Crypto to Stablecoin to Cash: Is This Faster or Cheaper?

– Converting crypto to a stablecoin first can protect value during slow bank transfers and volatile markets. Set up your crypto wallet before you start so funds move without delay.

– The stablecoin route adds extra conversion and network fees.

– Direct withdrawals usually cost less for smaller cash-outs. You can also buy Bitcoin with a bank account and reverse the process when cashing out via the same rail.

– Paybis shows the full fee breakdown before confirmation and settles sell orders quickly. ACH users can also buy Bitcoin with ACH transfer for a seamless round-trip experience.

– Use stablecoins for slower 2–3 day bank transfers. Use direct withdrawals when settlement is fast and transparent.

Crypto assets can increase or decrease in value. Paybis is a payment gateway, not an investment service. This content is for informational purposes only and does not constitute financial advice.

Most users compare trading fees and overlook the money lost when crypto prices swing during a 3-day bank transfer. That gap is exactly where the stablecoin conversion strategy earns its place, but it also carries its own cost. Paybis breaks down the exact steps, fees, and timing for both routes so you can choose the smarter path for your withdrawal.

The Stablecoin Withdrawal Strategy Explained

A stablecoin (a digital coin pegged to $1, like USDC or USDT) acts as a price-locked waiting room between your volatile crypto and your bank account. Instead of selling Bitcoin directly for euros while the price moves, you first convert to USDC, then sell USDC for euros when you’re ready. Paybis supports both USDT and USDC across multiple networks, as explained in the guide to stablecoins on Paybis. For a broader look at the regulatory landscape around dollar-pegged tokens, the STABLE Act overview is worth reading before you commit to a stablecoin strategy.

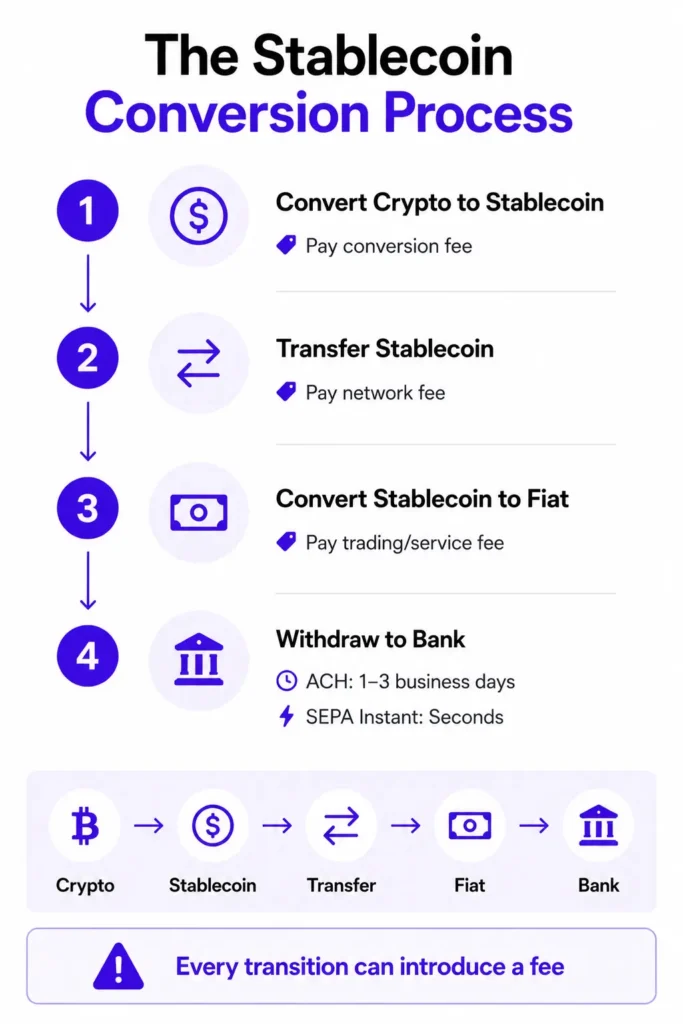

The Stablecoin Conversion Process Explained

The four-step stablecoin route works like this:

- Sell volatile crypto for stablecoin on an exchange, paying a conversion fee set by that platform.

- Transfer the stablecoin to your cash-out platform, paying a network fee that varies by blockchain.

- Sell the stablecoin for fiat (your local currency) on the receiving platform, paying a second service or trading fee.

- Withdraw fiat to your bank, waiting 1–3 business days for ACH or within seconds for SEPA Instant. Each transition is a fee point.

Payout Timeframes: Direct or Stablecoin?

Cashing Out Crypto Directly

The speed of a direct cash-out depends on the withdrawal method you choose. ACH transfers usually settle within 1–3 business days, while domestic wire transfers typically arrive within 24 hours. SEPA Instant settles in under 10 seconds if supported by your bank, while standard SEPA transfers take 1–2 business days. Paybis provides step-by-step guides for each withdrawal method, making the process easier to follow. For a full walkthrough of the cash-out process, the how to cash out Bitcoin guide covers every major method in detail.

USDC to Cash Conversion Speed

On-chain, stablecoin transfers move fast. ERC-20 (Ethereum network) USDT or USDC transfers confirm within 5–20 minutes under normal conditions, though congestion during high-traffic events like token launches can push this toward 30 minutes. TRC-20 (TRON network) produces a block every three seconds, and most transfers complete within five minutes end-to-end after exchange deposit credits. The blockchain leg is fast. The bank leg after the stablecoin sale takes just as long as any other fiat withdrawal.

Maximizing Crypto Withdrawal Speed

Three factors drive withdrawal speed. First, choose a platform that supports SEPA Instant or card payouts rather than standard ACH. Second, transfer stablecoins during off-peak network hours to avoid network fee spikes. Third, use TRC-20 for stablecoin transfers where supported because confirmation is near-instant and fees are predictable. Paybis consistently delivers a competitive net received amount on SEPA sell orders, meaning you typically receive more euros on a Bitcoin sale via Paybis SEPA than on comparable platforms at the same transaction size.

Direct Withdrawal vs. Stablecoin Route: Fee Comparison

Fees for Direct Crypto-to-Cash Withdrawal

A direct withdrawal carries these fee components:

- Service fee: Starts from 1.49% on Paybis (0% on your first card transaction)

- Payment processing fee: 4.5–8.5% for card transactions over $50, depending on currency

- Spread: The hidden markup between market price and the rate offered, common on platforms that don’t show net received upfront

The spread is the fee most platforms don’t show until checkout. Most platforms embed a spread on top of advertised fees, meaning a “$500 sell” shown at the quote stage may yield only $462 after spreads and processing are applied at the final step. For further context on how pricing works across different platforms, the guide to frictionless off-ramping and easiest crypto-to-fiat conversions compares the main options side by side.

Stablecoin Path: What You’ll Pay

The stablecoin route doubles the fee exposure:

- First conversion fee: A service or trading fee to convert BTC or ETH to USDC, set by the platform you use for that step

- Network fee: ERC-20 transfers cost $0.05–$0.50 under normal conditions, though fees can spike during peak network activity. TRC-20 fees sit in the $2.00–$4.00 range depending on recipient wallet status. BEP-20 on Binance Smart Chain generally offers lower fees of $0.10–$0.30

- Second conversion fee: A service or trading fee to convert USDC to fiat on the cash-out platform

- Fiat withdrawal fee: Same as the direct method

On a $200 transaction, paying $3.00 in TRC-20 fees before the second conversion already represents 1.5% of the total value before any service fees are counted.

How to Pay Less for Crypto Cash

The most practical way to reduce cost is to skip the stablecoin step entirely when using a platform that shows net received before you confirm. On Paybis, the exact fiat amount credited after all fees is displayed at the quote stage, before entering payment details, covering service fees, spreads, and processing costs in a single number.

Your Guide to Stablecoin Cash Conversion

Protecting Funds in Market Dips

The stablecoin route makes clearest sense when a large withdrawal coincides with a volatile market and a slow bank transfer. If you’re moving $1,000 worth of ETH and ACH takes 2 business days, even a modest 5–6% price drop costs $50–$60. Paying $2–3 in network fees to lock in your value via USDT is a straightforward trade-off in that scenario. Some users also convert profits to USDC immediately after a price surge rather than cashing out all the way to fiat, which captures the dollar value without triggering a fiat withdrawal and keeps funds available for a future crypto purchase. If you’re weighing how much Bitcoin exposure makes sense before you cash out, the guide on how much Bitcoin you should own offers a useful framework.

Note: converting crypto to a stablecoin may be a taxable disposal in many jurisdictions, so check the rules in your country before using this approach. While stablecoins are designed to maintain a $1 peg, market liquidity and volatility can affect stability, and no stablecoin maintains perfect parity with its peg at all times.

Bypassing Slow Bank Transfers

The on-chain leg of a stablecoin transfer operates 24/7 regardless of weekends, bank holidays, or cut-off times. TRC-20 transfers typically complete in under five minutes, while ERC-20 transfers typically take 5–20 minutes under normal network conditions. The subsequent fiat bank settlement follows standard banking timelines and is not exempt from these delays.

This is genuinely useful for international remittances. SWIFT transfers typically take 2–5 business days and carry layered costs: sending banks typically charge $15–$50, intermediary banks can add further fees per hop, receiving banks may apply an additional charge, and exchange rate markups of 2–5% apply on top. Crypto-based transfers can move funds faster and more cost-effectively across borders compared to traditional wire transfers.

Direct Option: When It Saves You Money

For Lower Fees on Small Crypto Withdrawals

On a $100 withdrawal, network fees of $2–3 represent 2–3% of the transaction value before any service fees. That cost is hard to justify. On small amounts, the stablecoin route costs you more in total fees than any price protection is worth. If you’re still building your position and want to understand entry costs, the article on how many dollars it takes to buy a Bitcoin puts small-amount investing in perspective.

Skip Stablecoin Fees in Calm Markets

When price volatility is low, the risk that justifies the stablecoin hedge simply isn’t present. Adding two conversion fees and a network fee to protect against a 0.5% overnight move is not a favorable trade. In stable market conditions, a direct sell via SEPA gives you more fiat in your account faster, without the intermediate steps. Paybis delivers a measurable net received advantage on SEPA sell orders compared to major competitors, making the direct route the more cost-effective choice in stable market conditions.

Prioritize Speed for Urgent Withdrawals

Card payouts and SEPA Instant settle near-instantly after the sell order confirms. The Paybis video guide page covers the fastest available routes step by step. When you need the money today and your bank supports SEPA Instant or card payouts, the direct route is faster than routing through a stablecoin conversion first.

Common Pitfalls of Crypto Cash-Outs

Price Volatility Risk During Direct Withdrawal

The real danger of a direct withdrawal via ACH is the 1–3 day gap between when you sell and when the money arrives. Crypto markets can move significantly within that window, with historical single-day moves of 5–9% not uncommon during corrections.

A $1,000 withdrawal initiated at peak price and settled three days later during a correction can return meaningfully less than expected. Stablecoins eliminate this specific risk. Fast platforms using card payouts or SEPA Instant reduce it by shrinking the settlement window to minutes.

Minimize Stablecoin Conversion Costs

ERC-20 gas fees rise during NFT mints, token launches, and large liquidation events. Under current network conditions, ERC-20 transfers typically cost under $0.50 outside of peak activity, but network spikes remain unpredictable.

Choosing TRC-20 for stablecoin transfers where supported keeps fees in the $2.00–$4.00 range depending on recipient wallet status and confirmation within five minutes, though BEP-20 on Binance Smart Chain consistently offers lower fees of $0.10–$0.30. If you use the wrong network for a withdrawal, the Paybis support guide on sending crypto on the wrong network explains the recovery steps.

Exchange Hacks: Are Your Funds Safe?

Every day funds sit on a centralized exchange during a withdrawal queue is a day they are exposed to custodial risk. Paybis has operated since 2014 with no security breaches and holds licenses from FinCEN (US), FINTRAC (Canada), FCA (UK), and VASP registration in Poland (RDWW-805). Paybis holds 31,550+ Trustpilot reviews with a rating of 4.1 or “Great,” and the payout security guide explains how MPC-based custody protects assets during the withdrawal process. For background on how to protect yourself from other common threats in the crypto space, the guide on cryptojacking and how to protect your computer is a practical read.

Your Smart Crypto to Cash Strategy

Total Costs for Each Cash-Out Method

| Method | Speed | Fee Structure | Best For |

|---|---|---|---|

| Direct via SEPA Instant | Under 10 seconds | Service fee + processing (no SEPA surcharge) | Urgent EUR withdrawals |

| Direct via ACH | 1–3 business days | Service fee + processing | US users, lower urgency |

| Direct via card payout | Near-instant | Service fee + card processing | Fast cash to debit card |

| Stablecoin via TRC-20 | Under 1 min on-chain (often seconds) + 1–3 days bank | 2 conversion fees + $2.00–$4.00 network | Volatile markets, value protection |

| Stablecoin via BEP-20 | Minutes on-chain + 1–3 days bank | 2 conversion fees + $0.10–$0.30 network | Lowest network fees |

| Stablecoin via ERC-20 | 5–20 min on-chain + 1–3 days bank | 2 conversion fees + $0.05–$0.50 network fee | ETH-compatible platforms |

Gauge Market Conditions Before You Convert

Before initiating a withdrawal, check the current price trend over the past 24 hours and your withdrawal method’s settlement time. If the market has moved sharply and your bank transfer takes 2+ days, the stablecoin hedge is worth the extra fees. If the market is stable and you’re using SEPA Instant or a card payout, the direct route gives you more cash with fewer steps.

Choose Your Crypto Withdrawal Speed

The right method comes down to two variables: settlement speed and market conditions.

- Volatile market + slow bank transfer: Use the stablecoin route. Lock in your value and pay the conversion fees as price insurance.

- Small amounts: Consider the direct route. Two conversion fees plus a network fee may cost more proportionally than the volatility protection provides.

- Urgent withdrawal + SEPA Instant or card: Use the direct route. Settlement completes in seconds with no second conversion step. Paybis operates in 180+ countries, supports 20+ payment methods, and handles 90+ cryptocurrencies. The sell crypto guide covering Neteller, Skrill, and bank transfer options covers all available cash-out options by region.

Ready to sell crypto with transparent pricing? Open an account on Paybis where it displays your exact net received amount upfront at the quote stage, with no hidden spreads at checkout. Paybis offers 24/7 human support with an average response time of 1–2 minutes if anything needs resolving during the process.

Key Terminology

- Authorization hold: A temporary reservation of funds on your card or bank account while a payment is being verified or processed. The money is not fully charged until the transaction is completed.

- Stablecoin: A cryptocurrency pegged to a fiat currency (usually $1), such as USDC or USDT. The price does not fluctuate with market conditions, making it useful as a value-holding step between selling volatile crypto and receiving fiat.

- Spread: The difference between the market exchange rate and the rate an exchange offers you. It is a hidden fee not shown as a line item, and it reduces the fiat or crypto you actually receive.

- Off-chain: Activity that happens outside the blockchain network. For example, an exchange updating your account balance internally without recording every step on the blockchain.

- Blockchain: A digital ledger that records transactions across a network of computers. Once transactions are confirmed, they are difficult to change or remove.

FAQ

Are Stablecoins Safe in Market Dips?

Stablecoins are designed to target a $1 peg and reduce exposure to Bitcoin or Ethereum price movements, but no stablecoin maintains perfect parity with its peg at all times. Market liquidity and volatility can influence stability, meaning the protection offered is a reduction in price exposure, not a guarantee of it. The primary risk is platform custody, not price exposure, so using a regulated platform with a clean security track record matters.

When Do Stablecoin Conversion Fees Peak?

ERC-20 gas fees rise during high network activity such as token launches, NFT mints, or large liquidations, and can spike unpredictably even when conditions appear calm. TRC-20 fees generally run $2.00–$4.00 depending on recipient wallet status, while BEP-20 on Binance Smart Chain keeps fees in the $0.10–$0.30 range. Scheduling transfers during off-peak hours and choosing lower-fee networks keeps costs more predictable.

Which Stablecoin Works Best for Withdrawals?

USDT on TRC-20 offers low network fees ($2.00–$4.00 depending on recipient wallet status) and fast confirmation for most cash-out use cases, though BEP-20 on Binance Smart Chain provides lower fees of $0.10–$0.30 if the receiving platform supports it. USDC on ERC-20 is better if the receiving platform only supports Ethereum-based tokens.

How Can You Cut Your Crypto Withdrawal Fees?

Platforms that display net received before you confirm capture all visible and invisible costs, including spreads, in a single number, making it possible to compare providers on actual value received rather than advertised rates alone. For smaller withdrawal amounts, consider using the direct route since two conversion fees plus a network fee on the stablecoin path may outweigh the cost savings from volatility protection.

Disclaimer: Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more at: https://go.payb.is/FCA-Info