘did not know’ is unlikely to hold up.

If you feel overwhelmed by the whole tax issue, it is advisable to consult a crypto tax accountant who can help navigate you through the puddle. Alternatively, you can try using crypto tax software.

Whichever route you take, you must pay the taxes due on your Bitcoin investments.

Where Can You Find The Best Crypto Tax Software?

If you’re looking for the best crypto tax software, there are many great crypto and Bitcoin tax calculator options available to you. Many have features such as auto-calculating gains and capital loss from trading activity, handling multiple exchanges, and preparing required IRS documents. Here are some good examples:

- TurboTax Premium

- Koinly

- CoinTracker

- TaxBit

Many good crypto tax software solutions allow you to connect the platform where you trade cryptocurrencies, like Binance, Huobi, etc., and automatically get all the required data to calculate your tax liability.

However, the best Bitcoin (and other crypto) tax software for you depends on several factors. Some of these variables are:

- Is the software configured for the country where you owe taxes?

- Can the crypto exchange you are using be connected with the crypto tax tool?

- Does the software offer a portfolio tracker?

- Does it automate tax calculations?

- Is the user interface intuitive and easy to use?

- How much does using the software cost?

- Does to software have your country’s crypto tax form template?

Consider all of these factors (and others that may matter to you) before you finalize your Bitcoin tax calculator. But, how to not pay taxes on Bitcoin at all? Is that possible?

How to Not Pay Taxes on Bitcoin: Reduce Taxable Income

Many jurisdictions around the world offer ways for citizens to reduce their taxable income through legal tax breaks and incentives.

Depending on where you are located, it is possible not to pay taxes on your Bitcoin holdings. In most applicable cases, this is possible only up to a certain limit.

For example, short-term capital gains (under 365 days) are taxed at 28%. However, long-term capital gains (more than 365 days) from cryptocurrencies (including Bitcoin) are exempt. Therefore, by holding your Bitcoin for longer, you can potentially avoid paying any tax on it.

Further, since many countries have not fully regulated cryptocurrencies, there are several legal loopholes for investors to avoid taxation. However, governments are working to minimize such loopholes. Biden’s Wealth Tax Proposal is an example.

Bitcoin Mining Taxes: Capital Gains Tax or Income Tax?

In most countries, Bitcoin mining activities are considered to be a taxable event. This means that if you mine Bitcoin for profit, then profits generated from the activity will be subject to taxation according to regular income tax rules.

In cases where miners use special hardware and consume electricity to perform their work, they may be able to deduct costs associated with those items from their total reported income on taxes. This makes you eligible for tax returns or reduces tax liability.

That said, there are some exceptions to Bitcoin mining taxes. For example, if you live in a country with tax laws that classify Bitcoin mining as an investment activity (as opposed to a business), you may be able to deduct capital gains taxes from your total taxable profits.

If you are mining Bitcoin, consult a tax professional in your jurisdiction for more clarity on how you should report your earnings (or capital losses).

Note that some countries, like China, have a complete ban on Bitcoin mining.

Read where is Bitcoin illegal here.

Crypto Tax Rates Across All Countries

Below is the crypto tax rate for 200+ countries.**

Country |

Capital Gains Tax Rate |

Income Tax Rate |

| Afghanistan | 20% | 20% |

| Albania | 15% | 10%-23% |

| Algeria | 25% | 20%-35% |

| Andorra | 0% | 0% |

| Angola | 25% | 20% |

| Antigua and Barbuda | 25% | 15%-30% |

| Argentina | 21% | 20%-35% |

| Armenia | 18% | 10%-23% |

| Australia | 0%-47% | 0%-45% |

| Austria | 27.50% | 0%-50% |

| Azerbaijan | 18% | 20% |

| Bahamas | 0% | 25% |

| Bahrain | 0% | 0% |

| Bangladesh | 25% | 0%-30% |

| Barbados | 20% | 30% |

| Belarus | 13% | 13% |

| Belgium | 33% | 0%-50% |

| Belize | 12.50% | 0%-25% |

| Benin | 20% | 0%-35% |

| Bhutan | 22% | 0%-32.5% |

| Bolivia | 3% | 0%-30% |

| Bosnia and Herzegovina | 15% | 0%-40% |

| Botswana | 0% | 0%-25% |

| Brazil | 15%-22.5% | 0%-27.5% |

| Brunei | 0% | 0% |

| Bulgaria | 10%-15% | 7%-15% |

| Burkina Faso | 30% | 0%-35% |

| Burundi | 15% | 0%-30% |

| Cambodia | 0% | 0%-20% |

| Cameroon | 35% | 0%-35% |

| Canada | 0%-50% | 0%-50% |

| Cape Verde | 25% | 0%-28% |

| Central African Republic | 30% | 0%-30% |

| Chad | 35% | 0%-35% |

| Chile | 10%-27% | 0%-40% |

| China | 20%-30% | 0%-45% |

| Colombia | 19% | 0%-35% |

| Comoros | 25% | 0%-32.5% |

| Democratic Republic of the Congo | 20% | 0%-35% |

| Republic of the Congo | 0% | 0%-30% |

| Costa Rica | 15% | 0%-25% |

| Côte d’Ivoire | 20% | 0%-35% |

| Croatia | 12% | 0%-40% |

| Cuba | 0% | 0% |

| Cyprus | 20% | 0%-35% |

| Czech Republic | 19% | 15%-23% |

| Denmark | 27% | 0%-56 |

| Djibouti | 10% | 0%-35% |

| Dominica | 20% | 0%-33.3% |

| Dominican Republic | 27% | 0%-27% |

| East Timor | 0% | 0% |

| Ecuador | 22% | 0%-25% |

| Egypt | 22% | 0%-25% |

| El Salvador | 0% | 0% |

| England | 0%-20% | 0%-45% |

| Equatorial Guinea | 30% | 0%-40% |

| Eritrea | 25% | 0%-35% |

| Estonia | 20% | 20% |

| Eswatini | 15% | 0%-30% |

| Ethiopia | 20% | 0%-35% |

| Federated States of Micronesia | 0% | 0% |

| Fiji | 20% | 15%-25% |

| Finland | 30% | 25%-53% |

| France | 30% | 11%-45% |

| Gabon | 35% | 0%-35% |

| Gambia | 25% | 0%-35% |

| Georgia | 15% | 0%-20% |

| Germany | 0%-45% | 0%-45% |

| Ghana | 25% | 0%-35% |

| Greece | 15%-45% | 0%-45% |

| Grenada | 20% | 25% |

| Guatemala | 20% | 0%-35% |

| Guinea | 25% | 0%-35% |

| Guinea-Bissau | 20% | 0%-35% |

| Guyana | 25% | 0%-30% |

| Haiti | 30% | 0%-35% |

| Honduras | 15% | 0%-25% |

| Hungary | 15%-35% | 15%-40% |

| Iceland | 22% | 23%-46% |

| India | 30% | 0%-30% |

| Indonesia | 0%-30% | 0%-30% |

| Iran | 20% | 0%-25% |

| Iraq | 15% | 0%-35% |

| Ireland | 33% | 0%-40% |

| Israel | 25% | 10%-50% |

| Italy | 26% | 23%-43% |

| Jamaica | 25% | 0%-25% |

| Japan | 30% | 5%-45% |

| Jordan | 20% | 0%-35% |

| Kazakhstan | 10% | 10%-30% |

| Kenya | 30% | 0%-35% |

| Kiribati | 0% | 0% |

| Kuwait | 25% | 0%-35% |

| Kyrgyzstan | 10% | 0%-15% |

| Laos | 0% | 0% |

| Latvia | 20% | 20% |

| Lebanon | 15% | 5%-22% |

| Lesotho | 20% | 0%-35% |

| Liberia | 25% | 0%-35% |

| Libya | 20% | 0%-25% |

| Liechtenstein | 12% | 13% |

| Lithuania | 20% | 20% |

| Luxembourg | 20% | 15%-45% |

| Macedonia | 10% | 0%-15% |

| Madagascar | 20% | 0%-35% |

| Malawi | 30% | 0%-35% |

| Malaysia | 0%-30% | 0%-30% |

| Maldives | 0% | 0% |

| Mali | 25% | 0%-35% |

| Malta | 15% | 0%-15% |

| Marshall Islands | 0% | 0% |

| Mauritania | 20% | 0%-35% |

| Mauritius | 0%-30% | 0%-30% |

| Mexico | 1.9%-35% | 0%-35% |

| Micronesia | 0% | 0% |

| Moldova | 18% | 7%-20% |

| Monaco | 0% | 0% |

| Mongolia | 25% | 0%-30% |

| Montenegro | 0% | 0% |

| Morocco | 20% | 0%-40% |

| Mozambique | 25% | 0%-35% |

| Myanmar | 0% | 0% |

| Namibia | 25% | 0%-35% |

| Nauru | 0% | 0% |

| Nepal | 25% | 0%-30% |

| Netherlands | 20% | 37.10% |

| New Zealand | 0%-33% | 0%-33% |

| Nicaragua | 15% | 0%-25% |

| Niger | 30% | 0%-35% |

| Nigeria | 20% | 0%-30% |

| North Korea | NA | NA |

| Northern Mariana Islands | 0% | 0% |

| Norway | 22% | 22% |

| Oman | 20% | 0%-35% |

| Pakistan | 25% | 0%-30% |

| Palau | 0% | 0% |

| Palestine | 15% | 0%-35% |

| Panama | 0%-25% | 0%-25% |

| Papua New Guinea | 30% | 0%-30% |

| Paraguay | 10% | 0%-28% |

| Peru | 5%-29.5% | 0%-50% |

| Philippines | 20% | 20% |

| Poland | 19% | 18%-32% |

| Portugal | 17% | 14.5% – 48% |

| Qatar | 0% | 0% |

| Romania | 16% | 10%-55% |

| Russia | 20% | 13%-35% |

| Rwanda | 30% | 0%-30% |

| Saint Kitts and Nevis | 25% | 0%-25% |

| Saint Lucia | 17.50% | 0%-30% |

| Saint Vincent and the Grenadines | 25% | 0%-25% |

| Samoa | 20% | 0%-25% |

| San Marino | 7.50% | 17%-24% |

| Sao Tome and Principe | 25% | 0%-35% |

| Saudi Arabia | 20% | 0%-35% |

| Scotland | 20% | 20% |

| Senegal | 25% | 0%-35% |

| Serbia | 15% | 10%-20% |

| Seychelles | 0% | 0% |

| Sierra Leone | 30% | 0%-35% |

| Singapore | 0% | 0% |

| Slovakia | 19% | 19% |

| Slovenia | 20% | 15%-50% |

| Solomon Islands | 30% | 0%-30% |

| Somalia | NA | NA |

| South Africa | 40% | 18%-45% |

| South Korea | 24% | 6%-42% |

| South Sudan | 0% | 0% |

| Spain | 20% | 19%-45% |

| Sri Lanka | 20% | 0%-30% |

| Sudan | 20% | 0%-30% |

| Suriname | 30% | 0%-35% |

| Swaziland | 30% | 0%-30% |

| Sweden | 30% | 32.01%-56.99% |

| Switzerland | 0%-11.5% | 0%-40% |

| Syria | 25% | 0%-35% |

| Taiwan | 40% | 4%-40% |

| Tajikistan | 20% | 0%-13% |

| Tanzania | 30% | 0%-30% |

| Thailand | 15% | 5%-35% |

| Togo | 20% | 0%-35% |

| Tonga | 0% | 0% |

| Trinidad and Tobago | 25% | 0%-25% |

| Tunisia | 20% | 0%-35% |

| Türkiye (Turkey) | 30% | 15%-40% |

| Turkmenistan | 15% | 0%-10% |

| Tuvalu | 0% | 0% |

| Uganda | 30% | 0%-30% |

| Ukraine | 18% | 18% |

| United Arab Emirates | 0% | 0% |

| United Kingdom*** | 10%-20% | 0%-45% |

| Uruguay | 12% | 0%-30% |

| Uzbekistan | 14% | 0%-12% |

| Vanuatu | 20% | 0% |

| Vatican City | 0% | 0% |

| Venezuela | 30% | 0%-35% |

| Vietnam | 20% | 5%-35% |

| Wales | 20% | 20% |

| Yemen | 20% | 0%-35% |

| Zambia | 30% | 0%-30% |

| Zimbabwe | 25% | 0%-35% |

| Åland (autonomous region of Finland) | 20% | 20% |

**Note that the aforementioned tax rates are subject to change. They are as latest as August 2024 and are not updated in real time.

***Tax obligations for individuals and businesses in the UK are established and overseen by Her Majesty’s Revenue and Customs (HMRC). Adhering to UK tax laws and ensuring precise tax reporting is of paramount significance, as it not only upholds the integrity of the country’s revenue system but also fosters a fair and equitable distribution of financial resources, vital for maintaining public services and economic stability.

Conclusion

Cryptocurrency has been a disruptive force in global economic policies, shaking up paradigms established over centuries. It’s no wonder, then, that regulators worldwide have taken steps to bring crypto under their purview.

For Bitcoin to continue its meteoric rise, it needs to abide by the same rules as conventional financial systems. Regulators must see cryptocurrency businesses acting with compliance and due diligence in order to maintain trust.

So, if you’re a crypto enthusiast, it pays to stay current on legislative updates and understand the regulations that govern your everyday dealings with cryptocurrencies.

By understanding the regulations and their implications, you’ll be well-equipped to handle any changes that come your way. You can remain in compliance without sacrificing the fundamental principles of Bitcoin, which make it so revolutionary in the first place.

By doing this, we ensure that cryptocurrency is here to stay both now and in the future.

Cryptocurrency is here to stay, but it needs to be regulated and compliant. By understanding the regulations that govern our everyday dealings with cryptocurrencies, we can maintain trust and keep Bitcoin’s revolutionary principles intact.

Ensuring the enduring success of cryptocurrency hinges upon robust regulation and unwavering compliance. These safeguards not only foster investor confidence and market stability but also curb illicit activities within the realm of digital finance. It’s worth noting that the present article has been adapted to adhere to the UK’s stringent financial promotions regulations, underlining our commitment to ethical dissemination of information. It remains paramount, however, that readers exercise prudence and consult with financial and tax experts to make well-informed decisions tailored to their individual circumstances.

Keep Up with All-Things Crypto on Paybis

At Paybis, we strongly advise individuals to act according to the laws governing their jurisdiction – that includes reporting profits and losses to file taxes diligently and voluntarily.

On Paybis, you will find ample resources to learn more about cryptocurrencies, regulations, and some tools like crypto tax software to help you navigate the web3 space better.

Consider starting on your crypto investment journey with as little as $4 today with Paybis. Buy or sell crypto directly using your preferred payment method.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info