Crypto Tax US 2026: How the IRS Treats Bitcoin and Crypto Gains

- The IRS treats cryptocurrency as property. Every time you sell, trade, or spend crypto, it is a taxable event.

- Long-term gains on crypto held over 12 months are taxed at 0%, 15%, or 20% depending on your income. Short-term gains are taxed as ordinary income at 10–37%.

- From 2026, all centralized US exchanges must report your capital gains and losses to the IRS via Form 1099-DA. The IRS now has the same visibility into crypto transactions as it has into stock trades.

- Mining, staking rewards, and crypto received as payment are taxed as ordinary income at the time you receive them.

- Crypto has no wash-sale rules. You can sell at a loss and immediately rebuy to capture the tax deduction.

- Every Form 1040 filer must answer the digital asset question, regardless of how small their crypto activity was.

In 2026, the IRS knows more about your crypto activity than most investors realize. Every centralized exchange operating in the United States is now required to send Form 1099-DA directly to the IRS, reporting your capital gains and losses the same way a stockbroker reports your equity trades. The era of crypto as a reporting grey area is over.

That does not make crypto taxes simple. The rules around what counts as a taxable event, how gains are calculated, how income is treated, and how to report everything correctly are still genuinely complex. This article covers how the IRS treats cryptocurrency in 2026, what the rates are, and what you are expected to report. If you want to go deeper into Bitcoin specifically, the Paybis Bitcoin taxes guide covers Bitcoin’s tax treatment in full detail. If you are looking to buy crypto on a licensed platform with fees shown upfront, Paybis covers 90+ assets, including Bitcoin and Ethereum, for US users.

Table of contents

- How Does the IRS Treat Cryptocurrency in 2026?

- What Are the Crypto Capital Gains Tax Rates for 2026?

- What Counts as a Taxable Crypto Event in the US?

- What Crypto Transactions Are Not Taxable?

- How Is Crypto Income Taxed in the US?

- What Is Form 1099-DA and Why Does It Matter in 2026?

- How Do You Report Crypto on Your Tax Return?

- What Is Tax-Loss Harvesting in Crypto?

- Bottom Line

How Does the IRS Treat Cryptocurrency in 2026?

The IRS treats cryptocurrency as property, not currency. That classification has been in place since Notice 2014-21 and it shapes every tax obligation that flows from holding or using crypto.

Property taxation means that when you dispose of cryptocurrency, the transaction is treated like selling a stock or real estate. You calculate the gain or loss based on the difference between what you paid for it and what you received when you sold it. That gain or loss is then reported on your tax return.

The “property” classification also means that paying for a coffee with Bitcoin is technically a taxable event. You are disposing of property that has a cost basis, and if its value has gone up since you acquired it, you have realized a gain. Most people do not think about everyday crypto spending in those terms, but the IRS does.

Crypto transactions fall into two categories for tax purposes. Disposals, including sales, trades, and spending, generate capital gains or losses. Earning crypto through mining, staking, or receiving it as payment generates ordinary income. The distinction matters because the two categories are taxed at different rates.

What Are the Crypto Capital Gains Tax Rates for 2026?

The rates depend on how long you held the crypto before disposing of it.

Short-term capital gains apply when you hold crypto for 12 months or less before selling or trading. These gains are taxed at your ordinary income tax rate, which ranges from 10% to 37% depending on your total taxable income for the year. There is no preferential treatment for short-term gains.

Long-term capital gains apply when you hold crypto for more than 12 months. For 2026, the rates are:

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $47,025 | $47,026 – $518,900 | Above $518,900 |

| Married filing jointly | Up to $94,050 | $94,051 – $583,750 | Above $583,750 |

| Head of household | Up to $63,000 | $63,001 – $551,350 | Above $551,350 |

High-income investors face an additional 3.8% Net Investment Income Tax (NIIT) on top of the standard long-term rate if their modified adjusted gross income exceeds $200,000 for single filers or $250,000 for married filing jointly.

The difference between short-term and long-term treatment on a $100,000 gain can be $17,000 or more in tax savings. The 12-month holding threshold is one of the most significant variables in crypto tax planning. Holding crypto inside a retirement account changes the picture significantly. The Paybis guide to crypto ETFs in IRAs and 401(k)s covers how tax-deferred and tax-free growth works for crypto investments.

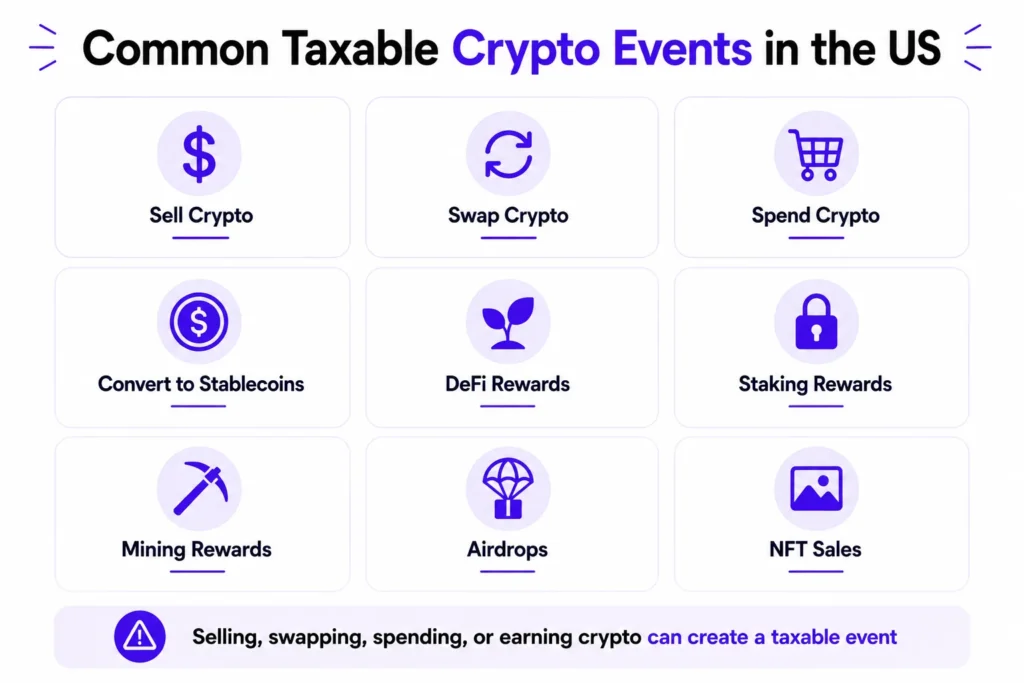

What Counts as a Taxable Crypto Event in the US?

The IRS interprets “disposal” broadly. These are all taxable events:

- Selling crypto for US dollars or any fiat currency

- Trading one cryptocurrency for another: exchanging Bitcoin for Ethereum is a disposal of Bitcoin at its current fair market value. The Paybis crypto swap taxes guide covers this in detail.

- Spending crypto on goods or services: paying with crypto is treated as selling it at the point of transaction

- Converting crypto to stablecoins: this is technically a sale even if it feels like parking funds

- Receiving DeFi rewards: yield farming returns, liquidity mining rewards, and lending income

- Staking rewards: taxable as ordinary income when received

- Mining rewards: taxable as ordinary income at the fair market value on the date received

- Airdrops: taxable as ordinary income when received

- NFT sales and trades: each transaction is a disposal

The amount of the transaction does not affect whether it is taxable. A $10 crypto payment for a service is just as reportable as a $100,000 sale. The IRS requires all disposals to be tracked and reported.

What Crypto Transactions Are Not Taxable?

Not every interaction with crypto triggers a tax obligation.

- Buying crypto with fiat currency is not a taxable event. Purchasing Bitcoin with US dollars simply establishes your cost basis. No gain or loss is realized until you dispose of it.

- Transferring crypto between your own wallets is not taxable. Moving Bitcoin from an exchange wallet to a hardware wallet you own does not constitute a disposal. Keeping records of these transfers is important to demonstrate ownership continuity.

- Gifting crypto to another person is generally not taxable up to the annual gift tax exclusion ($18,000 per recipient in 2024, subject to adjustment). The recipient inherits your cost basis and holding period. Gifts above the exclusion may require filing a gift tax return, though gift tax itself is rarely owed.

- Donating crypto to a qualified charity can generate a deduction for the fair market value at the time of donation without triggering capital gains tax on the appreciation. This can be one of the most tax-efficient ways to make charitable contributions for people with appreciated crypto.

- Receiving crypto as a gift is not immediately taxable. Tax applies when you later sell or trade it.

How Is Crypto Income Taxed in the US?

When you earn cryptocurrency, it is taxed as ordinary income at fair market value on the date you receive it. The income category it falls into depends on how you earned it.

- Mining rewards are taxed as ordinary income and may also be subject to self-employment tax if mining constitutes a trade or business. The value used is the fair market value of the crypto on the day the reward was received. Your cost basis in that crypto is then set at that same value for future capital gains calculations.

- Staking rewards are taxable as ordinary income when received, based on fair market value at the time of receipt. A 2023 court case challenged this treatment for certain staking situations, but IRS guidance has maintained the income characterization.

- Crypto received as payment for services is treated identically to receiving that payment in dollars. If a client pays you $5,000 worth of Ethereum for a project, you have $5,000 of ordinary income. Your cost basis in that Ethereum is $5,000.

- Airdrops and hard forks are treated as ordinary income at fair market value when the crypto is received and you have dominion and control over it.

Crypto income is reported on Schedule 1 (Form 1040) for most individuals or Schedule C for self-employed individuals whose crypto earnings are part of a trade or business.

What Is Form 1099-DA and Why Does It Matter in 2026?

Form 1099-DA is the IRS form for reporting digital asset transactions, and 2026 is the first year it is mandatory for all centralized cryptocurrency exchanges operating in the United States.

Before 2026, crypto reporting varied significantly between exchanges. Some sent Form 1099-B, others sent informal transaction summaries, and some sent nothing. The IRS received limited data directly. That has changed. From 2026, every centralized exchange must report each customer’s capital gains and losses directly to the IRS, the same way traditional brokers report stock transactions.

What this means for crypto holders:

- Your exchange will send you a Form 1099-DA showing your reported gains and losses for the year

- The same data goes directly to the IRS

- Mismatches between what you report on your return and what your exchange reported will be flagged automatically

- The IRS has significantly more information than it had in previous years

Form 1099-DA does not replace your obligation to track and report your own transactions accurately. Cost basis reporting from exchanges may be incomplete, particularly for assets transferred in from other platforms or wallets. Reviewing the form carefully against your own records is important before filing. For a direct comparison of how Paybis and Coinbase handle IRS reporting differently, the Paybis vs Coinbase IRS reporting guide explains what each platform sends and what you are responsible for tracking yourself.

How Do You Report Crypto on Your Tax Return?

Crypto reporting happens across several forms depending on the nature of your activity.

- Form 8949 is where you list every individual crypto disposal. Each sale, trade, or spending transaction gets its own line with the acquisition date, sale date, cost basis, proceeds, and resulting gain or loss.

- Schedule D (Form 1040) summarizes the totals from Form 8949, separating short-term and long-term gains and losses.

- Schedule 1 (Form 1040) is where crypto income from staking, airdrops, and similar sources is reported as additional income.

- Schedule C (Form 1040) applies if your crypto activity constitutes a trade or business, such as professional mining.

- The digital asset question on Form 1040 must be answered by every filer. It asks whether you received, sold, exchanged, or otherwise disposed of any digital assets during the year. Answering “no” when you did have activity is a false statement on a federal tax return.

The IRS strongly recommends keeping detailed records of every transaction, including the date of acquisition, the amount paid, the fair market value on relevant dates, and the platform used. Tax software designed for crypto, such as CoinLedger or Koinly, can automate much of this tracking by connecting to exchange APIs. The Paybis guide to the best crypto tax software compares the leading tools by features and pricing.

What Is Tax-Loss Harvesting in Crypto?

Tax-loss harvesting means deliberately selling crypto at a loss to reduce your taxable gains elsewhere.

If you have made $20,000 in gains from Bitcoin but also have $15,000 in unrealized losses in other assets, selling those losing positions reduces your net taxable gain to $5,000. The losses offset the gains.

Crypto has a significant advantage over stocks here: the wash-sale rule does not apply. Under wash-sale rules, if you sell a stock at a loss and buy the same or a substantially identical stock within 30 days, you cannot claim the loss. Crypto is classified as property, not a security, so no wash-sale restriction applies. You can sell Bitcoin at a loss today and rebuy it immediately without forfeiting the deduction.

Capital losses that exceed your capital gains in a given year can offset up to $3,000 of ordinary income. Losses beyond that carry forward to future years indefinitely.

This is one area of crypto taxation where the property classification works in a holder’s favor. Whether it continues without legislative change is uncertain, as Congress has discussed extending wash-sale rules to crypto on multiple occasions.

Bottom Line

The IRS treats cryptocurrency as property. Every sale, trade, and spending transaction is potentially taxable. Long-term holders benefit from preferential capital gains rates of 0%, 15%, or 20%. Short-term gains are taxed as ordinary income at rates up to 37%. From 2026, Form 1099-DA means every centralized US exchange reports your transactions directly to the IRS, removing the ambiguity that previously characterized crypto tax reporting. Keeping accurate records of every transaction is not optional. A qualified tax professional with crypto experience is the right resource for anything beyond the general framework this article covers.

This article is for general informational purposes only. It does not constitute tax advice. Crypto tax rules are complex and depend on individual circumstances. Consult a qualified tax professional or CPA before making any decisions about your crypto taxes.

FAQ

Do I have to report crypto if I did not sell anything?

You still need to answer the digital asset question on Form 1040, but if you only bought crypto and made no disposals during the year, you generally do not have a reportable taxable event from those holdings. However, if you received crypto through staking, mining, airdrops, or as payment, that income is reportable even if you did not sell. The question on Form 1040 must be answered honestly regardless of the amount involved.

Is trading Bitcoin for Ethereum a taxable event?

Yes. The IRS treats crypto-to-crypto trades as disposals. When you trade Bitcoin for Ethereum, you are treated as having sold your Bitcoin at its current fair market value. If the Bitcoin has appreciated since you acquired it, that appreciation is a capital gain. The Ethereum you received establishes a new cost basis at its fair market value on the date of the trade. This rule catches many crypto holders off guard, particularly those who do frequent trades across many assets.

How does the IRS know about my crypto?

The IRS receives data through several channels. From 2026, Form 1099-DA requires all centralized US exchanges to report customer transactions directly. The IRS has also used blockchain analytics firms like Chainalysis to trace transactions on public blockchains. Court orders have previously compelled exchanges to hand over user records for high-volume traders. Several states and countries now share financial data with the IRS under information exchange agreements. Treating crypto as invisible to tax authorities is a significant and increasingly well-documented error.

What happens if I did not report crypto in previous years?

If you have unreported crypto gains from prior years, consulting a tax professional about your options is important before the IRS contacts you. Voluntary disclosure before an audit generally results in significantly better outcomes than discovery after the fact. The IRS has sent waves of warning letters to crypto holders and has pursued criminal charges in cases of clear intentional evasion. The statute of limitations for civil tax assessment is typically three years from the filing date, extended to six years for substantial underreporting.

Can I use crypto losses to offset other investment gains?

Yes. Crypto capital losses can offset capital gains from other asset classes including stocks, real estate, and other investments. If your total capital losses exceed your capital gains in a year, up to $3,000 of the excess can offset ordinary income, with any remaining losses carrying forward to future tax years. This makes crypto an asset class where losses have real tax utility beyond the crypto market itself, particularly for investors with gains in other portfolios.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info